NACA program house hacking is one of the most underutilized combinations in real estate — especially for first-time buyers who’ve been told they need perfect credit and a 20% down payment to get started.

I’ll be upfront: most “no money down” content online is either outdated, overhyped, or buried in asterisks. So when I come across a program that’s legitimately been around for decades and has actual homeowners behind it, I pay attention.

NACA is one of those programs.

What Is the NACA Program?

NACA stands for Neighborhood Assistance Corporation of America. It’s a nonprofit organization that runs a mortgage program specifically designed for people who don’t fit the traditional lending mold — lower credit scores, limited savings, or income that doesn’t look great on paper.

The program has been around since the 1980s and has helped hundreds of thousands of people buy homes. This isn’t a social media trend. It’s an established program with a real track record.

The NACA Program Benefits Are Actually This Good

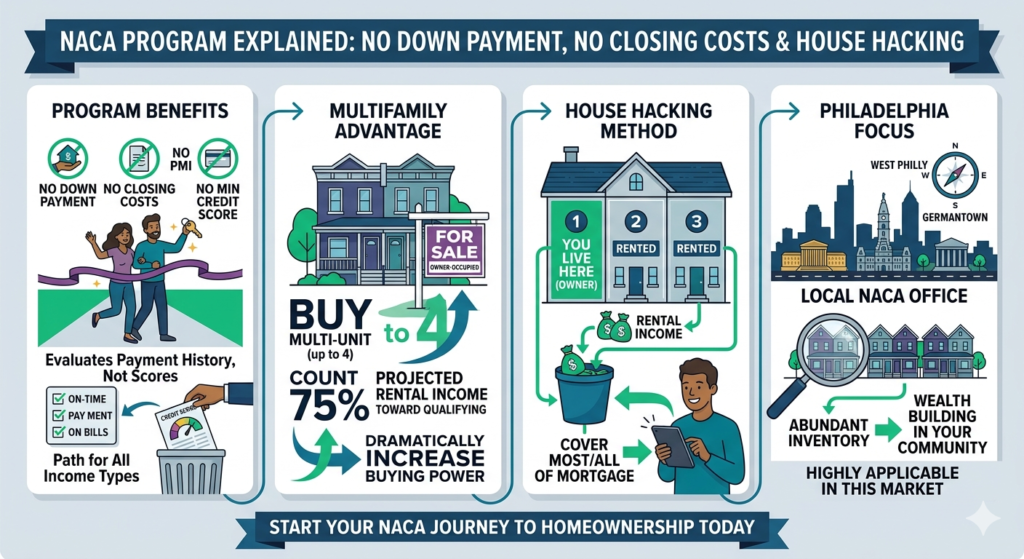

Here’s what NACA offers — and yes, these are real:

No down payment. Zero. You don’t need to bring any money to the table for the purchase price.

No closing costs. The fees that typically eat up 2–5% of a home’s purchase price at closing — gone.

No PMI. Private mortgage insurance, which conventional lenders require when you put down less than 20%, is not part of the NACA program.

No minimum credit score. Instead of pulling your FICO score, NACA looks at your payment history — rent, utilities, recurring bills. If you’ve been paying your obligations consistently, that matters more than your number.

Income flexibility. NACA doesn’t necessarily disqualify you for having a modest income. What they care about more is your debt load relative to what you earn.

For someone just starting out — or someone who’s been told by a conventional lender that they don’t qualify — this combination is significant.

The NACA Program House Hacking Angle

Here’s where the NACA program gets really interesting for investors.

NACA is an owner-occupant program. You have to live in the property you’re buying. But you can buy a multifamily property — a duplex, triplex, or fourplex — as long as you live in one of the units. And when you do, NACA will count 75% of the projected rental income from the other units as part of your qualifying income.

That changes the math completely.

The investor in the video I watched had a $40,000 annual salary. On his own, that qualified him for roughly $300,000 in financing — not enough for a multifamily property in most markets. But by applying for a multifamily home through the NACA program and having rental income from the other units counted toward his qualifying income, he was able to purchase a property that would have been completely out of reach on his W-2 alone.

He moved into one unit. Rented the others. The rental income covered most or all of his mortgage payment. He was essentially living for free while building equity and generating income.

That’s NACA program house hacking — and it’s one of the cleanest ways to execute this strategy with minimal upfront capital.

The Catch

The NACA program isn’t instant. The process is longer and more involved than a conventional mortgage. You have to attend a homebuyer workshop, work with a NACA counselor, go through a qualification process, and demonstrate financial readiness — which can take months.

The program also requires you to stay engaged. If you have credit issues or past financial problems, NACA will work with you to address them, but that takes time.

And owner occupancy is required. This is not a program you can use to buy a pure investment property you never live in. The multifamily house hacking approach works because you’re genuinely living there.

According to HUD.gov, nonprofit mortgage assistance programs like NACA have consistently produced lower default rates than conventional subprime lending — which is part of why the program has survived and expanded over four decades.

NACA Program House Hacking in Philadelphia

Philadelphia actually has a NACA office — which matters because the counseling and qualification process is done locally. For buyers in this market, that means working with counselors who understand Philadelphia’s specific neighborhoods, price points, and programs.

Given how many multifamily properties exist in Philadelphia — rowhouses converted to duplexes, triplexes throughout West Philly, Germantown, and North Philly — the house hacking opportunity here is real. These properties exist all over the city, often at price points that work with NACA’s structure.

My accountant runs my taxes lean, which means my reported income looks lower than my actual financial picture. That’s a problem with conventional lenders. NACA’s approach of looking at payment history and debt load instead of just income is interesting in that context. If I ever buy a duplex or triplex to live in while I’m building toward larger development — which honestly fits my roadmap — the NACA program is worth a serious conversation.

Who the NACA Program House Hacking Strategy Is Actually For

NACA makes the most sense for:

Someone buying their first home or first multifamily property who has limited savings but a solid history of paying their bills. Someone with a non-traditional income situation — self-employed, variable income — who keeps getting turned down by conventional lenders. Someone who wants to house hack a multifamily property and use rental income to offset or eliminate their housing costs. Someone with credit challenges who needs a lender that looks at the full picture rather than just a score.

If that’s you, NACA is worth the time it takes to go through the process. The benefits are real and the program has the track record to back it up.

Use the Philadelphia House Hacking Calculator to run the numbers on a specific property before you start the NACA program application process.

Not financial advice — just someone doing a lot of research and asking a lot of questions.