Here’s a situation a lot of real estate investors find themselves in — and I’m going to be honest because it describes me pretty well too.

You have good credit. You have a business. You have real assets and real experience. But your tax returns make you look broke on paper, because you (or your accountant) did exactly what you were supposed to do: wrote off every legitimate deduction, minimized taxable income, and paid less to the IRS.

Smart tax planning. Terrible mortgage application.

This is exactly the problem DSCR loans were designed to solve. And in Philadelphia’s current market, understanding how they work could be the difference between staying on the sidelines and actually buying something.

What Is a DSCR Loan?

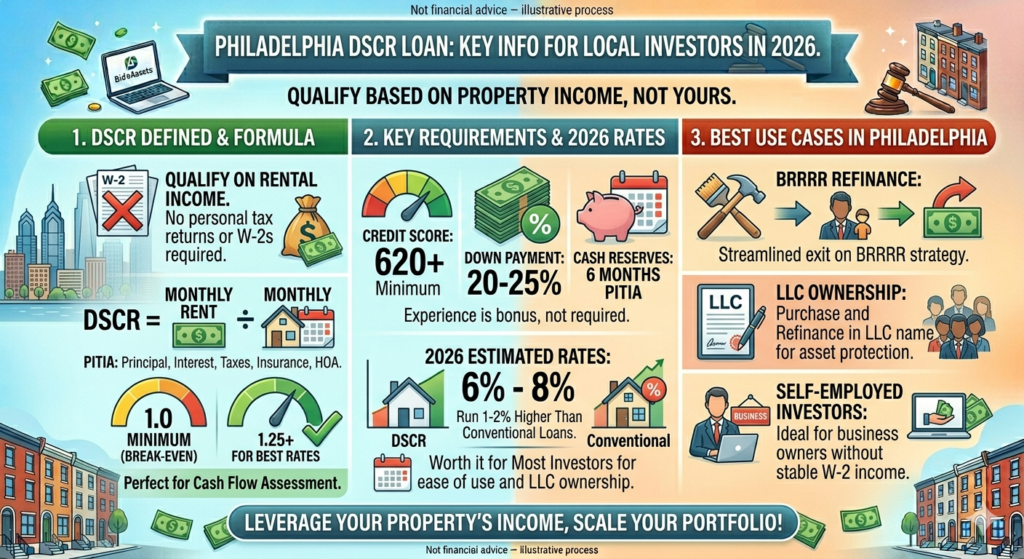

DSCR stands for Debt Service Coverage Ratio. A DSCR loan is a type of non-QM (non-qualified mortgage) loan designed for real estate investors, where approval is based on the property’s debt service coverage ratio rather than the borrower’s personal income. It allows real estate investors to qualify based on rental income potential instead of traditional income documentation. BiggerPockets

Translation: the lender doesn’t care what’s on your tax returns. They care whether the property can pay for itself.

A traditional mortgage loan will require income verification, tax returns, and a debt-to-income ratio. DSCR loans require none of these. BiggerPockets

How the Math Works

The DSCR formula is simple:

Monthly Rent ÷ Monthly PITIA = DSCR

PITIA = Principal + Interest + Taxes + Insurance + HOA (if applicable). It’s the full monthly cost of owning the property.

A DSCR of 1.0 means the property’s rent exactly covers its debt service. A DSCR of 1.25 means the rent exceeds debt service by 25% — the threshold most lenders use to unlock their best rate tier. Real Estate Witch

Real example for Philadelphia:

- Property rents for $1,800/month

- Monthly PITIA: $1,400

- DSCR = 1.28 ✅ — qualifies at most lenders, good rate tier

- Property rents for $1,200/month

- Monthly PITIA: $1,400

- DSCR = 0.85 — some lenders will still do this, but you’ll need more down and pay a higher rate

Philadelphia’s rental market actually helps here. Germantown, Brewerytown, and West Philly rental demand has stayed strong — which means properties in those areas can often hit the 1.25 DSCR threshold that gets you the best terms. Redfin

What You Need to Qualify in 2026

To qualify for a DSCR loan in 2026, you typically need a credit score of 620 or higher, a down payment of 20-25% of the property value, and cash reserves of 3-12 months of mortgage payments. The property must be an income-generating investment property that is rent-ready, and most lenders require a minimum DSCR ratio of 1.0, though 1.25 or higher unlocks the best terms. App Store

Breaking that down:

Credit score: Minimum FICO of 640-660 to qualify, with scores above 700 needed for optimal terms and higher LTV. Strong credit is one of your real assets here — use it. City of Philadelphia

Down payment: 20-25% down is standard. Unlike FHA loans, there is no low-down-payment option. This is the binding constraint for most investors — not income, not credit, just cash. App Store

Reserves: Lenders typically require 6 months of PITIA payments in liquid reserves after closing. So after your down payment, you need additional cash sitting in the bank. City of Philadelphia

The property: Must be an investment property — not your primary residence. DSCR loans can only be used for investment properties that generate rental income. Primary residences, second homes, and fix-and-flip properties do not qualify. App Store

What Are the Rates?

Current DSCR loan rates in 2026 typically range from 6.0% to 8.0% depending on credit score, LTV, and property cash flow. For comparison, conventional 30-year fixed rates for owner-occupied properties are sitting around 6.22% right now. City of Philadelphia

Expect an interest rate 1-2% higher than a standard conventional loan. That’s the cost of skipping the income documentation. For most investors, that tradeoff is completely worth it — paying 0.75% more on a property you can actually buy beats a conventional rate on a property conventional underwriting won’t approve. City of Philadelphia

One thing most articles skip: most DSCR loans have a prepayment penalty — typically a 5-year step-down — meaning if you sell or refinance quickly, you pay a fee. This matters if you’re planning a BRRRR where you want to refinance out of the hard money loan fast. Ask about prepayment terms before you commit. City of Philadelphia

Why DSCR Makes Sense for Philadelphia Specifically

Philadelphia has a few characteristics that make DSCR loans particularly relevant:

The price point is right. Philadelphia properties in Germantown, Brewerytown, and Port Richmond frequently fall in the $150k-$250k acquisition range — well within the DSCR loan minimum of $100k-$150k and far below the jumbo threshold. Redfin

Rental demand is steady. Philadelphia has a large renter population. Strong rental demand means your DSCR math is more likely to work — you can actually get the rent the appraiser needs to see.

Self-employed investors are common here. A lot of people doing deals in Philadelphia are running their own businesses, not collecting W-2s. DSCR was built for exactly this situation.

LLC ownership is supported. You can take out a DSCR loan in the name of an LLC to protect your personal assets. For investors building a portfolio, this is a big deal — it keeps liability separate and can keep the loan off your personal credit report. Utbf

DSCR and BRRRR: The Connection

If you’re doing a BRRRR deal — buy, rehab, rent, refinance, repeat — DSCR is often the refinance tool at the end.

Here’s why: after a flip or rehab, you’ve added value to the property. You want to pull cash out through a refinance. But if your personal income looks low on paper, conventional lenders won’t give you the cash-out refi you need.

DSCR doesn’t care. Some leading DSCR lenders allow refinancing as soon as the rehab is complete — without the 6-month seasoning period that conventional lenders require. Rent the property, show the lender the lease, and you can refinance based on the new rental income. BiggerPockets

That’s the whole BRRRR cycle working the way it’s supposed to.

The Honest Downside

DSCR loans are a great tool — but they’re not magic.

The down payment requirement is real. 20-25% on a $200k Philadelphia property is $40-50k cash, before closing costs and reserves. If you don’t have that sitting somewhere, DSCR doesn’t solve your problem.

The rate premium adds up over time. On a $180k loan, the difference between 6.5% and 8% is about $175/month — $2,100/year. Over five years, that’s over $10,000. Still worth it for most investors, but don’t ignore it.

And the property has to actually cash flow. Philadelphia’s property taxes can be significant, especially after a reassessment post-renovation. Run the full PITIA number — not just principal and interest — before you assume your DSCR will work.

Who DSCR Is Right For

DSCR loans are perfect for self-employed or freelance people, investors who’ve maxed out conventional financing at 10 properties, people who invest through LLCs, and anyone whose tax returns don’t reflect their actual financial strength. BiggerPockets

If that sounds like you — and honestly, it sounds like a lot of Philadelphia investors — DSCR is worth understanding before your next deal, not after you’ve already been turned down by a conventional lender.

Run your DSCR numbers below before you talk to a lender — know whether your deal qualifies before you pick up the phone.