Most real estate investors think about building a portfolio in one direction: buy more rentals, collect more rent, repeat.

That’s not wrong. But there’s a specific variation on that model that I keep coming back to — one that uses flipping strategically to eliminate debt on your rental properties, turning them into pure cash flow machines faster than most people expect.

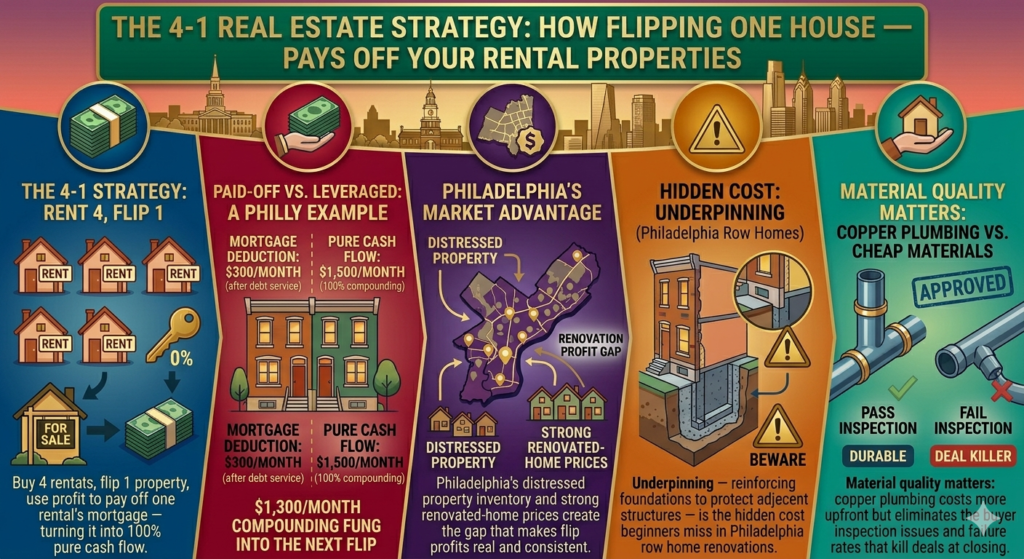

It’s called the 4-1 strategy. And once you understand the math, it’s hard to unsee.

The Basic Concept: 4 Rentals, 1 Flip

The real estate portfolio strategy works like this:

Step 1: Buy 4 rental properties. Finance them the normal way — conventional loan, DSCR loan, hard money into a refinance, whatever works for your situation. Each one has a mortgage. Each one generates some cash flow after expenses.

Step 2: Buy a 5th property — but this one is a flip, not a rental. Buy it distressed, renovate it, sell it at a profit.

Step 3: Take the profit from the flip and use it to pay off the mortgage on one of your 4 rental properties.

Step 4: That rental — now mortgage-free — generates 100% pure cash flow. Every dollar of rent that comes in goes straight to you, with no debt service eating into it.

Step 5: Repeat.

The math compounds fast. Once you have one paid-off rental, you use its cash flow to help fund the next flip. The next flip pays off a second rental. Two paid-off rentals fund the next one even faster. Each cycle accelerates the one after it.

Why This Works Better Than Just Buying More Rentals

The standard advice is to keep buying rentals and let the mortgages pay themselves off over 30 years. That works. But it’s slow — and in the early years, each rental property generates relatively thin cash flow because most of the rent goes to the mortgage.

The 4-1 real estate portfolio strategy short-circuits that timeline.

Instead of waiting 30 years for a mortgage to pay itself off, you use one strategic flip to eliminate one mortgage entirely — potentially in a year or two rather than three decades.

A paid-off rental generating $1,500/month in rent is a fundamentally different asset than a leveraged rental generating $200/month in cash flow after debt service. Same property. Same rent. But the paid-off version puts $1,300 more per month in your pocket.

That difference is what funds the next flip. Which pays off the next rental. Which funds the next flip faster.

The Philadelphia Application

This strategy maps particularly well onto Philadelphia’s market — and here’s why.

Philadelphia has a large inventory of distressed properties available at significant discounts through conventional channels, wholesalers, and tax sales. The flip side of the market — renovated properties in South Philly, Fishtown, Point Breeze, and surrounding neighborhoods — commands strong prices from buyers.

That gap between distressed acquisition cost and renovated sale price is where flip profit comes from. And Philadelphia’s gap is real and consistent enough to make the 4-1 strategy viable.

A rough Philadelphia example:

- 4 rental properties, each generating $300/month cash flow after expenses = $1,200/month total

- 1 flip: buy distressed at $80,000, renovate for $40,000, sell at $200,000

- Flip profit after costs: approximately $60,000-$70,000

- Use $60,000 to pay off the mortgage on one of the 4 rentals

- That rental now generates $1,200/month instead of $300/month

- Total portfolio cash flow: $300 × 3 + $1,200 = $2,100/month

One flip. One paid-off rental. Cash flow jumps from $1,200 to $2,100/month.

Do that again and you’re at $3,000+/month from the same 4 properties.

The Construction Side: What Actually Makes a Flip Profitable

Executing a flip well is the part most strategy content glosses over. The 4-1 strategy only works if your flips are actually profitable — which means your renovation has to come in on budget and on time.

Here’s what experienced developers who’ve worked on Philadelphia row homes and new construction actually focus on:

Lock in your scope before you start.

The four things to have nailed down before any work begins: the scope of work, the budget with contingency built in, the layout and measurements, and the target sale price. Changing any of these mid-project is expensive. Changing them after demolition has started is very expensive.

The contingency isn’t optional. Budget 10-20% above your contractor’s estimate. Something always comes up.

Underpinning matters more than most beginners realize.

In Philadelphia’s dense row home neighborhoods, your property shares walls or sits adjacent to neighboring structures. When you’re doing foundation work on a new build or a gut renovation that touches the foundation, the adjacent building’s structure can be affected.

Underpinning is the process of reinforcing the foundation in a way that protects neighboring structures. Skip it and you risk destabilizing an adjacent building — which creates legal liability, regulatory problems, and potentially catastrophic delays. It’s not glamorous work. It doesn’t show up in the finished product. But it’s the kind of thing that experienced developers budget for automatically, and beginners discover painfully.

Material quality has a long tail.

There’s a temptation in flips to use the cheapest materials that will pass inspection. Sometimes that’s the right call. But experienced developers who’ve seen the same properties cycle through the market multiple times tend to favor materials that hold up.

Copper plumbing over cheaper alternatives is one example that comes up consistently. The upfront cost difference is real. But copper lasts decades without the failure rates of cheaper options — and a buyer’s inspector who finds plumbing issues can unravel a deal at closing.

The calculus: materials that cost slightly more upfront but reduce callbacks, buyer objections, and future liability are almost always worth it in a flip targeting buyers with conventional financing.

Show up to the site.

This sounds obvious. It isn’t always practiced. Developers who aren’t on-site regularly find out about problems when they’re expensive to fix. Developers who check in frequently catch issues when they’re cheap to fix.

A framing mistake discovered during rough framing costs an afternoon. The same mistake discovered during drywall costs days. Discovered after finish work: potentially tear out and redo. The math on site visits is straightforward.

Putting It Together: The 4-1 as a Roadmap

The 4-1 real estate portfolio strategy isn’t a get-rich-quick framework. It’s a systematic approach to converting flip income into permanent cash flow by eliminating debt one property at a time.

For someone starting with limited capital, it provides a structured sequence: build a small rental base, execute flips to eliminate debt on those rentals, use the increased cash flow to fund more activity, repeat.

For someone already holding rentals with mortgages, it offers a path to accelerate debt elimination without waiting 30 years for mortgages to pay themselves off.

The flipping skill set — finding distressed properties, managing renovations, selling effectively — is learnable. The rental income that results from a paid-off property is permanent. The combination of those two things is what makes this strategy worth understanding.

Not financial advice — just someone doing a lot of research and asking a lot of questions.