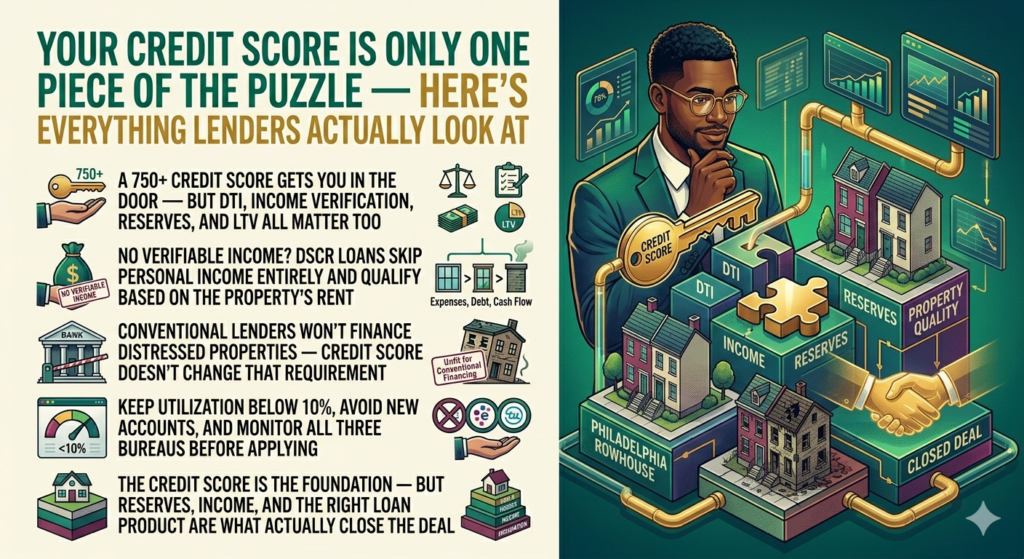

Your Credit Score Is Only One Piece of the Puzzle — Here’s Everything Lenders Actually Look At

Real estate loan credit score requirements are what most people fixate on. I did too — until I realized it’s just the beginning.

My scores are decent — around 750 on Experian and close to 800 on the others. I thought that was the hard part. I thought if your credit score was good, the rest would follow.

It turns out a good real estate loan credit score gets you in the door. What happens after that is a completely different conversation.

What Your Real Estate Loan Credit Score Actually Does

Your credit score is a three-digit number that tells lenders how reliably you’ve repaid debt in the past. For real estate lending, here are the general benchmarks:

- 760 and above: Best rates and terms available

- 720 to 759: Very good — most programs available

- 680 to 719: Good — some restrictions may apply

- 620 to 679: Fair — limited programs, higher rates

- Below 620: Difficult — hard money only, higher rates and stricter terms

A score in the 750 to 800 range puts you in a strong position for most loan programs. But it doesn’t mean approval is automatic.

What Lenders Look at Beyond Your Real Estate Loan Credit Score

This is the part most people don’t talk about.

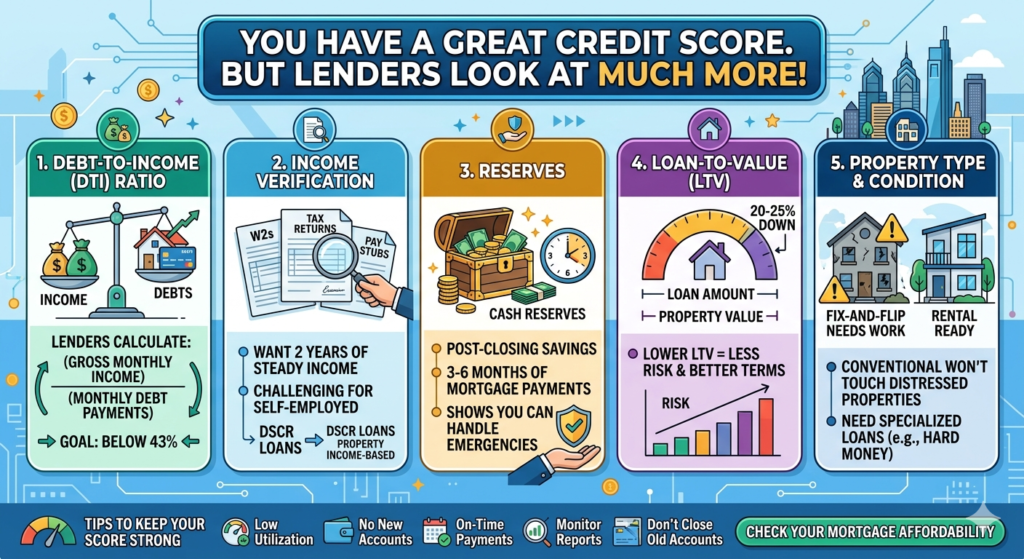

Debt-to-Income Ratio (DTI)

For conventional loans, lenders calculate how much of your gross monthly income goes toward debt payments. Most want a back-end DTI below 43%.

If you don’t have verifiable income — self-employed, between jobs, building something new — your DTI calculation gets complicated fast. This is exactly why DSCR loans exist. They skip the personal income calculation entirely and focus on the property’s income instead. Check the DSCR Loan Qualifier to see if a property qualifies based on rental income alone.

Income Verification

Conventional lenders want two years of tax returns, W-2s, or documented self-employment income. If you can’t show consistent, verifiable income, conventional financing becomes very difficult — regardless of your real estate loan credit score.

Reserves

Most lenders want to see cash left after closing. Typically 3 to 6 months of mortgage payments sitting in an account you own. An excellent credit score with an empty bank account will still get you declined.

Loan-to-Value (LTV)

Lenders look at how much you’re borrowing relative to the property’s value. Putting 20–25% down puts you in a much stronger position than 5% down — even with identical credit scores.

Property Type and Condition

Conventional lenders won’t touch distressed properties. If you’re buying a fix-and-flip, you need a loan product specifically designed for that — like a hard money loan or renovation loan. A perfect real estate loan credit score doesn’t change that requirement.

According to the Consumer Financial Protection Bureau, most conventional lenders cap DTI at 43% — but many prefer to see it below 36% for investment properties.

How to Keep Your Score Strong While Preparing to Invest

Since my scores are already in decent shape, my focus is on protecting them while I prepare for my first investment.

- Keep utilization low. Below 30% of your limits helps. Below 10% is even better.

- Don’t open new accounts unnecessarily. Every hard inquiry can temporarily lower your score. Avoid new credit applications before you’re ready to apply for a real estate loan.

- Pay everything on time. Payment history is the single biggest factor. One missed payment can drop a good score significantly.

- Monitor all three bureaus. Experian, Equifax, and TransUnion can have different information. Errors are more common than most people realize — dispute anything that looks wrong immediately.

- Don’t close old accounts. Closing an old card you don’t use can hurt your score by shortening your average account age.

Want to track your progress toward investment-ready credit? The Credit Score Improvement Tracker helps you monitor exactly where you stand.

What This Means for My Situation

My real estate loan credit score is not the problem. That’s genuinely useful to know.

What I’m working on now is the other pieces — building verifiable income, understanding which loan products match my situation, and finding the right deals so that when I’m ready to move, I can move quickly and confidently.

The credit score is the foundation. But a foundation alone doesn’t build anything. You still have to do the work.

Not financial advice — just someone doing a lot of research and asking a lot of questions.