Rent vs buy rule — the simplest math I’ve found for answering one of the most stressful questions in personal finance: am I throwing money away by renting?

I’ve rented in New York, New Jersey, DC, and now Philadelphia. I know what it feels like to hand over $1,800 a month and wonder if I’m just making someone else rich. And I know how complicated the rent vs buy decision feels when you factor in down payments, interest rates, maintenance costs, and everything else.

But this one calculation cuts through all of it.

What Is the Rent vs Buy Rule?

The rent vs buy rule gives you a monthly dollar figure that tells you whether renting or buying makes more financial sense at a given home price.

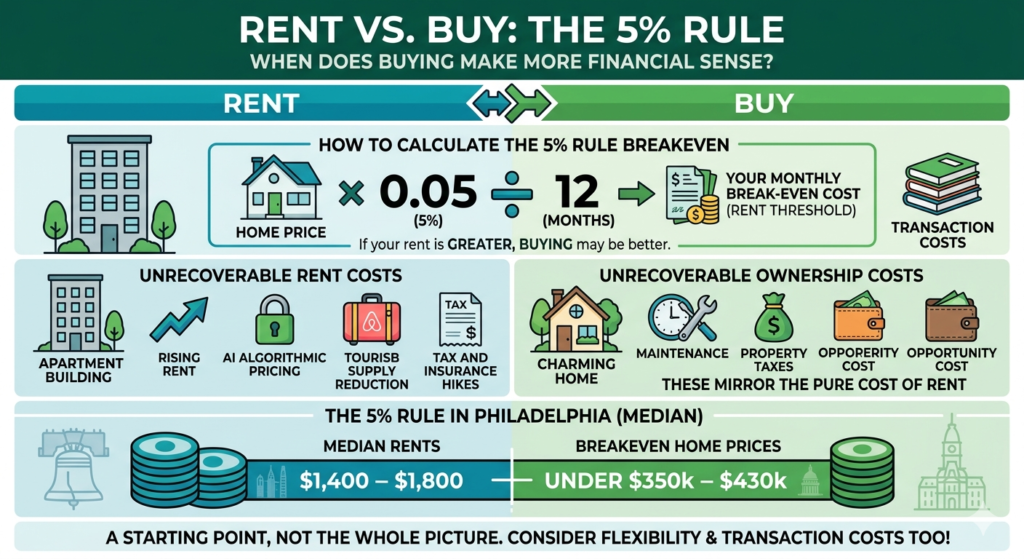

The formula:

(Home price × 0.05) ÷ 12 = Your rent vs buy rule breakeven number

Example: You’re looking at a $300,000 home in Philadelphia.

$300,000 × 0.05 = $15,000 $15,000 ÷ 12 = $1,250/month

If you’re currently paying more than $1,250/month in rent — buying that $300,000 home is likely the better financial move.

If you’re paying less than $1,250/month — renting might still make more sense, depending on your situation.

That’s it. One number. Immediate clarity.

Why Rent Keeps Going Up (And It’s Not Just Greed)

Before we get into when buying makes sense, it’s worth understanding why rent has become so brutal — because the reasons go deeper than most people realize.

Property taxes and insurance have exploded. Over the last five to six years, property taxes and landlord insurance premiums have increased dramatically in most markets. Landlords don’t absorb those costs — they pass them directly to tenants. When a landlord’s insurance bill jumps $3,000 a year, that $250/month has to come from somewhere.

Airbnb pulled rental supply off the market. Every home that became a short-term rental is one fewer home available for long-term renters. In cities and suburbs with high travel demand, Airbnb has meaningfully reduced the supply of available rental units — which pushes prices up for everyone else.

AI is optimizing rent in real time. Large property management companies now use algorithmic pricing tools that analyze occupancy data, local demand signals, and competitor pricing to set and adjust rents dynamically. The same way airlines price seats, some landlords now price apartments.

Remote work increased demand for space. When people started working from home full time, demand for larger units jumped. More demand, same supply, higher prices.

None of this is going away. Which is exactly why the rent vs buy rule deserves serious attention.

The Rent vs Buy Rule Applied to Philadelphia

Let me run the rent vs buy rule across a few real Philadelphia price points.

| Home Price | 5% Rule Breakeven | Buying Better If Rent Is… |

|---|---|---|

| $200,000 | $833/month | Above $833 |

| $300,000 | $1,250/month | Above $1,250 |

| $400,000 | $1,667/month | Above $1,667 |

| $500,000 | $2,083/month | Above $2,083 |

In Philadelphia, the median one-bedroom rent is somewhere in the $1,400–$1,800 range depending on the neighborhood. Which means for a significant portion of Philadelphia renters, the rent vs buy rule suggests buying is the better financial move — if they can qualify for financing.

What the Rent vs Buy Rule Is Actually Measuring

The 5% figure isn’t arbitrary. It’s a rough estimate of the total unrecoverable annual cost of owning a home:

- ~3% for the opportunity cost of your down payment (what that capital could earn invested elsewhere)

- ~1% for property taxes (rough average — varies significantly by location)

- ~1% for maintenance and repairs

These are the costs of ownership you never get back — the equivalent of rent in the ownership equation. Mortgage principal payments don’t count because you’re building equity.

The rent vs buy rule essentially asks: is my rent higher or lower than what it would cost me just to own this home, excluding the equity-building component?

What the Rent vs Buy Rule Doesn’t Account For

The rent vs buy rule is a starting point, not a final answer.

Appreciation. If you buy in a neighborhood where values are rising, your equity grows beyond what your mortgage paydown generates. The rent vs buy rule ignores this upside.

Flexibility. Renting gives you the ability to move without the friction of selling. If your job situation is uncertain or you might relocate, renting has real non-financial value.

Transaction costs. Buying and selling a home costs roughly 8–10% of the home’s value in total. If you’re not planning to stay for at least 3–5 years, those transaction costs can wipe out any financial advantage from buying.

Financing costs. The rent vs buy rule doesn’t factor in your specific interest rate. At 7% on a 30-year mortgage, your monthly payment is significantly higher than at 5%. The rule gives you a directional answer — your actual mortgage payment tells you the real number.

According to Census.gov, Philadelphia’s homeownership rate has consistently lagged the national average — driven in part by down payment barriers and qualifying income requirements that keep renters in the market longer than the rent vs buy rule math suggests they should be.

My Honest Take on the Rent vs Buy Rule

I’ve been renting my entire adult life in the U.S. And every time I’ve run the rent vs buy rule against what I was actually paying in rent, buying came out ahead on paper.

The barrier has always been the down payment and the qualifying income — not the monthly cost comparison.

Which is why I spend so much time on this blog studying the programs that actually lower those barriers: USDA loans, FHA financing, down payment assistance, house hacking. Because the rent vs buy rule math often points toward buying — it’s the upfront friction that keeps people in rentals longer than the numbers suggest they should be.

Use the Philadelphia Rent vs Buy Calculator to run your own full comparison — monthly costs, break-even timeline, and equity building over time — for any Philadelphia property you’re considering.

Not financial advice — just someone doing a lot of research and asking a lot of questions.