Rental Property Cash Flow: Is Your Philadelphia Rental Actually Making Money?

Rental property cash flow is the number most landlords never actually calculate. They look at rent versus mortgage and call it a day. That gap — between what they think they’re making and what they’re actually making — is where a lot of people quietly lose money for years.

I’ve talked to people here in Philadelphia who own rental properties and genuinely believe they’re cash flow positive. Some of them are right. A surprising number are not. The math is the difference.

What Most Landlords Get Wrong About Rental Property Cash Flow

The most common mistake: someone collects $1,500 a month in rent, pays $900 in mortgage, and concludes they’re making $600 a month in rental property cash flow.

They’re skipping four things that will absolutely cost them money.

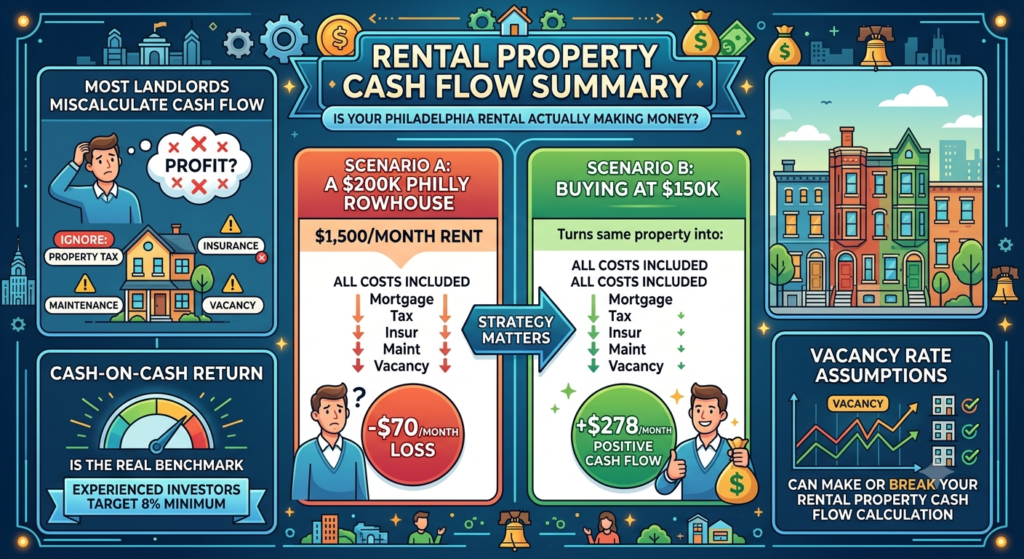

Property tax. In Philadelphia, property tax runs about 1.3% of assessed value annually. On a $200,000 property, that’s roughly $217 per month.

Insurance. Landlord insurance on a Philadelphia rental runs $80 to $120 per month depending on coverage.

Maintenance and repairs. Experienced investors budget 1% of property value per year. On a $200,000 property, that’s $167 per month.

Vacancy. Properties aren’t rented 12 months a year, every year. A conservative vacancy estimate for Philadelphia is 5% — about 18 days of lost rent per year.

Add all of that in, and that $600 a month looks completely different.

Rental Property Cash Flow: A Real Philadelphia Example

Let’s run the actual numbers.

You buy a two-bedroom rowhouse in West Philadelphia for $200,000. You put 20% down — $40,000 — and finance $160,000 at 6.5% on a 30-year mortgage.

Monthly mortgage: $1,011 Property tax: $217 Insurance: $100 Maintenance reserve: $167 Total monthly costs: $1,495

You rent it for $1,500/month. After 5% vacancy, effective monthly rent is $1,425.

Rental property cash flow: $1,425 − $1,495 = −$70/month.

You’re losing $70 a month on a property you thought was making money.

When Rental Property Cash Flow Actually Works

The same property at a lower purchase price tells a completely different story.

Buy that same West Philly rowhouse for $150,000 — achievable at a sheriff sale, through aggressive negotiation, or with a distressed property.

Monthly mortgage on $120,000 at 6.5%: $759 Property tax: $163 Insurance: $100 Maintenance reserve: $125 Total monthly costs: $1,147

Effective monthly rent after vacancy: $1,425

Rental property cash flow: $1,425 − $1,147 = +$278/month.

Annual cash flow: $3,336 Cash-on-cash return on $30,000 down: 11.1%

The difference between those two scenarios is $50,000 in purchase price. This is why buying right matters more than almost anything else.

Cash-on-Cash Return: The Number That Actually Matters

When I’m evaluating rental property cash flow, cash-on-cash return is the metric I care most about. It tells you what percentage return you’re getting on the actual cash you put in — down payment plus renovation costs.

Most experienced investors look for a minimum of 8% cash-on-cash return. Below 5%, you have to ask whether the hassle of being a landlord is worth it compared to putting that money somewhere else.

Negative cash-on-cash return means you’re subsidizing your tenant’s housing. That’s not investing.

Rental Property Cash Flow and Vacancy: The Number That Changes Everything

Your vacancy rate assumption changes your entire rental property cash flow calculation. In strong rental markets, vacancy is low. In weaker markets or with difficult tenants, it runs much higher.

Philadelphia has strong rental demand in most neighborhoods right now — but some blocks are stronger than others. Know your specific neighborhood’s vacancy reality before you finalize your numbers.

How to Calculate Your Rental Property Cash Flow

I built a free Rental Property ROI Calculator so you can run the real numbers on any property — including every cost most landlords forget.

Enter your purchase price, down payment, monthly rent, expenses, interest rate, and vacancy rate. It calculates your true monthly cash flow, annual cash flow, and cash-on-cash return — and tells you whether the deal hits the 8% benchmark experienced investors use.

Run your current property through it. You might be surprised. You can also run your DSCR numbers here.

Not financial advice — just someone doing a lot of research and asking a lot of questions.