Seller finance negotiation is nothing like negotiating a bank loan. When you get a bank loan, you fill out the application, submit your documents, and wait to find out if you qualify — at whatever rate the bank sets. You accept or walk away.

Seller finance negotiation flips that entirely. No application. No underwriter. No rate sheet. Just two people negotiating a deal. And that means every single term is on the table.

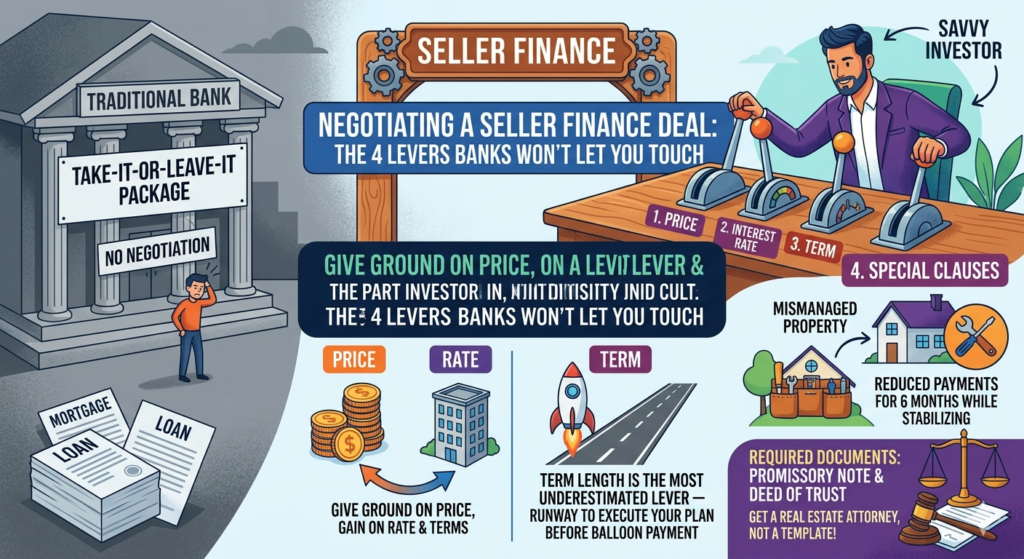

Most people who learn about seller financing focus on the “no bank” part. What they miss is the creative part — the four distinct levers you can pull, and how combining them makes deals work when nothing else would.

The 4 Levers in Seller Finance Negotiation

Lever 1: Price

Price is where most seller finance negotiations start. And it’s often where you give ground — intentionally.

Here’s the counterintuitive move: if a seller wants $1.2M and the property is worth $1.1M, you might offer $1.2M. Full asking price. Maybe even above.

Why? Because you’re going to make it up on the other three levers.

A seller who gets their price is a motivated seller financing partner. You’ve solved their ego problem. Now you negotiate the rate, term, and clauses — and that’s where you actually make the deal work financially.

Price is the lever you give. The other three are the levers you take.

Lever 2: Interest Rate

Banks give you the market rate. Right now that’s somewhere in the 7–8% range for investment properties. You take it or leave it.

With seller finance negotiation, you can propose any rate. Including rates that don’t exist anywhere in the current market.

A seller who owned a property for 30 years and carries a small or zero mortgage doesn’t need your interest payments to survive. What they need is a steady income stream, a fair price, and someone they trust to take care of the asset.

If you give them the price they want, they might accept 4% interest. Or 3.5%. Or interest-only payments for the first few years. None of these are available at any bank in 2026. But they’re available in seller finance negotiation.

The math: the difference between a 7.5% bank loan and a 3.5% seller finance note on a $1M property is roughly $3,300/month in debt service. That’s $39,600/year staying in your pocket as cash flow instead of going to a bank.

Lever 3: Term

The term is how long you have before you need to refinance or pay off the balance.

Most seller finance deals include a balloon payment — the full remaining balance comes due at the end of the term. This is the lever most beginners underestimate — and the one that can sink a deal if you get it wrong.

The principle: give yourself enough time to actually execute your plan.

If you’re buying a value-add property that needs 18 months to stabilize before it qualifies for conventional financing — negotiate a 5 or 7 year term, not 3. If you get a 3-year balloon and stabilization takes longer than expected, you’re scrambling to refinance a property that isn’t performing yet.

A seller who’s getting their price and a reasonable interest rate is usually flexible on term. Ask for 7 years. Ask for 10. The worst they can say is no.

And here’s something worth noting in seller finance negotiation: a longer term is actually a selling point for the right seller. An elderly landlord who wants steady monthly income for the next decade doesn’t want a 3-year balloon any more than you do. Align your interests.

Lever 4: Special Clauses

This is where seller finance negotiation gets genuinely creative — and where deals that look impossible on paper become possible in practice.

Special clauses are custom provisions negotiated into the promissory note. They can address almost any timing or cash flow problem your specific deal has.

The most useful: deferred or reduced payments in the early months.

You’re buying a 38-unit apartment building. It’s been mismanaged — high vacancy, below-market rents, deferred maintenance. The current NOI doesn’t cover normal debt service. But if you have 6 months to stabilize it, the numbers will work.

You negotiate a clause: for the first 6 months, your monthly payment to the seller is reduced by $3,000. That’s $18,000 in breathing room during exactly the window you need it most. Once stabilization ends and rents are up, normal payments begin — and now the property actually supports them.

Other special clauses worth knowing:

- Interest-only period — Pay only interest for the first 1–3 years, then shift to principal and interest. Reduces your payment significantly during the value-add phase.

- No prepayment penalty — The right to pay off the seller’s note early without penalty. Always ask for this.

- Right of first refusal on the note — If the seller ever wants to sell your promissory note to a third party, you get the first option to buy it yourself, often at a discount.

- Subordination clause — Lets you bring in additional financing later without triggering default on the seller note.

The Mindset Shift Behind Successful Seller Finance Negotiation

Most buyers ask: “What price does this property need to be at for the deal to work?”

Sophisticated seller finance negotiation asks: “Given the seller’s price, what combination of rate, term, and clauses makes this deal work?”

These are fundamentally different questions — and they lead to completely different outcomes.

If a seller wants $1.4M for a property worth $1.2M on the open market — a conventional buyer says no. A seller finance negotiation says: “Okay, $1.4M. But at 3.5% interest, 7-year term, with 6 months of reduced payments while I stabilize the asset. Now let’s run the numbers.”

Sometimes it still doesn’t work. But a lot of the time, it does.

The Legal Documents You Need After Seller Finance Negotiation

Seller financing isn’t a handshake deal. It requires proper legal documentation — and this is not the place to cut corners.

Promissory Note — This is the core document. It spells out exactly how much is owed, the interest rate, the payment schedule, the term, the balloon payment date, and any special clauses you’ve negotiated.

Deed of Trust (or Mortgage, depending on state) — This secures the promissory note against the property. If you default, the deed of trust gives the seller the legal right to foreclose and take the property back.

Get a real estate attorney to draft these. On a $1M+ deal, proper legal documentation is not optional. Template documents from the internet are not sufficient — your state’s specific foreclosure laws and recording requirements matter.

According to the Consumer Financial Protection Bureau, seller financing arrangements are legally binding contracts with the same enforceability as bank loans — and improperly drafted documents can leave both parties without recourse if something goes wrong.

Putting Seller Finance Negotiation Together

The four levers work together. You rarely pull just one.

A deal where you pay full asking price might work because you negotiated a 3.5% interest rate and a 7-year term with a 6-month reduced payment clause. A deal where you negotiate the price down might not need as much creativity on the other levers.

Read the seller. Understand what they actually need. Sellers who need cash flow care most about the interest rate and payment schedule. Sellers who want to be done care most about price and simplicity. Sellers who are nervous about your ability to execute care most about term length and security.

Build the structure that gives them what they need while giving you what you need. That’s the deal.

Use the Subject To Calculator to model your seller finance negotiation numbers — plug in price, rate, and term to see exactly what your monthly payment and cash flow look like before you sit down at the table.

Not financial advice — just someone doing a lot of research and asking a lot of questions. Consult a real estate attorney before drafting or signing any seller financing documents.