I’ll be honest — when I first saw this, I thought it was clickbait.

$750. That’s it. For a $350,000 four-unit property.

But I looked into it. And the math actually works. It’s not a scam, it’s not a loophole, and it’s not something only rich people with connections can do. It’s a combination of three financial tools that most people have never heard of — stacked together in exactly the right order.

Let me break it down.

The Deal

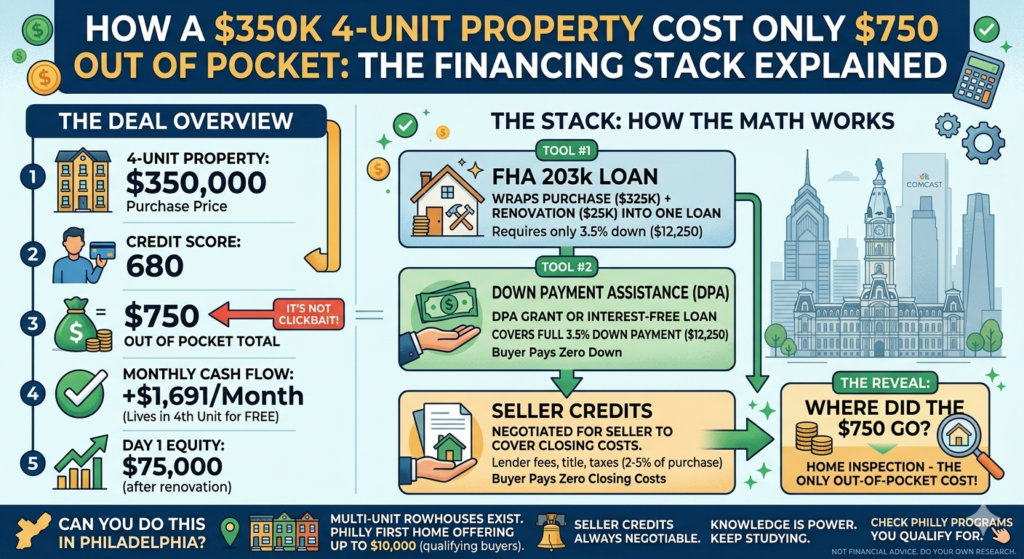

- 4-unit property, purchase price: $350,000

- Buyer’s credit score: 680

- Money out of pocket: ~$750

- Monthly mortgage (PITI): ~$2,959

- Monthly rental income from 3 units: $4,650

- Monthly cash flow: +$1,691 — while living in the fourth unit for free

- Instant equity after renovation: $75,000

So this person bought a house, lives in it for free, makes $1,691/month, and gained $75K in equity on day one.

How?

Tool #1: FHA 203k Loan

A regular mortgage only lends you money to buy the house. The FHA 203k does something different — it wraps the purchase price AND renovation costs into one single loan.

In this deal: $325K purchase + $25K renovation = $350K total, one loan, one payment.

The other thing about FHA loans: the down payment is only 3.5%. On $350K, that’s $12,250. Still a lot of money if you don’t have it — which is where tool #2 comes in.

Tool #2: Down Payment Assistance (DPA)

DPA programs exist specifically to cover down payments for buyers who qualify. Some are grants (free money). Some are interest-free loans. Either way, someone else pays your down payment.

In this deal: the full $12,250 down payment was covered by a DPA program. Buyer paid zero.

Philadelphia has DPA programs too — Philly First Home offers up to $10,000 for qualifying first-time buyers. These programs are real, they’re funded, and most people have no idea they exist.

Tool #3: Seller Credits

When you buy a house, there are closing costs on top of the purchase price — lender fees, title fees, taxes, all kinds of stuff. Usually 2–5% of the purchase price.

Seller credits means you negotiate for the seller to cover those costs instead of you. The seller agrees, usually in exchange for a slightly higher offer price or because they want to close quickly.

In this deal: closing costs were covered by seller credits. Buyer paid zero.

So Where Did the $750 Go?

Home inspection. That’s basically it.

Down payment → DPA covered it. Closing costs → Seller covered it. Renovation → Built into the 203k loan. Inspection → $750 out of pocket.

That’s the whole stack.

Can You Do This in Philadelphia?

Pieces of this strategy absolutely exist in Philadelphia:

- FHA 203k loans work here — and Philly’s older rowhouse stock is exactly what this loan was designed for

- DPA programs — Philly First Home, PHFA programs, HOME program

- Seller credits — always negotiable, especially in slower markets or motivated seller situations

- Multi-unit properties — Philadelphia has tons of duplexes, triplexes, and 4-units, especially in neighborhoods that are still underpriced

The 4-unit piece is important. FHA allows owner-occupants to buy up to 4 units with the low 3.5% down payment. Above 4 units, you need commercial financing with much higher requirements. So the 4-unit is the sweet spot.

The Honest Caveat

FHA 203k loans require income verification. Stable employment history. DTI (debt-to-income ratio) under 43%. This isn’t a no-income, no-job loan — you need to qualify.

But if you have decent credit, stable income, and you’re willing to live in one unit while renting the others? This strategy is real and it works.

I’m still studying this. I’m not there yet. But every time I dig into one of these deals, I find another tool I didn’t know existed — and I realize the gap between where I am and where I want to be is mostly just knowledge.

That’s why I keep studying.

Check Philadelphia Programs You Might Qualify For:

Not financial advice — just someone who went down a rabbit hole and came back with a lot of notes.