If you’ve ever thought about building a house from scratch, I want to talk you out of it. Not because it’s impossible — but because there’s a smarter way to get a brand new home that almost nobody talks about.

It’s called a spec home. And once you understand how it works, the “build your own” dream starts to look a lot less appealing.

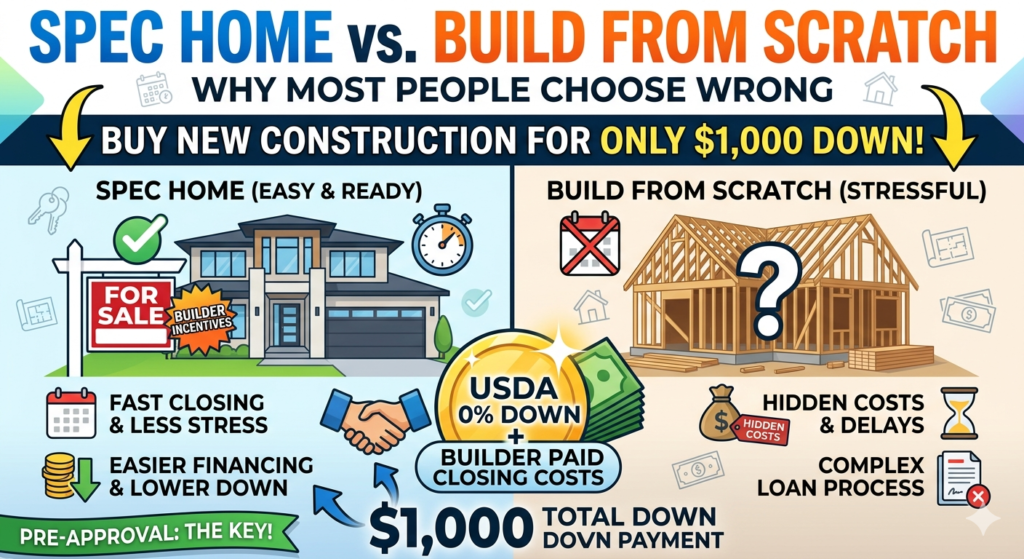

What Is a Spec Home?

A spec home — short for speculation home — is a house that a builder starts constructing before they have a buyer. They’re betting (speculating) that someone will want to buy it when it’s done or nearly done.

This happens constantly. Builders need to keep their crews working. They can’t wait around for a custom buyer to show up before they break ground. So they build ahead of demand — and then sell.

The result: there are always spec homes in various stages of completion sitting in new developments, waiting for a buyer.

And those buyers have more leverage than most people realize.

Why Building From Scratch Is Harder Than It Looks

Before we get into why spec homes are a better play for most buyers, let’s talk about what custom construction actually involves — because the marketing around it leaves out a lot.

The base price is never the final price.

Every builder starts with a base price that covers the most basic version of the home. The moment you start making decisions — flooring upgrades, lighting packages, hardware finishes, kitchen cabinet levels — the number climbs. Fast. It’s not unusual for buyers to add $20,000 to $50,000 in upgrades before they’ve even thought about landscaping.

Impact fees are real and nobody warns you.

Depending on where you’re building, local municipalities charge impact fees — essentially a tax for the infrastructure burden your new home creates (roads, schools, utilities). In some California counties, these run $15,000 to $20,000. In Pennsylvania, they vary by municipality but can add thousands to your closing costs.

These fees are often buried in the fine print of a construction contract. Read everything carefully.

Construction loans are complicated.

To finance a custom build, you typically need either to own the land outright or have significant equity to bring to the table. Construction loans work differently than mortgages — you draw funds in stages as construction progresses, you pay interest only during the build phase, and then the loan converts to a permanent mortgage at completion.

The paperwork is intensive. The timeline is uncertain. Cost overruns are common. And if you’re not financially experienced with real estate transactions, managing a construction loan while also managing a builder relationship is genuinely stressful.

For a first-time buyer or early investor, it’s a lot to take on.

The Spec Home Advantage

Here’s where it gets interesting.

When a builder has a spec home sitting at 60%, 80%, or 100% completion without a buyer, they have a problem. Every month that home sits unsold is a month they’re carrying construction loan interest. They want it off their books.

That urgency creates negotiating opportunity for you.

What you can negotiate on a spec home:

Closing costs. This is the big one. Builders will often agree to cover some or all of your closing costs in exchange for a clean offer at or near their asking price. On a $350,000 home, closing costs might run $8,000 to $12,000 — and if the builder absorbs those, your cash-to-close drops dramatically.

Finish selections. If the home isn’t fully complete, you may still be able to choose flooring, countertops, paint colors, or fixtures. You’re getting a semi-custom home without paying custom prices or managing the build timeline yourself.

Price. If the home has been sitting for a while, there’s room to negotiate on price too — especially if the builder is carrying multiple unsold units.

Timeline. A spec home that’s already framed and nearly complete might close in 6 to 8 weeks. Compare that to 12 to 18 months for a custom build from scratch. For someone renting and ready to move, that speed has real financial value.

How to Buy a New Spec Home for Around $1,000 Out of Pocket

This is where USDA financing changes the math entirely.

The USDA loan — backed by the U.S. Department of Agriculture — offers 100% financing for homes in eligible areas. No down payment. The program is designed for low-to-moderate income buyers purchasing in rural or suburban areas that meet USDA’s geographic criteria.

USDA loan basics:

- Down payment: 0%

- Income limit: roughly $120,000 for a household of 4 (varies by county)

- Credit score: 620+ recommended

- Property must be in a USDA-eligible area (check eligibility at usda.gov)

- Must be your primary residence

The $1,000 scenario:

If you’re buying a spec home using USDA financing, and you negotiate the builder to cover closing costs — here’s what your out-of-pocket looks like:

- Earnest money deposit: ~$500

- Home inspection: ~$400–500

- Miscellaneous: ~$100–200

- Total out of pocket: approximately $1,000

You’re closing on a brand new home. No down payment. No closing costs. Just the deposit and inspection.

This isn’t a loophole. It’s two legitimate programs — USDA financing and builder-paid closing costs — working together in the way they were designed to work.

The catch: USDA eligibility is geographic. Not every Philadelphia suburb qualifies. You’d need to check specific addresses or zip codes against USDA’s eligibility map. Areas like parts of Chester County, Montgomery County, and Bucks County have USDA-eligible pockets worth exploring.

What About FHA?

If the home or location doesn’t qualify for USDA, FHA is the next option.

FHA requires 3.5% down — so on a $300,000 spec home, that’s $10,500. Still relatively low compared to conventional financing. And if you negotiate the builder to cover closing costs, you’re only bringing the down payment to the table.

FHA doesn’t have the geographic restriction that USDA does, which makes it more flexible for suburban Philadelphia locations.

How to Find Spec Homes in Philadelphia’s Suburbs

New construction activity in the Philadelphia metro area is concentrated in the outer suburbs — Chester County, Montgomery County, Bucks County, parts of Delaware County. These are the areas where builders are actively putting up spec inventory.

Where to look:

- Zillow and Realtor.com: Filter by “New Construction” and look for homes listed as available now (not “pre-sale” or “to-be-built”) — those are spec homes

- Builder websites directly: Ryan Homes, NVR, Pulte, Toll Brothers, and regional builders all list available inventory on their sites

- Drive new developments: If you see active construction, stop in at the model home and ask what’s available now and what the builder’s incentives are for quick-close buyers

- Ask about incentives: Builders run promotions — especially at the end of a quarter when they’re trying to hit sales numbers. End of March, June, September, and December are often the best times to ask

The Hidden Negotiating Advantage of Being Ready

Builders love buyers who are ready to move quickly. If you have your USDA or FHA pre-approval letter in hand, you’ve already done most of the work. You’re not a maybe — you’re a real buyer.

That pre-approval changes how a builder’s sales rep talks to you. You go from “someone browsing” to “someone we should close.” And that’s when the conversation about closing cost coverage and finish selections gets real.

Get pre-approved before you start shopping. It costs nothing and changes everything about how the conversation goes.

Not financial advice — just someone doing a lot of research and asking a lot of questions. USDA eligibility and loan terms change — verify current requirements with an approved USDA lender before making any decisions.