Nobody talks about this part.

You see the highlight reels — the groundbreaking photos, the “I quit my 9-to-5” captions, the finished product looking glossy and perfect. What you don’t see is what happens when an unexpected $30,000 invoice lands on your desk ten days into a $1.4 million development project.

I came across a video recently where a guy documented exactly that moment. And honestly, it was more useful to me than any success story I’ve watched.

The Setup

He’s a regular guy who decided to bet on himself. A $1.4 million real estate development project — his way out of the 9-to-5 grind. Day 10 of construction, he’s standing next to an excavator on site, feeling good.

Then he gets back to the office.

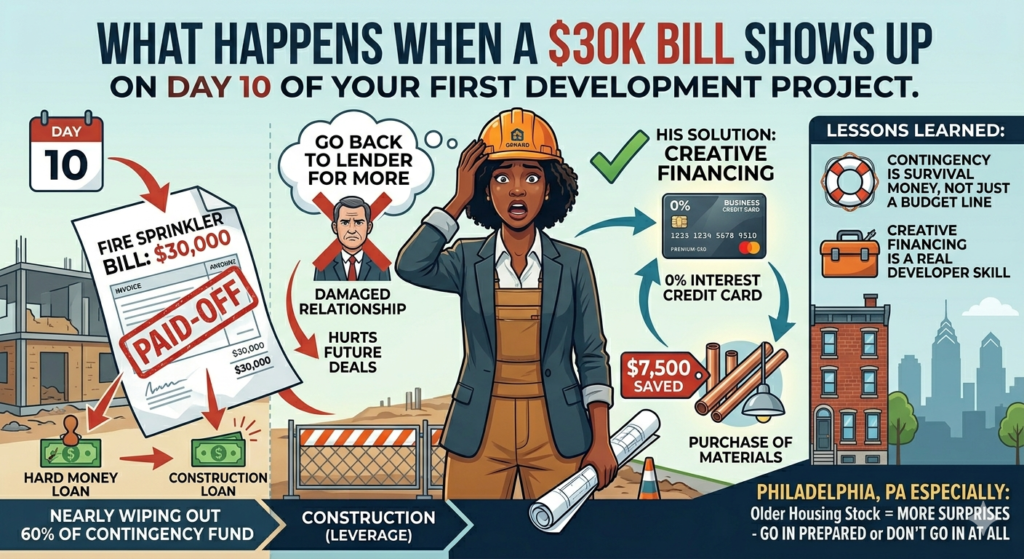

Waiting for him: a bill for fire sprinkler system installation. $30,000. Unplanned.

That single line item was about to eat through 60% of his entire contingency fund. Two weeks in.

Why He Couldn’t Just Ask the Lender for More Money

This is the part that really got me.

The obvious move seems like — just go back to your construction lender and ask for more funds, right?

Wrong. Going back to your lender two weeks into a project asking for additional money is a massive red flag. It signals that you didn’t underwrite the deal properly, that you don’t know what you’re doing, and it can seriously damage your relationship with that lender for future projects.

In real estate development, your lender relationships are everything. You burn that bridge on project one, and project two gets a lot harder to finance.

So he had to find another way.

The “Loophole” He Found

After going through his budget line by line, he landed on a creative solution — a 0% interest business credit card with a 12-month promotional period.

The idea: use the card to finance one of his upcoming large purchases outside of the construction loan. This kept his lender relationship intact, freed up cash within the project budget, and gave him 12 months to pay it back interest-free.

By routing that purchase through the card instead of the construction loan, he also saved around $7,500 — roughly 10% on a $75,000 purchase — which helped offset part of the sprinkler bill.

Smart? Yes. Perfect solution? Not quite.

At the end of the video he’s honest about it — he still hasn’t fully closed the gap. He’s still looking for more savings. The problem isn’t solved, just managed.

What This Actually Teaches You About Development

A few things I took away from watching this:

1. Contingency isn’t optional — it’s survival money. Standard advice is 10-15% contingency on any development budget. This guy had some set aside, and it still almost wasn’t enough. One surprise line item nearly derailed the whole thing.

2. Protecting lender relationships matters as much as the deal itself. He could have solved the immediate problem by going back to the lender. He chose not to — because he was thinking about deals two and three, not just deal one. That’s the mindset shift from investor to developer.

3. Creative financing is a real skill. A 0% business card isn’t glamorous. It’s not the stuff of YouTube thumbnails. But it saved his project timeline and his lender relationship at the same time. Knowing your financing options — all of them — is what keeps a project moving when things go sideways.

4. Things will go sideways. Fire sprinklers. Soil issues. Permit delays. Material cost increases. Something unexpected will happen on every project. The question isn’t whether you’ll face a surprise — it’s whether you have the cash, the creativity, and the relationships to absorb it.

Philadelphia Angle

If you’re thinking about development in Philadelphia specifically, this story hits differently.

Philly’s older housing stock means more surprises during construction — lead pipes, knob-and-tube wiring, foundation issues that don’t show up until you’re already in the ground. The inspection and permitting process through L&I can also throw curveballs that affect your timeline and budget.

Which means your contingency needs to be real money, not just a line on a spreadsheet.

I’m not saying don’t do it. I’m saying go in with eyes open — and maybe apply for that 0% business card before you need it.

Not financial advice — just someone doing a lot of research and asking a lot of questions.