I keep coming across this term — 1031 exchange — and every time I do, experienced investors talk about it like it’s one of the most powerful tools in real estate. So I finally sat down and actually learned what it is.

Here’s what I found, explained the way I wish someone had explained it to me.

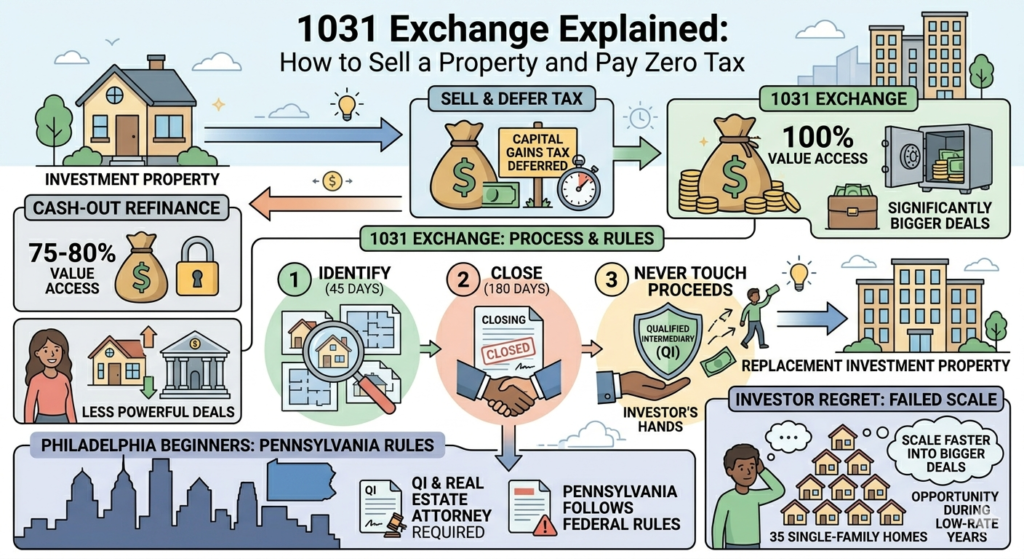

What Is a 1031 Exchange?

A 1031 exchange (named after Section 1031 of the IRS tax code) lets you sell an investment property and defer paying capital gains tax — as long as you reinvest the proceeds into another investment property.

In plain English: you sell a property, make a profit, and instead of giving a chunk of that profit to the IRS, you roll it into your next deal. Tax deferred. Not tax free forever — but deferred, potentially indefinitely if you keep exchanging.

For real estate investors, this is a big deal.

Why It Matters — The Numbers

Here’s where it clicked for me.

Say you own a rental property worth $500,000. You originally paid $300,000 for it, so you’ve got $200,000 in gains. If you sell normally, you’d owe capital gains tax on that $200,000 — potentially 15% to 20% federal, plus state taxes. That’s $30,000 to $40,000+ going to taxes before you can reinvest.

With a 1031 exchange, that money stays in play. All $200,000 goes into your next deal instead of to the IRS.

Over time, that compounding effect is massive.

Refinance vs. Sell — Which Gets You More?

This is something I learned from an investor who owned 35 single-family homes and looked back on his strategy with some regret.

He explained it this way:

When you refinance (the BRRRR strategy), you can typically pull out about 75% to 80% of your property’s value as cash. You keep the property, which keeps cash flowing — but you’re limited in how much equity you can access.

When you sell, you get 100% of the value. That extra 20% might not sound like much, but when you’re talking about a $500,000 property, that’s an additional $100,000 to deploy into your next deal.

His regret: when interest rates were 2.5% to 3%, he held onto his 35 homes instead of selling some and using a 1031 exchange to move into bigger deals. He could have scaled much faster. He didn’t — because selling felt scary, and holding felt safe.

“Holding everything isn’t always the right move” is a lesson I keep hearing from experienced investors. It was interesting to hear someone say it with real regret behind it.

How a 1031 Exchange Actually Works

The mechanics matter here because there are strict rules. Miss a deadline and you lose the tax deferral.

Step 1: Sell your property. The proceeds go to a Qualified Intermediary (QI) — a third party who holds the money. You cannot touch the cash yourself or the exchange is disqualified.

Step 2: Identify your replacement property within 45 days. You have 45 days from the sale to identify potential replacement properties in writing. You can identify up to three properties.

Step 3: Close on the replacement property within 180 days. You have 180 days total from the sale to close on the new property.

Step 4: The replacement property must be equal or greater in value. To defer all capital gains, the new property needs to be worth at least as much as the one you sold. If you trade down in value, you pay taxes on the difference.

What Qualifies?

A few important rules:

- Both properties must be held for investment or business purposes. Your primary residence doesn’t qualify.

- It must be like-kind property — but “like-kind” is broader than it sounds. You can exchange a single-family rental for a multifamily building, or a duplex for a commercial property. As long as both are investment real estate, it generally qualifies.

- You need a Qualified Intermediary. This isn’t optional — it’s a legal requirement.

When Does It Make Sense to Sell Instead of Refinance?

Based on what I’ve been learning, selling + 1031 makes more sense when:

- You want to scale up significantly — move from single-family to multifamily, or from small multifamily to commercial

- Your property has appreciated a lot and you want to access more than 80% of its value

- You’ve found a better deal in a better market

- The property has become difficult to manage and you want out

Refinancing makes more sense when:

- You want to keep the asset and its cash flow

- Rates are favorable enough that the math works

- You don’t have a clear next deal to move into

Neither is always right. It depends on where you are in your investing journey and what your next move is.

What This Means for a Beginner Like Me

I’m not selling anything yet — I don’t own anything yet. But understanding the 1031 exchange changes how I’m thinking about investing from the start.

It means I shouldn’t just think about buying and holding forever. I should think about each property as a stepping stone — something that builds equity, generates cash flow, and eventually might fund a bigger deal through a tax-smart exit.

That’s a different mindset than “buy a rental and collect checks.” And I think it’s a more accurate picture of how experienced investors actually build wealth over time.

For Philadelphia investors specifically — Pennsylvania doesn’t have its own 1031 exchange rules separate from federal, so the federal rules apply. But you’ll still want a local real estate attorney and a Qualified Intermediary who knows the Philly market when you’re ready to execute one.

Not financial advice or legal advice — just someone doing a lot of research and asking a lot of questions.