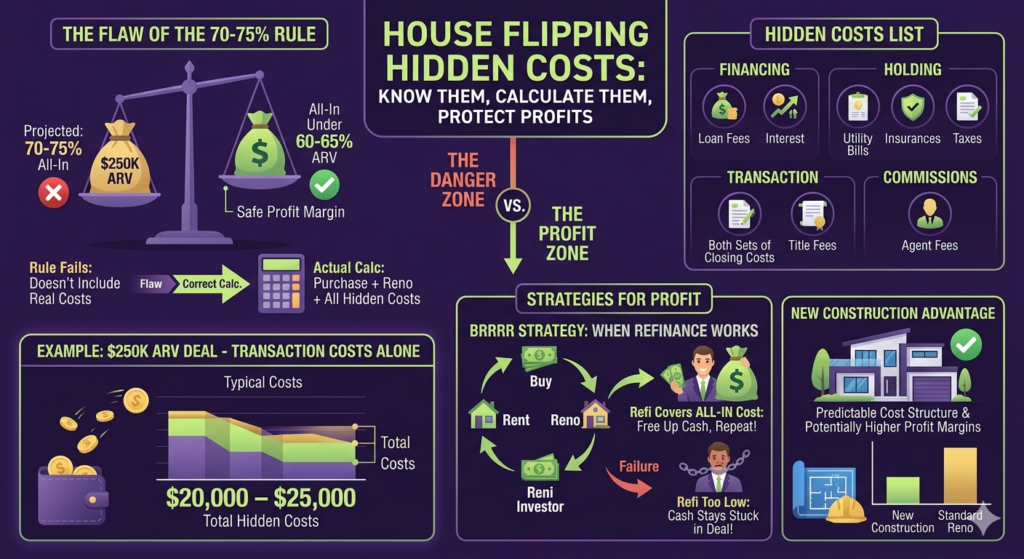

I used to think the 70% rule was the golden ticket to a profitable flip. Buy at 70% of ARV, subtract repairs, done. Easy math, right?

Except it’s not. And the more I dig into house flipping hidden costs, the more I realize how many investors — including people who’ve done this before — are getting squeezed on deals they thought were solid.

Let me walk you through what I’ve been learning.

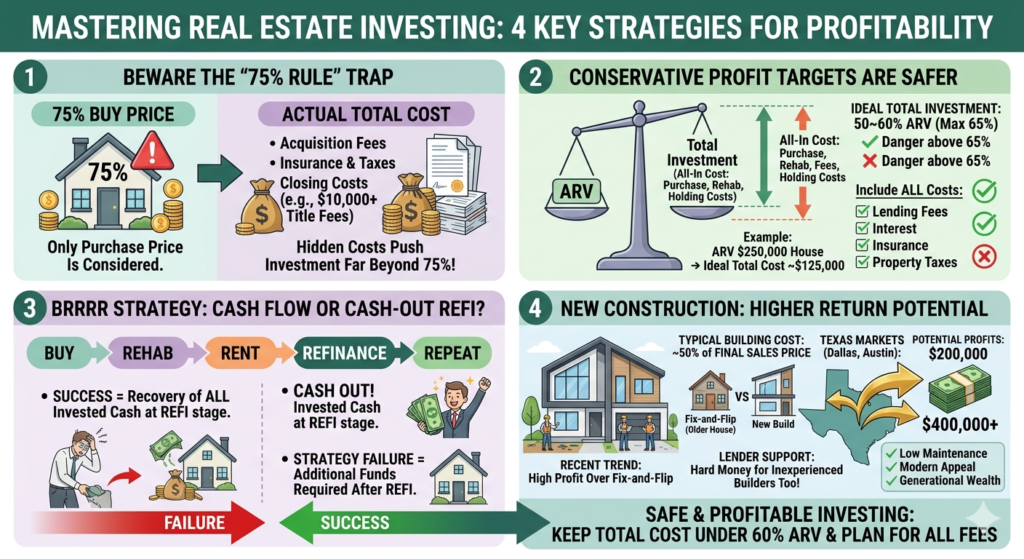

The 75% Rule Trap Nobody Talks About

You’ve probably heard of the 70% rule. But some investors stretch it to 75%, thinking they have a little more cushion. Here’s the problem: by the time you add up all the house flipping hidden costs that come with buying and selling a property, that “cushion” disappears fast.

We’re talking about things like:

- Acquisition costs (inspection, appraisal, title search)

- Title company closing costs on the buy side — often $3,000–$5,000+

- Title company closing costs on the sell side — another $5,000–$10,000+

- Holding costs (insurance, property taxes, utilities)

- Loan origination fees and points

- Real estate agent commissions on the sale side (typically 5–6%)

Add all of that up and your “75% deal” is suddenly an 85–90% deal. That’s where flips go sideways.

What Your All-In Cost Should Actually Be

This is the number that matters: your all-in cost — every single dollar you spend from contract to closing on the sale side.

Based on what I’ve been researching, the target range for a profitable flip is:

- Ideal: 50–60% of ARV

- Maximum: 65% of ARV

So if a house has an ARV of $250,000, your all-in cost should ideally land around $125,000–$150,000. And that includes everything — purchase price, rehab, loan fees, interest, insurance, taxes, and both sets of closing costs.

At 65% ($162,500 all-in on a $250K ARV deal), you’re cutting it close. At 75%+, you’re gambling.

House Flipping Hidden Costs Most Beginners Miss

This is where I see a lot of first-timers get burned. They calculate purchase price + rehab and stop there. Here’s what actually needs to go into the math:

Financing costs:

- Loan origination points (1–3% of loan amount)

- Monthly interest on hard money loans (typically 10–14% annualized)

- Draw fees if you’re using a construction draw schedule

Holding costs:

- Homeowner’s insurance (you need a vacant property policy — different from regular HO insurance)

- Property taxes (prorated for however long you hold it)

- Utilities if you’re keeping them on during rehab

Transaction costs:

- Title insurance (both lender’s and owner’s policy)

- Closing costs on the purchase side

- Agent commissions on the sale (if you’re not selling yourself)

- Closing costs on the sale side — title company fees, transfer taxes, etc.

According to BiggerPockets, transaction costs alone can run 8–10% of the sale price when you factor in both sides. That’s $20,000–$25,000 on a $250K deal. If you weren’t accounting for that, now you see the problem.

Unexpected rehab overruns: Always add a 10–15% contingency buffer on top of your repair estimate. Always.

How This Connects to BRRRR

If you’re using the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat), the same math applies — just with a different exit.

The whole point of BRRRR is to pull your invested cash back out through the refinance. If you go into the deal with your all-in cost too high relative to ARV, the refinance won’t cover what you put in. You end up with cash stuck in the deal, and you can’t “repeat” the strategy because you don’t have the capital to do it again.

That’s not a BRRRR. That’s just a rental property you overpaid for.

The 60% all-in rule applies here too. If the appraisal after rehab comes in at $250K and you can refinance at 75% LTV, you’re pulling out $187,500. If your all-in cost was $160,000, you’re good — you got your money back plus some. If it was $200,000, you’ve got $12,500 stuck in the deal permanently.

Use the BRRRR Calculator to run these numbers before you ever make an offer.

New Construction: Where the Math Actually Gets Interesting

One thing I didn’t expect to find while researching house flipping hidden costs is how the numbers on new construction can actually be cleaner.

With a fix-and-flip, you’re dealing with unknown rehab conditions — old plumbing, surprise foundation issues, asbestos, you name it. Every one of those is a hidden cost waiting to happen.

With new construction, your cost structure is more predictable:

- Construction cost typically runs around 50% of final sale price

- You’re not dealing with deferred maintenance or surprise gut jobs

- Lenders (including hard money lenders) will sometimes work with first-time builders if the numbers are solid

In markets like Dallas or Austin, investors are reportedly pulling $200,000–$400,000+ profit on new builds. Philadelphia isn’t Texas, but the principle holds — when you control the build cost and the product is brand new, your hidden cost exposure is lower.

A Quick Example to Pull It All Together

Let’s say you’re looking at a house with an ARV of $200,000.

| Cost Item | Amount |

|---|---|

| Purchase price | $85,000 |

| Rehab estimate | $35,000 |

| Contingency (15%) | $5,250 |

| Hard money points + fees | $3,500 |

| Interest (6 months @ 12%) | $7,200 |

| Insurance + taxes (holding) | $2,400 |

| Buy-side closing costs | $3,500 |

| Sell-side closing costs + agent | $14,000 |

| Total All-In | $155,850 |

| ARV | $200,000 |

| All-In % of ARV | 77.9% |

That deal looks okay on paper at $85K purchase price — but when you run the full house flipping hidden costs, you’re at nearly 78% of ARV. That’s not a deal. That’s a headache.

To hit 65% all-in on a $200K ARV property, your total costs need to stay under $130,000. Back-calculate from there to figure out your max purchase price.

Run the Numbers Before You Fall in Love With a Deal

Emotions are expensive in real estate. You find a house, you can already picture the after photos, and suddenly you’re rounding down on repair estimates and forgetting about title fees.

Don’t do that.

Use the calculators below to run the actual numbers — house flipping hidden costs included — before you make any offer.

Not financial advice — just someone doing a lot of research and asking a lot of questions.