The first time I heard about the silent second mortgage strategy, I had to rewind the video three times. Not because it was complicated — because it was so simple I couldn’t believe more people weren’t talking about it.

This comes from Alisha Collins, a real estate agent who’s been using this exact method for 20 years to build her rental portfolio. And once you understand how it works, the way you think about equity is never the same.

What Is a Silent Second Mortgage Strategy?

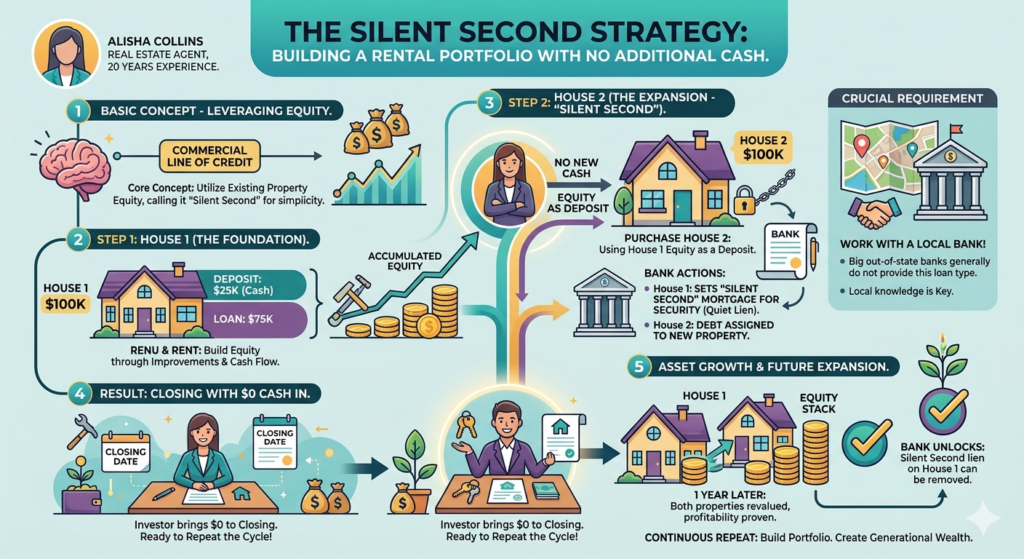

At its core, the silent second mortgage strategy is about using the equity you’ve already built in one property to fund the down payment on the next one — without bringing new cash to the closing table.

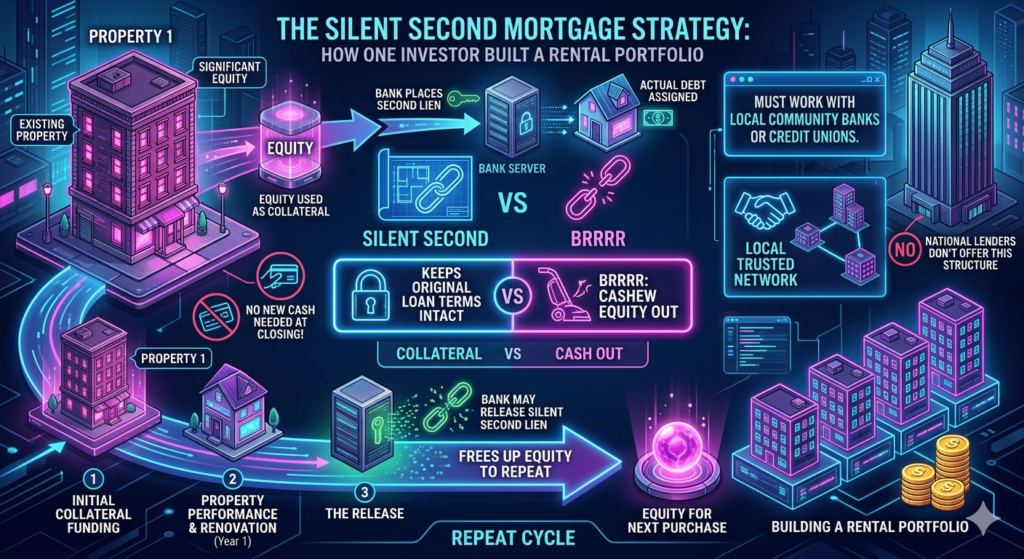

Technically, it works like a commercial line of credit. But calling it that makes people’s eyes glaze over. “Silent second” is a better way to describe what’s actually happening: the bank places a second lien (silently, in the background) on your existing property as collateral, while the actual debt gets assigned to the new property you’re buying.

You’re not pulling cash out. You’re using equity as leverage — and the bank holds your first property as backup security.

How the Silent Second Mortgage Strategy Works Step by Step

Let’s walk through a real example.

House 1:

- You buy a $100,000 property

- Put $25,000 down, borrow $75,000

- Rehab it, rent it out, let equity build

House 2 (here’s where it gets interesting):

- You find another $100,000 property

- Instead of pulling new cash for the down payment, you use the equity from House 1

- The bank places a silent second lien on House 1 as collateral

- The actual loan debt is assigned to House 2

- You show up to closing with zero new cash out of pocket

That’s it. That’s the whole thing.

Why the Bank Goes Along With This

This is the part that surprises most people. Why would a bank agree to this structure?

Because they’re fully secured. They have a lien on House 1 and the loan on House 2. From their perspective, there’s collateral backing everything. As long as your numbers are solid and your rental income covers the debt service, they’re comfortable.

The key word there is local bank. This is not something you’re going to walk into Chase or Wells Fargo and ask for. National lenders and government-backed loan programs don’t do this. They have rigid underwriting boxes and this deal structure doesn’t fit.

Local community banks and regional lenders are a completely different conversation. They have more flexibility, they make portfolio loans, and they can structure deals based on the actual asset rather than just your W-2.

If you’re not already building a relationship with a local bank or credit union, that’s the first step before this strategy even becomes available to you.

The Equity Snowball Effect

Here’s where the silent second mortgage strategy really starts to compound.

After about a year — assuming both properties are performing well, rents are coming in, and values have held or appreciated — the bank can reassess. If they’re satisfied with how the portfolio is performing, they may release the silent second lien on House 1.

When that happens, you now have:

- House 1: fully free equity available again

- House 2: its own equity building through rent and appreciation

And the cycle repeats. Use House 1 or House 2’s equity to fund House 3. Let the bank place a silent second on whichever property makes sense. Close without new cash.

This is how a single $25,000 down payment can theoretically fund an entire rental portfolio over time — as long as each property is performing and the bank stays confident in you.

What You Need to Make This Work

This isn’t a strategy you can execute on day one. There are a few things that need to be in place:

Before anything else, run your current equity position through the Cash-Out Refi Calculator to see what you’re actually working with.

Equity in an existing property. You need at least one property that has meaningful equity — either from your original down payment, appreciation, or forced appreciation through rehab.

A relationship with a local bank. This is non-negotiable. Start having conversations with community banks and credit unions now, even before you need the loan. Ask about their portfolio lending programs. Ask if they do commercial lines of credit secured by residential investment property.

Properties that cash flow. The bank needs to see that your rentals are actually generating income. If your properties are breaking even or losing money, this conversation gets a lot harder.

Clean financials. You don’t need to be rich, but you need to be organized. Bank statements, rent rolls, lease agreements — have all of it ready.

According to the Census Bureau, rental vacancy rates have remained relatively low in most markets, which supports the case for rental portfolio investing when the numbers are structured correctly.

How This Compares to BRRRR

A lot of people are going to read this and think — isn’t this just BRRRR?

Similar idea, different mechanics.

BRRRR relies on a cash-out refinance to pull your invested capital back out after the rehab and rent-up phase. You’re refinancing the property itself based on its new appraised value.

The silent second mortgage strategy keeps the original loan structure intact and uses the equity as collateral rather than cashing it out. You’re not refinancing House 1 — you’re pledging it to help fund House 2.

If you want to stress-test a BRRRR deal before committing, the BRRRR Calculator can help you see whether your numbers actually work before you talk to any lender.

Both strategies use leverage. Both require performing properties. But the silent second approach keeps your existing loan terms untouched, which can matter a lot if you locked in a good rate.

Run the Numbers First

Before you have any conversation with a bank about this strategy, know your numbers cold.

What does your current equity position look like? What would a new property’s cash flow look like with this financing structure? Use the calculators below to work through it before you walk into any lender meeting.

Not financial advice — just someone doing a lot of research and asking a lot of questions.