If you’ve spent more than ten minutes on real estate TikTok, you’ve seen it. Someone standing in front of a house, pointing at text that says “I bought this with ZERO dollars down.” Comments going crazy. Link in bio. $997 course waiting for you on the other side.

No money down real estate investing is real — but it’s not what most of those videos are selling you. I’ve been doing a deep dive into how this actually works, and there’s a lot more nuance here than a 60-second clip can cover. So let me break it down the way I wish someone had broken it down for me.

No Money Down Real Estate Investing: Is It Actually Possible?

Short answer: yes. But the longer answer is — it depends entirely on your situation and the deal itself.

The concept of no money down real estate investing has been around for decades. It’s not some new hack a 22-year-old discovered on social media. What’s changed is how it’s being marketed — and that’s where things get muddy.

Let me explain what’s actually going on behind the scenes.

What “Asset-Based Lenders” Actually Are

Most of the TikTok content around 100% funding points to something called an asset-based lender — and frames it like it’s some secret Wall Street institution that regular investors don’t know about.

Here’s the reality: asset-based lenders do exist, and they’re different from your typical hard money lender in a few ways. Regular hard money lenders look at the property value (ARV) and usually lend up to 70–80% of that. You’re still on the hook for the remaining 20–30% out of pocket.

Asset-based lenders — which can include private equity funds, institutional lenders, or larger private capital groups — focus almost entirely on the asset itself rather than your income or credit score. And in certain structures, they can fund 100% of a deal. But here’s what the TikToks leave out: how they do it.

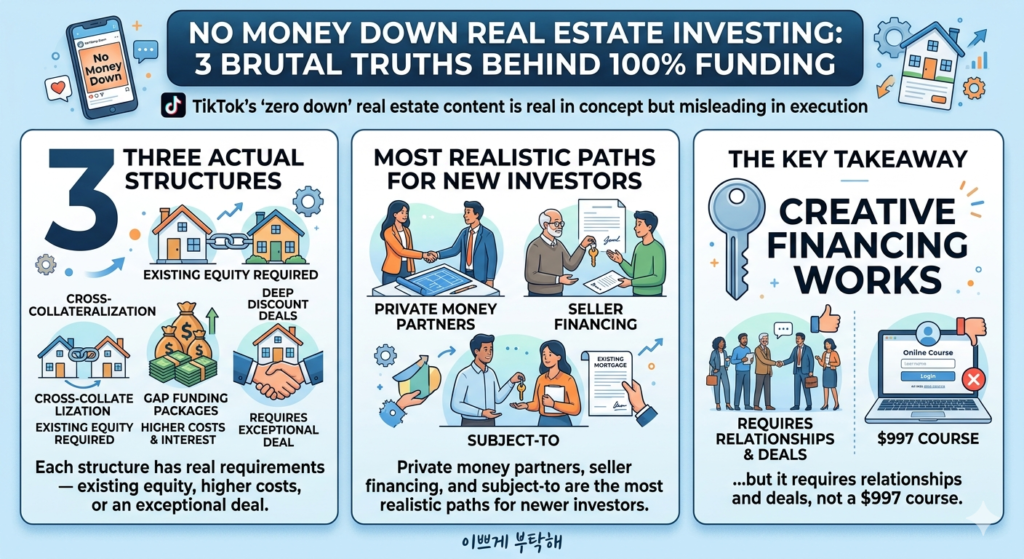

The 3 Structures Behind 100% Funding

1. Cross-Collateralization

This is the most common one. Say you already own a rental property with equity sitting in it. A lender can tie that existing equity to your new deal as additional collateral. Now they’re looking at the combined value of both properties — and suddenly lending 100% on the new purchase feels a lot less risky to them.

The catch? You need to already own property with equity. This is not a beginner move.

2. GAP Funding Packages (1st + 2nd Lien Combined)

Some lenders offer a packaged deal where they handle both the primary loan (say, 80% of purchase price) and the gap — the remaining 20% — through a second, subordinate loan. Both come from the same source, so on paper it looks like 100% funding.

The subordinate loan comes with a higher interest rate, sometimes equity sharing requirements, and stricter terms. You’re not getting free money — you’re paying more for the convenience of not bringing cash to the table. According to the Consumer Financial Protection Bureau, layered financing structures like this carry real risk for borrowers who don’t fully understand the terms.

3. Deep Discount / Wholesale Purchase

This one is actually the most legitimate path to no money down real estate investing — and the least sexy to talk about on TikTok.

If a property has an ARV of $200,000 and you negotiate it under contract for $100,000 (off-market, distressed seller, sheriff sale, whatever), the lender sees a $200K asset securing a $100K loan. Their LTV is 50%. They’ll fund the whole thing all day because their risk is essentially zero.

This isn’t a special lender. This is just a great deal. Any hard money lender will do this. The “secret” is finding deals that are deep enough — which is the actual hard part nobody wants to talk about.

No Money Down Real Estate Investing: The Real Catch

None of these structures are bad. But all of them have conditions that 60-second videos don’t mention:

Cross-collateralization requires existing equity — meaning you’re not starting from zero, you’re leveraging what you already built.

GAP funding packages cost more. Higher origination points, higher interest rates, sometimes equity splits. Your profit margin on the deal shrinks significantly.

Deep discount deals require hustle, patience, and a network. You’re not finding $100K ARV deals scrolling Zillow. These come from relationships — wholesalers, attorneys, driving for dollars, sheriff sales.

And across all three — lenders offering true 100% funding typically want to see a track record. They’re not handing $400K to someone who just watched a YouTube video last Tuesday.

So What Does No Money Down Actually Look Like for a Real Investor?

In practice, the investors pulling off no money down real estate investing are usually doing one of these:

Private money partners. Find someone with capital who wants returns without doing the work. You find the deal, they fund it. Profits split. This is probably the most realistic path for newer investors — but it requires you to bring something to the table, which is the deal itself.

Seller financing. The seller becomes the bank. You negotiate terms directly with them — down payment, interest rate, repayment schedule. Works best with motivated sellers who own the property free and clear or close to it.

Subject-to. You take over the existing mortgage payments without formally assuming the loan. The deed transfers to you, the loan stays in the seller’s name. Requires almost no cash upfront — but carries real legal and ethical complexity. Always work with a real estate attorney on these.

Hard money + private money stack. Hard money covers 70–75% of ARV, private money partner covers the gap. Effectively zero out of pocket — but you need both relationships in place before you can execute.

The TikTok Problem

Here’s what frustrates me about how no money down real estate investing gets talked about online: the strategy is real, but the framing is designed to sell you something.

“Stop saving for a down payment” sounds great until you realize the alternative requires either existing equity, an incredible deal, or a private money relationship you haven’t built yet. None of those things come from a $997 course. They come from doing the work.

I’m not trying to be cynical. I genuinely believe creative financing is one of the most powerful tools in real estate. But I’ve seen too many people go in thinking they found a loophole, only to realize the “loophole” had requirements nobody mentioned upfront.

What I’m Actually Doing

I’m still learning this side of financing — I’ll be the first to admit that. I’ve done a few flips in partnership and I’m deep in research mode on creative deal structures right now. What I’ve found is that the investors doing this well aren’t using secret lenders. They’re building relationships, finding real deals, and stacking financing tools together creatively.

That’s a slower path than TikTok makes it sound. But it’s the one that actually works.

Not financial advice — just someone doing a lot of research and asking a lot of questions.