DSCR loan rental property strategy is the question I keep coming back to — because right now, it’s the most realistic path I can see back into real estate investing.

I’m going to be honest about where I am. The last few years have not been kind financially. Bad things came in waves, and by the time the dust settled, I had lost a significant amount of money. Twice.

What pulled me back — slowly, imperfectly — was coming back to the thing I’ve always believed in. Real estate. Not because it’s easy. Not because I have money right now. But because it’s the one area where I’ve seen real value created.

So here I am. Researching. Studying. Trying to figure out how to get back into this market with as little cash as possible.

What Is a DSCR Loan Rental Property Strategy, Exactly?

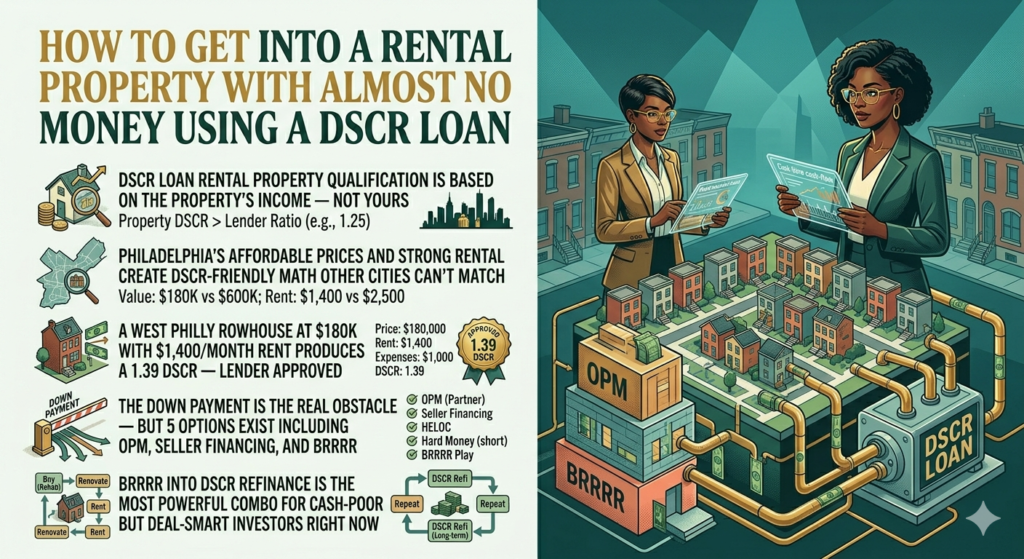

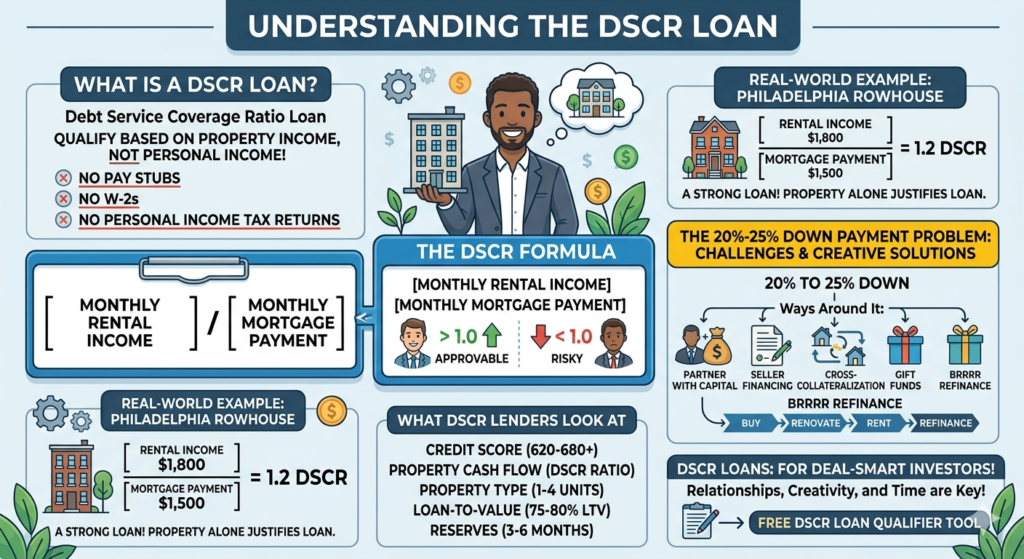

DSCR stands for Debt Service Coverage Ratio. It’s a loan used primarily by real estate investors — and the fundamental difference from a conventional mortgage is this: the lender doesn’t care about your personal income.

Read that again.

No pay stubs. No W-2s. No two years of tax returns. Doesn’t matter if you’re self-employed, between jobs, or building something from scratch.

What they care about: does the property generate enough rental income to cover the mortgage?

That’s the DSCR loan rental property qualification in a nutshell. Most lenders want a DSCR of 1.0 or higher — meaning rental income at least covers the mortgage. Some go as low as 0.75 in strong rental markets.

The formula: DSCR = Monthly Rental Income ÷ Monthly Mortgage Payment

If a property rents for $1,800/month and the mortgage is $1,500/month: $1,800 ÷ $1,500 = 1.2 DSCR ✅

According to the Mortgage Bankers Association, DSCR loans have become one of the fastest-growing loan products for residential investors over the last three years — because they fill a gap that conventional financing simply can’t.

Why Philadelphia Is DSCR Loan Rental Property Friendly

Philadelphia has strong rental demand and relatively affordable purchase prices compared to other major East Coast cities. That combination creates DSCR-friendly math in a way that New York or Boston simply don’t.

Real example:

- Property: 3-bedroom rowhouse in West Philadelphia

- Purchase price: $180,000

- Down payment (20%): $36,000

- Loan amount: $144,000

- Rate: 7.5% on a 30-year DSCR loan

- Monthly payment: ~$1,007

- Market rent: $1,400–$1,600/month

- DSCR: $1,400 ÷ $1,007 = 1.39 ✅

A lender looking at this deal isn’t thinking about your tax returns. They’re thinking about that 1.39.

Want to run your own numbers? The DSCR Calculator will show you exactly where a property stands before you talk to a lender.

The Down Payment Problem With DSCR Loan Rental Property

Here’s where I’ll be completely straight: DSCR loans typically require 20–25% down. That’s the catch.

But the down payment obstacle has solutions:

Option 1 — Partner with someone who has capital. You find the deal, manage the project, bring the expertise. They bring the down payment. Split equity or cash flow. This is OPM — Other People’s Money — and it’s how a significant percentage of investors actually get started.

Option 2 — Seller financing on the down payment. Some sellers will carry a portion of the purchase price themselves. Creative negotiation can result in the seller effectively covering the down payment.

Option 3 — Cross-collateralization. If you own another property with equity, some lenders will allow you to use that equity as collateral in lieu of cash.

Option 4 — Gift funds. Some DSCR programs allow gift funds from family members to cover the down payment.

Option 5 — BRRRR into a DSCR loan rental property refinance. Buy distressed with hard money. Renovate. Rent. Refinance into a DSCR loan based on new appraised value. If you bought and renovated correctly, the refinance covers your costs and leaves you holding a cash-flowing rental with little to none of your original capital still in the deal.

This is arguably the most powerful combination in real estate right now for people who are cash-poor but deal-smart.

What DSCR Loan Rental Property Lenders Actually Look At

- Credit score: Most want 620–680 minimum

- Property cash flow: The DSCR ratio is the core metric

- Property type: Single-family, duplex, triplex, quadplex — most cap at 4 units

- LTV: Typically 75–80%, meaning 20–25% down

- Reserves: Many want 3–6 months of mortgage payments in reserves after closing

My Honest Take

DSCR loan rental property financing is real, it works, and it was genuinely designed for investors who don’t fit the conventional mortgage box. Self-employed, between jobs, building income outside traditional employment — this is the product made for you.

The down payment is the real obstacle. But as I’ve laid out above, it has solutions — none of them easy, all of them requiring relationships, creativity, or time.

I’m working on all three.

Not financial advice — just someone doing a lot of research and asking a lot of questions.