BRRRR Real Estate Investing: How One Woman Turned $4,000 Into an $11 Million Portfolio

I’ll be honest — when I first saw this, I thought it was one of those “too good to be true” real estate stories.

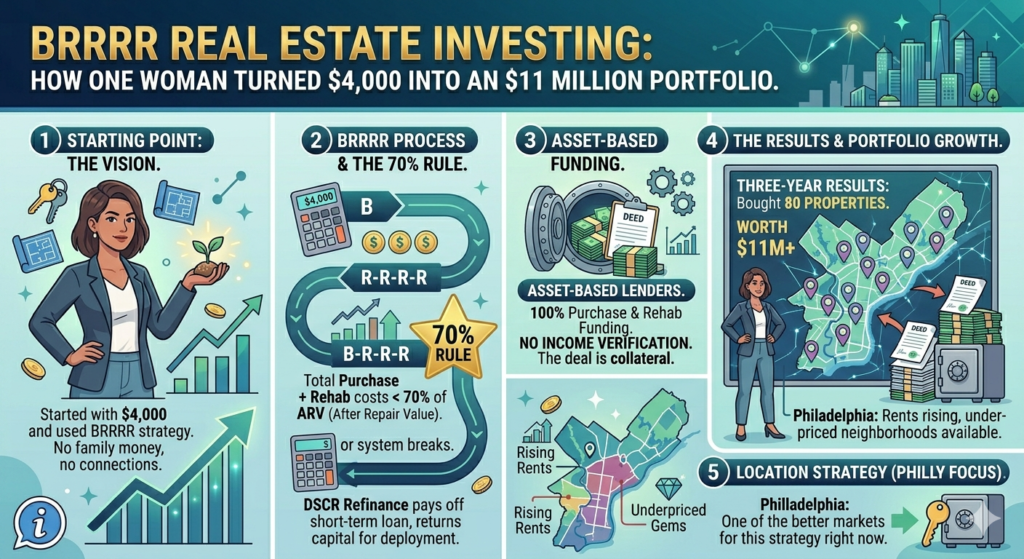

$4,000. No wealthy family. No connections. 80 properties in three years.

But the strategy she laid out is real. And once you understand how BRRRR real estate investing actually works at scale, the math makes complete sense.

The Starting Point

She didn’t come from money. She started with $4,000 and a very specific strategy — one that allowed her to buy properties with none of her own money, recycle her capital, and repeat the process over and over again.

The strategy is called BRRRR real estate investing: Buy, Rehab, Rent, Refinance, Repeat. And she executed it at a scale most people don’t think is possible.

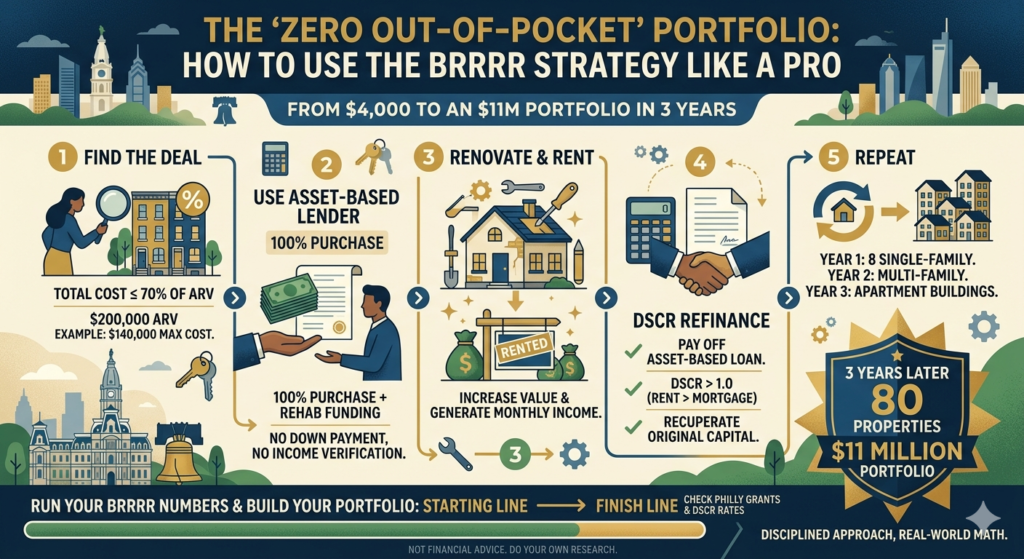

Step 1: Find the Right Deal

The first rule her lender gave her: the total cost of buying and renovating the property had to be 70% or less of the ARV — the After Repair Value.

So if a property would be worth $200,000 after renovation, her total all-in cost (purchase + rehab) had to be $140,000 or less.

This is the most important part of BRRRR real estate investing. The deal has to work on paper before anything else. If you can’t find properties that meet this threshold, the rest of the strategy falls apart.

In Philadelphia and the surrounding suburbs, these deals exist — especially in neighborhoods that are still underpriced relative to where they’re heading. According to BiggerPockets, the 70% rule is the foundation most BRRRR investors use to screen deals before spending a single dollar.

Use the BRRRR Calculator to run your numbers before you commit to anything.

Step 2: Use an Asset-Based Lender

Here’s where most people get stuck: “I don’t have money to buy the property.”

She solved this with an asset-based lender — similar to a hard money lender — who funded 100% of the purchase price AND the renovation costs.

No down payment. No income verification. The lender looked at the deal, saw that the numbers worked (purchase + rehab under 70% of ARV), and funded the whole thing.

This is how she bought her first property with almost none of her own money. And her second. And her third. BRRRR real estate investing only works at scale when you have the right lending relationships in place.

Step 3: Renovate and Rent

Once the property was purchased, she renovated it — bringing it up to rental-ready condition and pushing the value up toward that ARV number.

Then she got a tenant in. Now the property was generating monthly income and the clock on the refinance could start.

Step 4: The BRRRR Real Estate Investing Refinance

With a tenant in place and the property worth significantly more than she paid, she went to a DSCR lender and refinanced.

DSCR loans are based on the property’s rental income, not your personal income. The lender looked at the rent coming in, confirmed it covered the new mortgage payment, and issued a long-term loan.

That new loan paid off the short-term asset-based loan she used to buy the place.

And here’s the key: because she bought and renovated at 70% of ARV, the refinance often returned most — or all — of her original capital. She had a rental property. She had a tenant. And she had her money back to do it again.

Run your refinance numbers through the Cash-Out Refi Calculator to see how much capital you could pull back out.

Step 5: Repeat — At Scale

Year one: 8 single-family homes.

Then she moved into small multi-family properties. Then apartment buildings.

$4,000 in. $11 million portfolio out. Three years later.

That’s BRRRR real estate investing executed at its highest level — not luck, but a systematic, disciplined approach applied over and over again.

Is This Realistic for Regular People?

Yes — with caveats.

The deals have to pencil out. You need to find properties at the right price, with enough spread between purchase price and ARV to make the math work. That takes time, research, and a good eye for value.

The asset-based lenders exist — but they want to see a solid deal. You can’t bring them a mediocre property and expect 100% financing.

And the DSCR refinance requires the rent to cover the mortgage. In Philadelphia’s rental market right now, that’s increasingly achievable — rents have been climbing while purchase prices in certain neighborhoods are still reasonable.

BRRRR real estate investing isn’t a get-rich-quick scheme. It’s a very disciplined, very systematic approach to building a portfolio — one deal at a time. But the math works. And Philadelphia is one of the better markets in the country to try it right now.

Not financial advice — just someone doing a lot of research and asking a lot of questions.