How to Save $12,000 in Construction Loan Interest: The Non-Dutch Draw Strategy Explained

A construction loan draw schedule isn’t just paperwork — the way you time your draws determines how much interest you actually pay. And most people building new construction have no idea how much they’re leaving on the table.

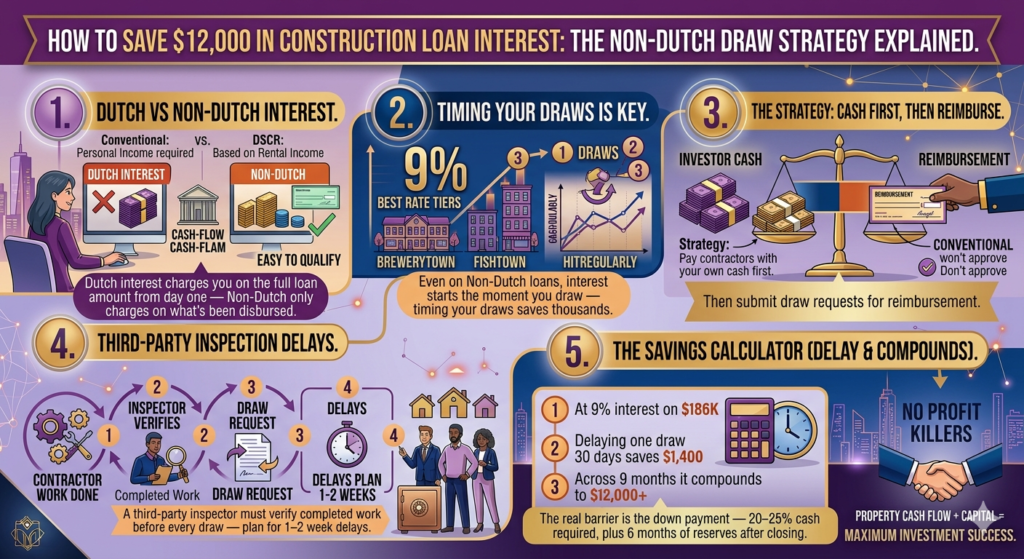

I was watching a video recently from someone who builds new construction properties, and one number stopped me cold. He said he spent $186,000 in his very first month of construction. And almost immediately, $1,400 of that was just gone. Interest. On money he’d already drawn but hadn’t fully spent yet.

Over nine months, that adds up to over $12,000 in unnecessary interest. The strategy he used to avoid it comes down to one thing: understanding your construction loan draw schedule.

First: How Construction Loans Actually Work

Unlike a regular mortgage where you get all the money at once, construction loans disburse in stages. You don’t get $500,000 on day one — you get it in chunks as the project progresses, paying interest only during the 12–18 month build period before the loan converts to a regular mortgage.

Each time you need money, you submit a draw request. The lender sends out a third-party inspector to verify the work is actually done before releasing funds. That inspection process takes 1–2 weeks — and the moment the money hits your account, the interest clock starts.

Dutch vs Non-Dutch: What’s Actually Different

Dutch interest (the bad one):

You pay interest on the full loan amount from day one — regardless of how much has actually been disbursed. Have a $1,000,000 construction loan but only drawn $250,000? You’re paying interest on all $1,000,000.

On a $1 million loan at 12% for 12 months, Dutch interest costs $120,000 — whether you draw it all upfront or in stages.

Non-Dutch interest (what most lenders use now):

You only pay interest on what’s actually been disbursed. Same $1 million loan, same 12% rate — if $250,000 is disbursed each quarter, total interest drops to $75,000. Nearly $45,000 saved just from the loan structure.

Most construction loans today are Non-Dutch. But here’s what that video taught me — even with a Non-Dutch construction loan draw schedule, the timing of your draws still matters enormously.

The Construction Loan Draw Schedule Strategy That Saves $12,000

Even on a Non-Dutch loan, interest starts the moment you draw. So if you draw $186,000 and take two weeks to spend it — you’re paying interest on money sitting in your account doing nothing.

The strategy:

Step 1: Use your own cash to pay contractors and suppliers first. Step 2: Let the work pile up — don’t submit a draw request every time you write a check. Step 3: When you’ve spent enough of your own cash, submit a draw request to get reimbursed. Step 4: Lender sends an inspector, verifies completed work, approves the draw. Step 5: Money comes back to you — and only now does interest start on that amount.

Push the draw request as late as possible and you minimize the days you’re paying interest on borrowed funds. Do this consistently across a 9-month build and you can save $12,000 or more.

The catch: you need enough cash on hand to float costs while you wait for reimbursement. If you’re living draw-to-draw, you don’t have the flexibility to delay.

Why the Bank Sends an Inspector

You cannot call the lender and say “framing is done, send $50,000.” They will not wire money based on your word alone.

A third-party inspector reviews completed work, submits a report, and the lender typically collects a lien release before approving funds. The inspector evaluates percentage of completion, whether it matches your draw request, quality standards, and photo documentation.

This is actually good for investors — it keeps your GC accountable. If a contractor overstates progress, the inspector catches it before more money flows to them. But it also means planning around a 1–2 week delay between submitting a draw request and receiving funds.

Use the House Build Cost Calculator to map out your full draw timeline before construction starts — so you know exactly how much working capital you need to float between draws.

What Construction Loan Rates Look Like in 2026

Construction loan rates currently range from 7.5% to 9% — about 1–2 percentage points higher than conventional mortgage rates.

At 9% on $186,000, that’s roughly $1,400 per month. Delay drawing that money by 30 days and you save $1,400. Across a full 9-month construction loan draw schedule with multiple draws at various stages, those savings compound fast.

What to Ask Your Lender Before You Sign

Not all lenders handle construction loan draw schedules the same way. Ask these before you commit:

- Dutch or Non-Dutch? If it’s Dutch, negotiate hard or walk away.

- How long does the draw inspection take? 1 week vs 3 weeks is meaningful for cash flow.

- How many draws am I allowed? More draws = more timing flexibility.

- Is there a fee per draw request? Some lenders charge $150–$300 per inspection.

- Milestone-based or my own schedule? Milestone-based draws give you less control over timing.

According to LendSure Home Loans, construction loan interest structures vary significantly between lenders — which is why asking these questions upfront can save you tens of thousands across a single project.

The Bigger Picture

A well-timed construction loan draw schedule isn’t complicated. It’s cash flow management — spend your own money first, get reimbursed later, minimize the days you’re paying interest on borrowed funds.

But it requires two things most beginner investors don’t think about before they start: enough working capital to float costs between draws, and a clear understanding of how your lender’s inspection and disbursement process works.

Know those two things going in, and you’ll build cheaper than most people taking on the exact same loan.

Not financial advice — just someone doing a lot of research and asking a lot of questions.