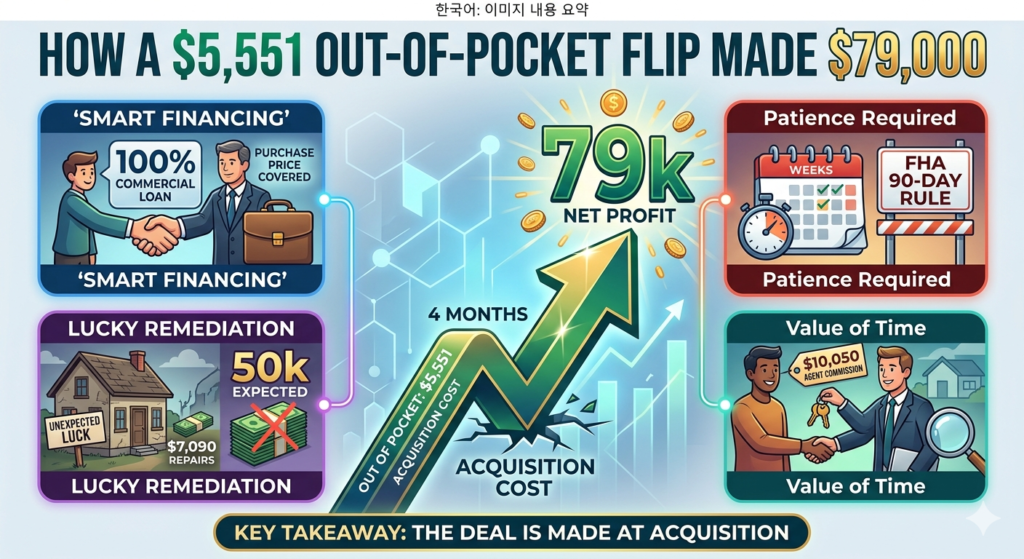

House flip profit of $79,000 on $5,551 out of pocket. In four months. I want to be upfront before I break down these numbers.

This deal worked out almost perfectly. The numbers are real. The profit is real. And a significant part of why it worked has nothing to do with skill — it has to do with luck.

Understanding what had to go right for this deal to produce this house flip profit is just as important as understanding the strategy itself.

The Deal Behind This House Flip Profit

A homeowner had an HVAC system failure that caused water damage throughout the house. They didn’t want to deal with the repairs. They wanted out — fast, as-is.

The property: 4 bedrooms, 3 bathrooms, a separate mother-in-law suite, a large workshop, and an acre of land. Two years earlier it had been worth $345,000.

Purchase price: $220,000.

That’s a $125,000 discount from recent value — before a single repair.

The Financing: 0% Down on a House Flip Profit Play

When you buy a home to flip, you’re buying it as an investment — which means commercial loans, hard money, or private money. The building is still a regular house. But the loan is classified differently because your purpose is investment, not residence.

In this case, the flipper used a commercial loan that covered 100% of the purchase price. No down payment on the acquisition itself.

The terms weren’t cheap — 8% interest rate, 1.5 points. But the only cash out of pocket at closing was $5,551 in closing costs.

$5,551 to control a $220,000 asset. That’s how you set up a meaningful house flip profit without tying up your own capital.

The Lucky Part: Repairs That Didn’t Need to Happen

The original plan assumed $50,000 in repairs. Water damage, potential mold, HVAC replacement — all reasonable assumptions.

The lucky part: a remediation company had already been through the property and set up industrial dehumidifiers. By the time the flipper took possession, the house had been thoroughly dried out. Mold testing came back clean.

The $50,000 repair budget became $7,090:

- New flooring

- Water heater replacement

- Wall repairs and paint

- Minor fixes throughout

That’s it. The $42,000 difference between expected and actual repairs? That’s luck. Good, legitimate, unforeseeable luck. Not every house flip profit story gives you that.

The FHA 90-Day Rule: Why the House Flip Profit Took 4 Months

The flipper listed at $330,000 and accepted an offer at $335,000 (with a $3,000 seller credit back to the buyer).

But here’s where something most beginners don’t know comes into play.

The buyer wanted to use FHA financing. And FHA has an anti-flipping rule.

The FHA 90-day anti-flipping rule: FHA won’t approve a loan on a property that the seller has owned for less than 90 days. They’re not questioning the seller’s behavior — they’re protecting their own money. A house that sold for $220,000 sixty days ago and is now listed at $335,000 triggers FHA’s scrutiny regardless of what work was done.

For flippers, this means either waiting until 90 days have passed, or finding a cash or conventional buyer who isn’t subject to the same restriction.

In this case, the flipper waited. Four months total hold time. Four months of paying 8% interest on a $220,000 loan — $5,946 in carrying costs coming directly out of the house flip profit.

The Full House Flip Profit Numbers

| Item | Amount |

|---|---|

| Purchase price | $220,000 |

| Sale price | $335,000 |

| Seller credit to buyer | -$3,000 |

| Repairs | -$7,090 |

| Agent commission | -$10,050 |

| Interest (4 months at 8%) | -$5,946 |

| Taxes, insurance, utilities | -$3,700 |

| Closing costs (purchase) | -$5,551 |

| Net house flip profit | $79,663 |

Cash invested: $5,551. House flip profit: $79,663. In four months.

The Agent Fee That Was Worth It

The flipper paid $10,050 in agent commissions to sell the property — even though they had a real estate license themselves.

Why pay for something you can do yourself?

Because during those four months, finding and closing new deals was worth more than the time it would take to handle one sale personally. The $10,050 bought back the hours needed to source the next opportunity.

This is the mindset shift that separates people who do one flip at a time from people who build a real portfolio. Your time has value. Paying someone else to handle tasks you could do — but shouldn’t — is often the right business decision.

What This House Flip Profit Actually Teaches

Buying right. A $125,000 discount from recent value created enormous margin before the first nail was hammered.

Creative financing. A commercial loan with no down payment meant minimal cash at risk — $5,551 to generate a $79,663 house flip profit.

Transparency. The flipper disclosed the water damage history and provided mold test results to the buyer. Not just ethical — it’s protection against future liability.

Resilience. Not every deal goes this smoothly. The willingness to absorb setbacks and keep going is what makes a real estate business sustainable.

And yes — luck. The repair budget that evaporated because of someone else’s remediation work. You can’t plan for it. You can only recognize it when it happens and not confuse fortune with skill.

According to BiggerPockets, the average house flip profit in the U.S. runs 26–28% of the purchase price — but deals with distressed sellers, creative financing, and below-market acquisition consistently outperform that average when the numbers are set up correctly before the purchase.

Use the Philly Flip Profit Calculator to model your own house flip profit before you make any offer — plug in purchase price, repairs, carrying costs, and sale price to see your realistic net.

Not financial advice — just someone doing a lot of research and asking a lot of questions.