Rental property cash flow isn’t everything — and that mindset held me back for a long time from seeing what was really happening under the surface.

I used to think if a rental property didn’t spit out $500 a month, what was even the point? Then I came across a concept that rewired how I think about real estate investing: ghost income. The idea that most of the money you make in real estate is money you never actually see hit your bank account — at least not right away.

The Problem With Rental Property Cash Flow Obsession

Don’t get me wrong — rental property cash flow matters. You need it to pay your mortgage, cover repairs, and keep the lights on. But if you’re only evaluating deals based on monthly cash flow, you’re literally ignoring three other income streams that are quietly building your net worth every single month.

In Philadelphia specifically, this is really relevant. Rental property cash flow here isn’t always massive — especially if you’re buying in neighborhoods like Germantown, West Philly, or Kensington where prices have gone up but rents haven’t caught up proportionally. But that doesn’t mean those deals are bad. It means you have to know how to read the full picture.

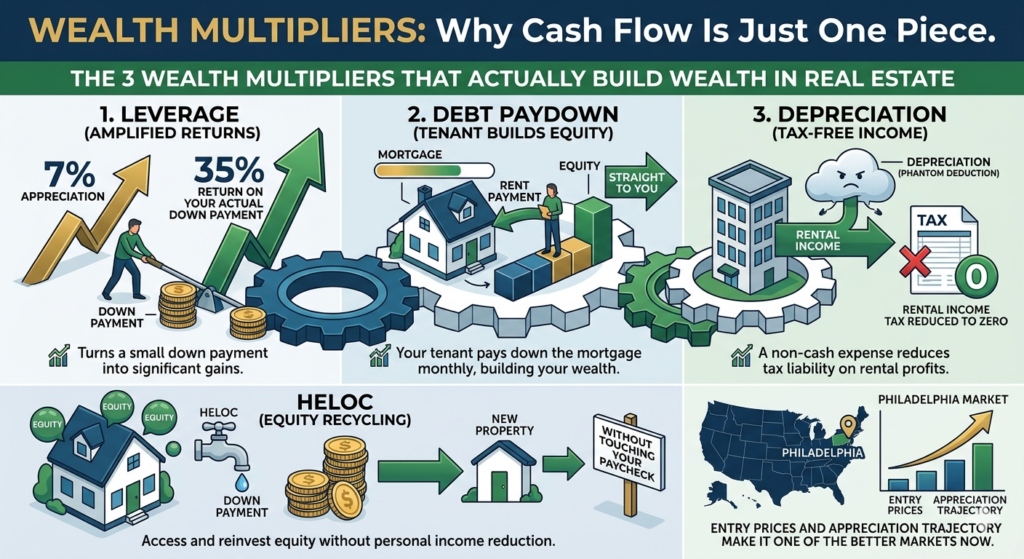

Wealth Multiplier #1: Appreciation + Leverage

This is the one that messes with your brain in the best way once you actually understand it.

Let’s say you buy a $200,000 property in Philadelphia with 20% down — that’s $40,000 out of pocket. You now control a $200,000 asset with $40,000. That’s 5x leverage.

Philadelphia home values have been appreciating steadily. At a conservative 5% annual appreciation, that’s $10,000 in value added in year one. But here’s the thing — that $10,000 gain is on the full property value, not just your $40,000 down payment.

Your actual return on invested capital is 25% — not 5%.

Run it at 7% appreciation (closer to the actual Philly average in some neighborhoods over the last decade): you’re looking at a 35% return on your down payment from appreciation alone. Before you collect a single dollar in rental property cash flow.

This is why Philadelphia keeps coming up. The market is still affordable enough that you can get in with reasonable down payments, but the appreciation trajectory — especially in transitioning neighborhoods — is genuinely compelling.

Wealth Multiplier #2: Principal Paydown (Your Tenant Is Building Your Equity)

Every month your tenant pays rent, a portion of that mortgage payment goes toward paying down the loan principal. That equity goes directly to you.

You didn’t earn it by working. You didn’t save it. Your tenant built it for you.

On a $160,000 mortgage at 7% interest over 30 years, you’re paying down roughly $2,500–$3,500 in principal in just the first year. That number grows every year as the loan amortizes.

So even on a deal where you’re only netting $200/month in rental property cash flow — which some people would call a “bad deal” — you’re actually gaining $200–$300/month in equity on top of that. It’s like a forced savings account that your tenant is funding.

And when the mortgage is fully paid off? The property that was giving you $200/month suddenly gives you $1,200/month. That’s the long game.

Wealth Multiplier #3: The Phantom Deduction (Depreciation)

The IRS lets you depreciate a residential rental property over 27.5 years. If you buy a $200,000 property and the land is worth $40,000, your depreciable basis is $160,000. Divide that by 27.5 and you get roughly $5,800 per year that you can deduct from your rental income — even if the property is actually going up in value.

If you’re collecting $18,000/year in rent and your actual expenses are $14,000 — you’d normally owe taxes on $4,000 in profit. But after the depreciation deduction? You’re showing a loss on paper. Zero rental income tax.

The money still came in. You just don’t pay taxes on it.

That’s ghost income. Real rental property cash flow, invisible to the IRS — legally.

The Strategy That Ties It All Together: Recycling Capital

Here’s how people actually scale a portfolio without going back to their savings account every time.

You buy Property #1. It appreciates. You build equity — from appreciation and principal paydown. A few years in, you have $50,000–$80,000 in equity sitting in that property doing nothing.

You pull it out with a HELOC (Home Equity Line of Credit). Use that money as the down payment on Property #2. Now you have two properties building equity, generating rental property cash flow, and giving you depreciation deductions.

Repeat.

This is how people go from one rental property to six without ever touching their W-2 paycheck again.

What This Looks Like in Philadelphia Right Now

Philadelphia is genuinely one of the better markets for this strategy right now:

Entry prices are still relatively low compared to NYC, DC, or even parts of New Jersey. You can still find solid rental properties in the $150K–$250K range in neighborhoods with real appreciation upside.

Rent growth has been solid — especially in neighborhoods like Fishtown, Point Breeze, and parts of North Philly that are seeing renewed interest.

The depreciation math works the same here as anywhere — but because prices are lower, your rental property cash flow is more stable relative to your investment.

DSCR loans are available for investors without traditional income documentation — which matters a lot for people in situations like mine.

The Honest Part

I haven’t done a full buy-and-hold rental play yet — my experience has been on the flip side, literally. But the more I dig into this, the more I think the long-term hold strategy is where the real compounding happens.

The flips give you chunks of cash. The rentals build the foundation.

Understanding all four income streams — rental property cash flow, appreciation, principal paydown, and tax benefits — makes you a way better investor than someone who only looks at monthly rent minus mortgage.

According to BiggerPockets, investors who model all four wealth multipliers — not just rental property cash flow — consistently make better acquisition decisions and hold properties longer, which is where the majority of real estate wealth is actually created.

Use the Multi-Unit Cash Flow Calculator to model the full picture on any Philadelphia rental — plug in rental property cash flow, appreciation assumptions, and principal paydown to see your total annual return before you make any offer.

Not financial advice — just someone doing a lot of research and asking a lot of questions.