I’m going to tell you about the moment I realized that knowing your numbers isn’t just about finding deals — it’s about not getting robbed at the finish line.

This isn’t my story. It’s a video I came across from an investor who owns 31 units and over $4 million in real estate. Someone who clearly knows what they’re doing. And even he almost lost $40,000 because he didn’t read one document carefully enough.

If it can happen to him, it can happen to any of us.

Here’s What Went Down

He was closing on a property he’d contracted at $110,000. During inspections, a sewer line issue came up — $5,800 in damage. He negotiated the price down to $104,000 to account for the repair cost. Clean deal. He also had a hard money loan in place for $150,000 to cover the purchase and renovation.

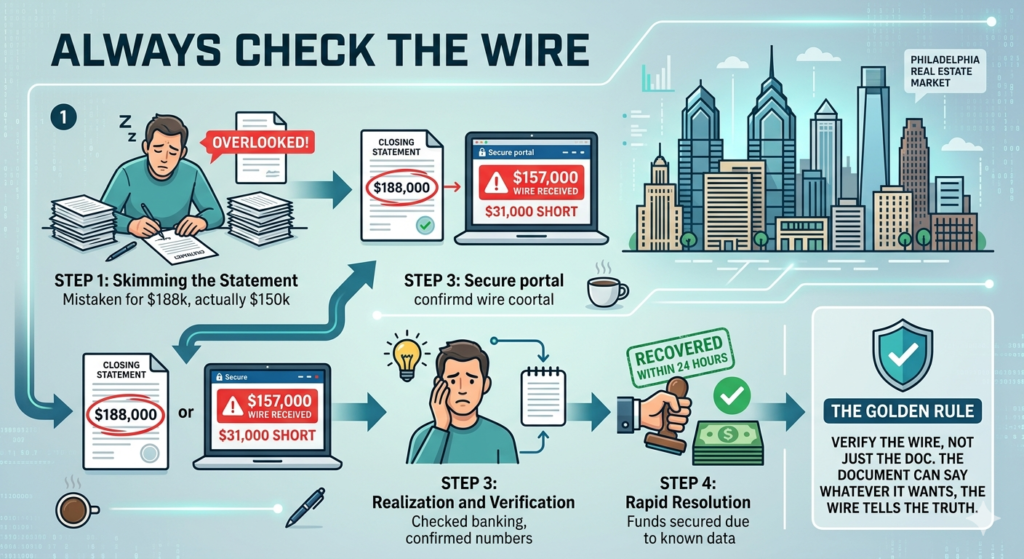

At closing, the closing statement came through.

He was busy. Thirty-one units busy. Multiple deals running simultaneously busy. So when the document landed in his inbox, he did what a lot of people do when they’re stretched thin — he skimmed it and signed.

The closing statement said he owed $188,000 at closing.

That number was wrong. Obviously, badly wrong. But he didn’t catch it in the moment.

He found out something was off when the wire hit his account.

Instead of receiving the $40,000 he was expecting — the difference between his hard money loan and what he owed at closing — he got $9,000.

Thirty-one thousand dollars short.

What Happened Next

Here’s the part that’s actually reassuring: he caught it fast.

Because he knew his numbers cold — what he’d contracted for, what the loan amount was, what he should have walked away with — the second that wire hit, he knew something was wrong.

He made calls. The wholesaler got involved. The title company traced the error. The money that had gone to the wrong place was returned, and within 24 hours, he had the correct amount wired to his account.

Crisis averted. But just barely.

The Three Lines He Said That I Keep Thinking About

“When you’re moving fast, mistakes happen. The question is whether you catch them.”

This hit me hard. He wasn’t saying slow down — he was saying stay sharp. Know your numbers well enough that something off by $31,000 feels wrong immediately, not three weeks later when you’re trying to reconcile your accounts.

“Always check the wire. The document can say whatever it wants — the wire tells the truth.”

This is the one I’m going to remember forever. The closing statement is just paper. The wire is real money moving in the real world. When you close on a property, don’t just wait for the confirmation email — verify the actual amount that landed. Every time.

“Read your closing statements. Every line. Every time.”

Not most lines. Not the summary page. Every. Single. Line. Even when you’re tired. Even when you’ve already signed three other documents that week. Even when the title company seems perfectly competent and you’ve worked with them before.

What Is a Closing Statement, Anyway?

Since I’m still learning this stuff myself, I went back to basics after watching this video.

A closing statement — sometimes called a HUD-1 or a Closing Disclosure — is the document that breaks down every dollar involved in a real estate transaction. It shows:

- The purchase price

- Your loan amount

- Any credits or adjustments (like that sewer line negotiation)

- Closing costs, title fees, prorations

- The final amount you’re receiving or paying

It can be several pages long. There are a lot of line items. And apparently, errors happen — even at professional title companies with experienced staff.

The investor in this video didn’t catch the error on the document. He caught it on the wire. That’s one layer of protection — but ideally, you catch it before money moves at all.

For Philadelphia Specifically

Philadelphia real estate transactions go through title companies, just like anywhere else. And Philadelphia has its own closing cost quirks — realty transfer tax, city wage tax prorations, water/sewer lien searches, and more.

There are more line items than you might expect. More places for something to be entered incorrectly. More reasons to read every single line before you sign anything.

If you’re new to this and you’re not sure what you’re looking at — ask. Ask your real estate attorney. Ask your agent. Ask the title company to walk you through it line by line before closing day. That’s not being difficult. That’s being a competent buyer.

The Real Lesson Here

This investor has 31 units. He’s done this dozens of times. And he still almost lost $40,000 because he was busy and skimmed a document.

I think about where I am in this process — still studying, still learning, nowhere near 31 units — and I’m taking notes. Not because I’m going to be perfect, but because I want to build the habit of checking before I need to.

Know what you’re supposed to receive before you close. Verify the wire when it lands. Read the closing statement line by line, even when you’re tired.

The deal isn’t done until the right number hits your account.

Not financial advice — just someone doing a lot of research and asking a lot of questions.