Most people think if the bank says no, the deal is dead.

It’s not. It just means you need a different structure.

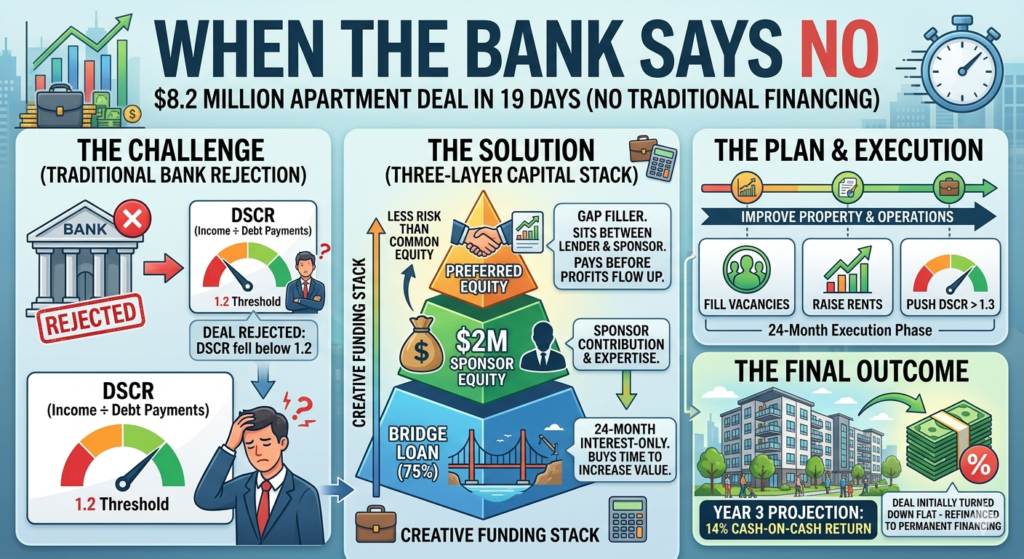

I came across a breakdown of an $8.2 million multifamily acquisition in Mesa, Arizona that got rejected by a traditional lender — and then closed in 19 days using a creative financing stack that I’d never seen explained this clearly before. This one is a little more advanced than my usual posts, but honestly? This is exactly the kind of deal structure I want to understand as I’m working toward larger projects.

Let me break it down piece by piece.

Why the Bank Said No: DSCR

The deal failed traditional bank underwriting because of DSCR — Debt Service Coverage Ratio.

DSCR measures whether a property generates enough income to cover its debt payments. The formula is simple:

DSCR = Net Operating Income ÷ Annual Debt Payments

Banks typically require a DSCR of 1.2 or higher. That means for every $1 of debt payment, the property needs to generate at least $1.20 in net income.

This property didn’t hit 1.2. Maybe the building had vacancies. Maybe rents were below market. Maybe operating expenses were too high. Whatever the reason — on paper, the income wasn’t sufficient to satisfy a traditional lender.

Bank says no. Deal dead? Nope.

The Three-Layer Financing Stack

Instead of one loan from one bank, the team built a three-layer structure:

Layer 1 — Bridge Loan (75% of total cost)

- A short-term loan covering 75% of the acquisition cost

- Interest rate: SOFR + 3.25% (SOFR is a benchmark rate, think of it like a floating base rate)

- Term: 24 months

- Payments: Interest only for the full 24 months — no principal paydown required

Layer 2 — Sponsor Equity ($2 million)

- The investor put in $2 million of their own cash

- This is their skin in the game

Layer 3 — Preferred Equity

- This filled the gap between what the bridge loan covered and what the sponsor could put in

- Return structure: 12% paid currently (monthly cash payments) + 4% accrued (paid later)

- Preferred equity sits between the debt and the common equity — it gets paid before the sponsor profits, but after the lender

Total: $8.2 million acquisition, closed in 19 days.

The Strategy: Lease Up and Stabilize

The 24-month interest-only period wasn’t just a financing convenience — it was the entire strategy.

During those two years, the plan was to:

- Fill vacancies (lease up)

- Push rents to market rate

- Cut unnecessary operating expenses

- Get the DSCR from below 1.2 to above 1.3

Once the property hits 1.3 DSCR, it qualifies for permanent financing — a long-term loan with better terms, lower rates, and a fixed structure. The bridge loan gets paid off and replaced with something sustainable.

By year three, the sponsor was projecting a 14% cash-on-cash return on their $2 million investment. That’s $280,000 per year in cash flow on a deal that a bank initially rejected.

What Is Preferred Equity, Exactly?

This was the part I had to sit with for a minute.

Think of the capital stack like floors in a building:

| Floor | Who | Gets Paid When |

|---|---|---|

| Ground floor | Lender (Bridge Loan) | First — always |

| Middle floor | Preferred Equity | Second — before sponsor profits |

| Top floor | Sponsor (Common Equity) | Last — but biggest upside |

Preferred equity investors get a fixed return (in this case 12% current + 4% accrued) before the sponsor sees any profit. They take less risk than the sponsor, so they get less upside — but they get paid first.

It’s not a loan. It’s not traditional equity. It sits in between — hence “preferred.”

Why This Matters for Philadelphia

You’re probably not doing an $8.2 million deal tomorrow. Neither am I.

But understanding this structure matters because:

DSCR is relevant at every level. Even small multifamily deals in Philadelphia get underwritten on DSCR. If you’re buying a triplex and the numbers don’t work for a conventional loan, a DSCR loan might — and knowing the difference between 1.1 and 1.3 DSCR changes how you underwrite every deal.

Bridge loans exist for smaller deals too. Hard money is essentially a bridge loan for residential investors. Same concept — short term, interest only, buy time to add value, then refinance into permanent financing. That’s literally the BRRRR strategy.

The capital stack concept scales down. Even on a $300,000 Philadelphia rowhouse flip, you have a capital stack — hard money loan, your equity, maybe a partner’s money. Understanding how layers of capital work and who gets paid first makes you a smarter investor at every level.

The Big Takeaway

A bank rejection isn’t a dead end. It’s a negotiation with the capital markets.

This deal got done because someone understood that the property’s current income wasn’t the whole story — the future income, after stabilization, was what mattered. They structured the financing to buy time to get there.

That mindset — seeing a property’s potential rather than just its current state — is what separates investors who find deals from investors who make deals.

I’m still learning how to think this way. But watching how this $8.2 million structure was put together made the whole concept click in a way that reading textbooks never did.

Not financial advice — just someone doing a lot of research and asking a lot of questions.