How to Flip a House Step by Step: From Finding a Deal to Closing with Hard Money (Part 1)

If you want to flip a house step by step — not the theory, but the actual process — this is what I wish existed when I started asking these questions.

I’ve flipped houses before — three times in LA, actually — but always with a partner who handled everything on the ground. I showed up, put in money, and waited for a check. Which means I learned almost nothing about how the process actually works.

Now I’m in Philadelphia, looking at doing this on my own, and I’ve had to basically start from scratch on the operational side. What happens after you find a good deal? Who do you call? How does the money move? What does closing actually look like when you’re using hard money?

No fluff, no theory — just the actual process.

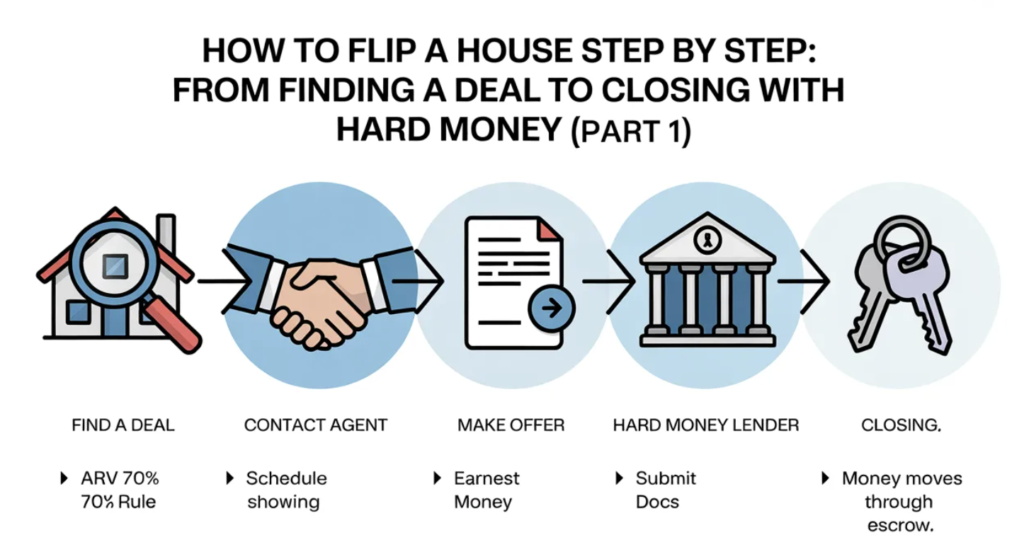

Step 1: You Found a Deal — Now Run the Numbers Again

Let’s say you’ve been running numbers on Zillow or the MLS and something looks promising. The purchase price is low enough, the ARV seems solid, and your gut says this could work.

First thing: don’t fall in love with it yet. Before you call anyone, run the numbers one more time.

The basic formula when you flip a house step by step:

ARV × 70% = maximum all-in cost Maximum all-in cost − estimated renovation = maximum purchase price

So if the ARV is $280k, your max all-in is $196k. If renovation is going to run $60k, you shouldn’t pay more than $136k for the property. If it’s listed at $160k, the deal doesn’t work — move on.

Plug your numbers into the Philly Flip Profit Calculator before you call anyone. If the deal doesn’t pencil out there, it doesn’t pencil out in real life.

If the numbers hold up, now you call a realtor.

Step 2: Contacting a Realtor — What to Actually Say

A lot of beginners don’t realize there are two different realtors in every transaction: the listing agent (represents the seller) and the buyer’s agent (represents you). You want your own buyer’s agent — someone whose job is to get you the best deal, not protect the seller’s price.

When you reach out, be upfront: tell them you’re an investor looking for fix-and-flip opportunities, you’re working with hard money financing, and you can close quickly. Investors who can close fast are attractive to sellers — that’s your leverage.

Your agent will set up showings, pull comps to verify your ARV estimate, and help you figure out a realistic offer price. Listen to them on the comps — they know the local market better than Zillow does.

When you go see the property, you’re not just looking at how bad it is. You’re looking at the bones: foundation issues, roof condition, signs of water damage, the layout. Cosmetic problems are fine and cheap. Structural problems eat your margin alive.

Step 3: Making an Offer

Your agent will draft the offer. A few things to know:

Earnest money — when your offer is accepted, you put down a deposit (usually 1–2% of the purchase price) to show you’re serious. This goes into escrow and gets applied toward your purchase at closing. If you back out without a valid reason, you lose it.

Contingencies — these are your exit ramps:

- Inspection contingency: if the inspection reveals major problems, you can renegotiate or walk away

- Financing contingency: if your financing falls through, you can exit without losing your deposit

Negotiation — the listed price is almost never the final price, especially on distressed properties. On a property that’s been sitting for 60+ days, you have more room. On something that just listed in a hot neighborhood, less so.

When the seller accepts — you’re officially under contract. Clock starts ticking.

Step 4: Under Contract — Lock in Your Hard Money

This is where a lot of first-timers freeze up. You’re under contract, which feels terrifying, and now you need to actually secure the money.

Hard money lenders move fast — most can close in 2–3 weeks. But you need to have a lender you’ve already talked to before you get under contract. Don’t wait until you have a deal to start shopping.

What hard money lenders look at:

- The deal itself — ARV, purchase price, renovation estimate

- Your experience (helpful but not always required for first deals)

- The property — they’ll do their own appraisal or BPO

Most hard money lenders will lend up to 70% of ARV. On that $280k ARV property, they’ll lend up to $196k total — covering both purchase and renovation costs, disbursed in draws as work is completed.

The gap between what they’ll lend and the total cost comes out of your pocket. Plus closing costs, plus points (usually 2–4% origination fee), plus monthly interest (typically 10–15% annualized) while you’re renovating.

This is why knowing how to flip a house step by step — including the financing math — matters before you ever make an offer. Use the Hard Money Loan Calculator to see exactly what your carrying costs will look like month by month.

Documents you’ll typically need:

- Purchase contract

- Renovation scope of work and budget

- Property photos

- Your ID and basic financial info

- Sometimes: proof of funds for your down payment

Once the lender issues a commitment letter, you’re good to move toward closing.

Step 5: Closing — How the Money Actually Moves

Closing is where escrow comes in, and this confuses a lot of people.

Escrow is a neutral third party — usually a title company — that holds funds and makes sure everyone does what they’re supposed to before money changes hands.

Here’s how the money flows:

- Your hard money lender wires the loan funds to escrow

- You wire your down payment and closing costs to escrow

- Escrow verifies everything is in order — title is clear, all documents signed

- Escrow wires the purchase price to the seller

- Title transfers to you — you get the keys

You don’t hand a check to the seller. It all moves through escrow, which protects everyone involved.

Closing costs on the buy side typically run 2–5% of the purchase price and include title insurance, escrow fees, recording fees, and your lender’s origination points. Budget for this — it’s real money on top of your down payment.

And then the property is yours. The clock on your hard money loan starts ticking.

What’s Next

That’s the full flip a house step by step process from offer to keys. According to the National Association of Realtors, distressed property transactions with cash or hard money financing close an average of 2–3 weeks faster than conventional deals — which is exactly why hard money is the standard tool for flippers.

Part 2 covers everything after you own the property: finding and hiring a General Contractor, structuring payments so you don’t get burned, and what your actual day-to-day role looks like during a renovation.

Because owning the property is just the beginning.

Not financial advice — just someone doing a lot of research and asking a lot of questions.