Hard money lenders no money down — that’s the pitch you see everywhere. But what does it actually look like when someone pulls it off?

I’ve been obsessing over a specific case study lately. A $170,000 profit on a flip, funded almost entirely with other people’s money. When I dug into the numbers, the math was more nuanced than the headline — but honestly? Still kind of mind-blowing.

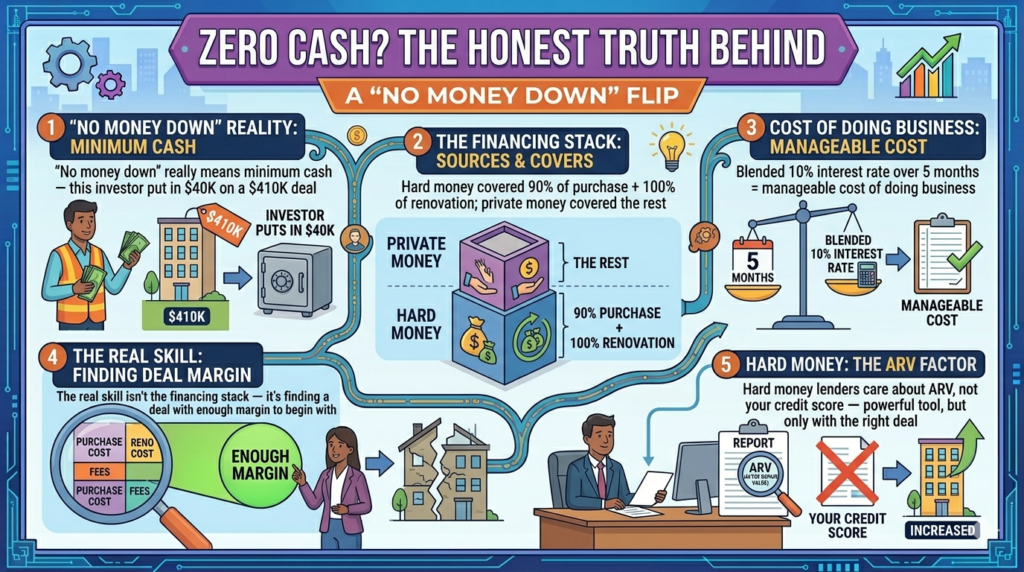

The Myth vs. Reality of Hard Money Lenders No Money Down

The video starts with a bold hook: can you flip a house with zero of your own cash?

Here’s the reality: the investor put down $40,000. In a $410,000 project, that’s still incredible leverage — but it’s not zero. To me, “no money down” really means “minimum cash” or “no life savings required.” It’s about being resourceful, not having deep pockets.

That distinction matters. Because if you go in expecting literally zero out of pocket, you’re going to be caught off guard.

Deconstructing the $410,000 Blueprint

This wasn’t a carpet-and-paint job. This was a house that hadn’t been touched in 30 years.

- Purchase price: $330,000

- Renovation: $80,000 (full gut job)

- ARV (after repair value): $600,000

- Total in: $410,000

- Projected profit: $170,000

To fund it without draining his bank account, he stacked two loans:

- Hard money loan — covered 90% of the purchase + 100% of renovation (8.5% interest)

- Private money loan — covered the remaining 10% of the purchase (12% interest)

Blended rate: 10%. Sounds high — but he held the property for five months. At that timeline, it’s just the cost of doing business.

That’s how hard money lenders no money down deals actually work in practice. Not zero dollars — but close enough that your personal savings stay intact.

Want to stress-test the numbers before you commit? Run it through the Hard Money Loan Calculator first.

What Hard Money Lenders Actually Care About

This is the part most beginners miss. Hard money lenders no money down deals aren’t approved based on your credit score or your W-2. They’re approved based on one thing: the ARV.

After repair value. What the property will be worth once the work is done.

That’s it. If the ARV supports the loan, you’re in. If it doesn’t, no amount of personal income or credit history will save you.

This is why experienced investors spend so much time on comps before they ever call a lender. According to BiggerPockets, underestimating ARV is one of the most common — and most expensive — mistakes new flippers make. You need to know that number cold before you structure anything.

Why Hard Money Lenders No Money Down Only Works If You Find the Right Deal

Here’s what the $170,000 profit number doesn’t tell you: finding a house for $330k that can actually sell for $600k is the hardest part of the whole equation.

That’s the real skill. Not the financing stack — the deal sourcing.

If the margin isn’t there, creative financing won’t save you. Hard money lenders care about the ARV, not your credit score — which is powerful. But if your renovation drags on, those 10% interest payments will eat you alive.

The money is made before you ever sign a contract.

What I Actually Took Away From This

Looking at a projected $170,000 profit puts my own early flip experience in perspective. The gap between a mediocre deal and a life-changing one usually comes down to two things: knowing your local market and understanding the math of your lenders.

Hard money lenders no money down deals aren’t magic. They’re a tool. And like any tool, they’ll work against you if you don’t know how to use them.

Not sure if your deal pencils out with hard money? The Philly Flip Profit Calculator can help you run the numbers before you go too far down the road.

Not financial advice — just someone doing a lot of research and asking a lot of questions.