I’ll be honest — I’ve seen a lot of those videos. You know the ones. Some guy standing in front of a boarded-up house saying he bought it for $200 and he’s going to sell it for $120,000. The comments are full of people losing their minds. “How do I do this??” “This is insane!!” “I’m quitting my job tomorrow!!”

And look, I get it. The number is eye-catching. But I’ve been in and around real estate long enough — three flips, years of studying this market, and a very clear goal of eventually getting into development — to know that when something sounds that simple, the details are usually where it gets complicated.

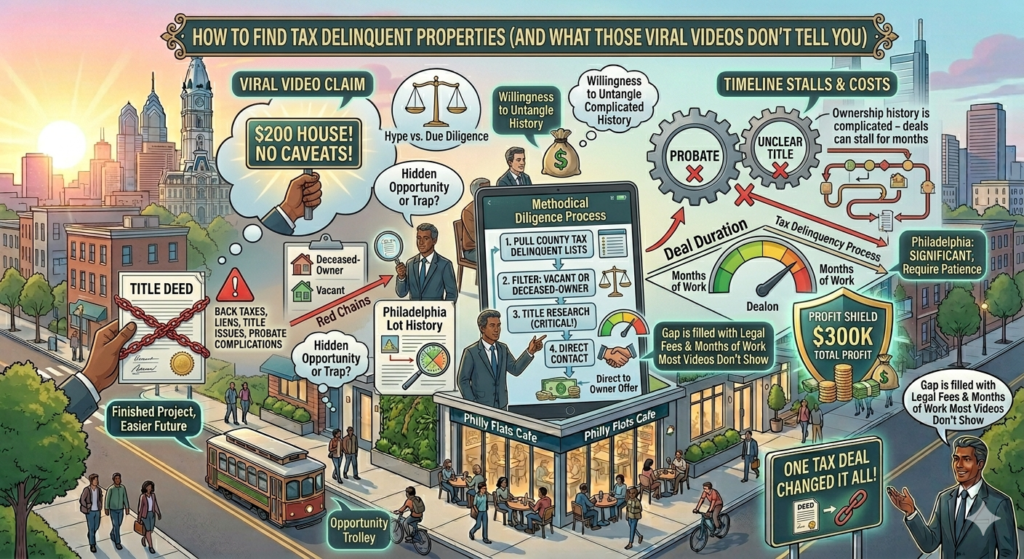

So let me break down what’s actually going on with tax delinquent properties, what the strategy really looks like, and what those viral videos tend to leave out.

What Is a Tax Delinquent Property?

When a property owner stops paying their property taxes, the county keeps a record of it. After enough time passes — this varies by state — the county can move to collect, and in some cases, the property can eventually end up at a tax sale or sheriff sale.

But before it gets to that point, there’s a window. And that window is where some investors focus their energy.

The strategy is straightforward in theory: find properties where taxes haven’t been paid, track down the owner or their heirs, and make an offer before the situation gets worse for them.

The $200 House — What’s Actually Happening There

So about that $200 price tag. Is it real? Technically, yes — it can happen. But here’s the context those videos skip over:

The properties selling for almost nothing are usually in areas with very low demand, severe structural issues, or both. The owner — or more commonly, the heirs of a deceased owner — may have inherited a property they never wanted, can’t afford to maintain, and are actively trying to get rid of. They owe back taxes, the property is deteriorating, and they just want out.

In that situation, yes, someone might take $200 just to be done with it.

But here’s what that $200 doesn’t include: back taxes you may need to clear, title issues, probate complications if the owner is deceased, demolition costs if the structure is unsalvageable, and whatever it actually costs to bring the property to a sellable condition.

The $200 is the acquisition price. It is not the total cost of the deal.

How the Strategy Actually Works

Here’s the legitimate framework, stripped of the hype:

Step 1: Pull the list. Contact your county treasurer or tax assessor’s office and request the list of tax delinquent properties. In most counties this is public record. In Philadelphia, the Office of Property Assessment and the Philadelphia Sheriff’s Office both have public data available.

Step 2: Filter for opportunity. Not every delinquent property is a deal. You’re looking for properties that appear vacant, have a deceased owner, or show signs that the current owner is motivated to sell. Cross-reference with property records to understand ownership history.

Step 3: Do your homework before you make contact. Pull the deed. Check for liens beyond the tax debt. Look up the property on the OPA (Office of Property Assessment) database if you’re in Philly. Understand what you’re actually buying before you call anyone.

Step 4: Make contact. If the owner is alive, reach out directly — letter, phone, door knock. If the owner is deceased, you’re dealing with heirs, which means probate may be involved. This is where things can slow down significantly.

Step 5: Negotiate with realistic numbers. Know your ARV. Know your rehab costs. Know what liens you’re inheriting. Make an offer that actually makes sense as a deal — not just a number that sounds good.

The Part That Takes the Longest: Title and Probate

This is what the $200 house videos almost never mention.

If the owner is deceased and the property wasn’t properly transferred, you may be dealing with an estate that was never probated. That means before you can do anything with the property, someone has to go through the legal process of establishing who actually owns it now.

In Pennsylvania, that process can take months. Sometimes longer if heirs are hard to locate or if there are disputes. And until title is clear, you can’t sell, you can’t finance, and in many cases you can’t even pull permits to renovate.

This doesn’t mean it’s not worth pursuing. It means you need to factor in time, and potentially legal fees, as part of your deal analysis.

Is This Worth Doing in Philadelphia?

Yes — with the right expectations.

Philadelphia has a significant number of tax delinquent and vacancy properties, many with complex ownership histories going back decades. The city also has active programs around land banking and vacancy through the Philadelphia Land Bank, which is worth understanding if you’re serious about this strategy.

The opportunity is real. But the deals that actually work require patience, title due diligence, and a clear-eyed understanding of what you’re getting into. The properties that are genuinely easy to acquire for almost nothing are usually easy for a reason.

The deals worth doing are the ones where you’ve done the homework, you understand the title situation, you know your numbers, and the seller — or the heirs — have a real motivation to move on.

Those deals exist. They just don’t look as clean on camera as a guy holding up a deed and saying “$200.”

What I Actually Think About This Strategy

I’m not dismissing it. Tax delinquent and distressed ownership situations are a legitimate corner of real estate investing, and I think there’s real opportunity in Philadelphia specifically given the city’s inventory of older, complicated properties.

But I watch those viral videos the same way I watch any too-good-to-be-true pitch — with one eyebrow up. The strategy is real. The $200 number is technically possible. The part between “I bought it for $200” and “I sold it for $120,000” is where months of work, legal fees, and carrying costs tend to live.

It’s not easy. But it is simple — that part, at least, I agree with.

Not financial advice — just someone doing a lot of research and asking a lot of questions.