HUD home purchase with $100 down sounds like a guru pitch. It’s not — it’s an actual government program. Not $10,000. Not $5,000. One hundred dollars.

Let me explain exactly how it works, who qualifies, and what the catches are.

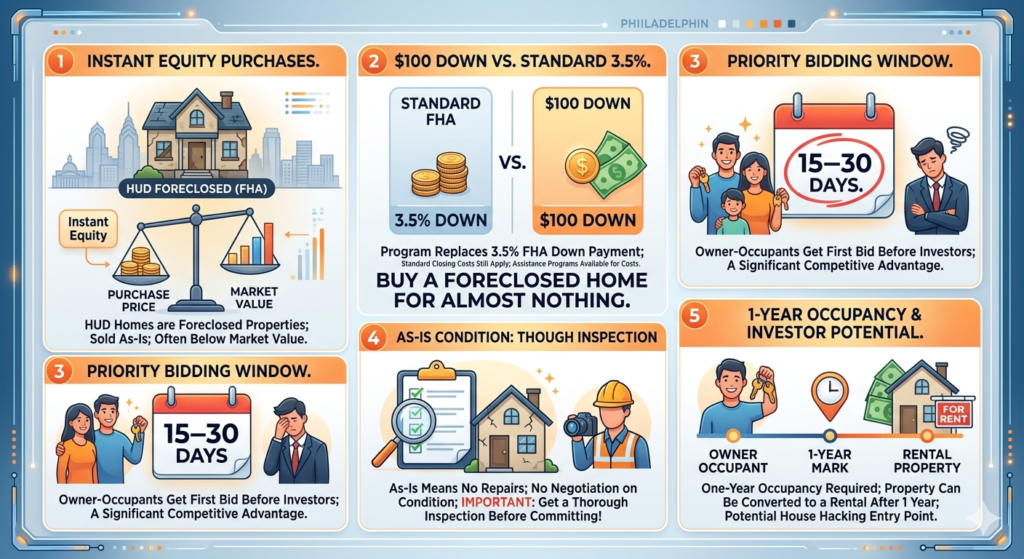

What Is a HUD Home Purchase?

Before you can understand the $100 down program, you need to understand what a HUD home actually is.

When someone buys a house using an FHA loan and then defaults, the lender forecloses. Because the loan was FHA-insured, the FHA pays the lender back for their loss. In exchange, the FHA takes ownership of the property — which is then transferred to HUD for sale.

HUD home purchases are sold as-is. No repairs, no warranties, no negotiation on condition. What you see is what you get — and what you get is usually a property that needs work, which is exactly why the price is often below market value.

That discount is where the opportunity lives.

The HUD Home Purchase $100 Down Payment Program

Standard FHA financing requires 3.5% down. On a $200,000 home, that’s $7,000 before closing costs.

HUD’s $100 Down Payment Program cuts that to exactly $100 — on qualifying HUD-owned properties, purchased with FHA financing, by owner-occupants.

Key requirements for the HUD home purchase $100 down program:

- The property must be a HUD-owned home listed on HUDHomeStore.gov

- You must finance with an FHA loan

- You must intend to live in the property as your primary residence for at least one year

- The offer must be at list price (HUD sets the price — you don’t negotiate it down)

- You must work with a HUD-registered real estate agent

What you still pay: The $100 replaces the down payment — but closing costs (typically 2–5% of the purchase price) still apply. The good news: closing costs can often be covered through government assistance programs, seller concessions, or lender credits.

In Philadelphia specifically, the Philadelphia Home Buy Now program and various PHFA grants can be stacked on top of this HUD home purchase program.

Why HUD Sells at a Discount

HUD is not in the business of being a landlord or property manager. They want these properties sold quickly, to owner-occupants who will stabilize neighborhoods.

Because HUD home purchases are sold as-is and HUD prioritizes speed over maximum price, they’re often listed below what a fully renovated comparable would sell for. That gap between purchase price and actual market value is instant equity — before you’ve done a single repair.

The Owner-Occupant Priority Window in HUD Home Purchase

HUD doesn’t open bidding to everyone at once. There’s a priority period — typically the first 15–30 days a property is listed — where only owner-occupants can submit offers. Investors can’t bid during this window.

This matters because you’re not competing against cash investors who can close in two weeks. You’re competing against other owner-occupants on a more level playing field.

If a property sits through the owner-occupant window without an accepted offer, it opens to investors — and prices can move. Getting in during the priority window on any HUD home purchase is almost always better.

FHA 203k: When the HUD Home Purchase Property Needs Serious Work

HUD home purchases are sold as-is. Some need cosmetic work. Some need significant repairs. And some need so much work that a standard FHA loan won’t cover them — because FHA has minimum property condition requirements that a heavily distressed property might not meet.

This is where the FHA 203k loan comes in. The 203k combines your purchase price and renovation costs into a single loan — wrapping everything together instead of scrambling for renovation financing separately.

Philadelphia’s older housing stock — row homes built in the early 1900s with outdated electrical, aging plumbing, and deferred maintenance — is exactly where 203k financing makes the HUD home purchase work when standard FHA won’t.

The Real Catches in HUD Home Purchase

Inventory is limited and unpredictable. HUD homes come to market when FHA-backed loans default. You can’t control the timing or location. Set up alerts on HUDHomeStore.gov for Philadelphia County — good properties move fast during the owner-occupant window.

As-is means as-is. HUD will not make repairs. If the inspection reveals a major problem — foundation issues, serious mold, environmental hazards — you either accept it, negotiate a price reduction (sometimes possible), or walk away and lose your earnest money deposit. Get a thorough inspection. Don’t skip it because the price is attractive.

The one-year occupancy requirement. You must live in the property for at least one year. Using the $100 down HUD home purchase program to immediately rent out is occupancy fraud. After one year, you can convert to a rental, move out, or do whatever you want.

Policy changes. HUD programs are subject to policy changes. The $100 down program has been modified and suspended in various states at various times. Verify current availability in Pennsylvania with a HUD-registered agent before building a strategy around it.

According to HUD.gov, the $100 Down Payment Program is available on select HUD-owned properties and is subject to change based on HUD inventory and policy — always confirm current program terms with a HUD-registered agent before making an offer.

How to Actually Complete a HUD Home Purchase

Step 1: Get pre-approved for an FHA loan. Know what you can afford and have a pre-approval letter ready before you look at properties.

Step 2: Find a HUD-registered real estate agent. You must use a HUD-registered agent to submit offers — you can’t do it yourself. HUDHomeStore.gov has an agent search tool.

Step 3: Search HUDHomeStore.gov for Philadelphia listings. Filter by county. Pay attention to the bid deadline and whether the property is in the owner-occupant priority period.

Step 4: Do your homework before bidding. Drive by the property. Review the Property Condition Report HUD provides. Check the neighborhood.

Step 5: Submit your offer at list price. The $100 down program requires an offer at list price. Your agent handles the submission through HUD’s bidding system.

Step 6: Get a full inspection immediately. Your due diligence period is typically 15 days. Use all of it.

Step 7: Close with your FHA lender. Standard FHA closing process, minus the $7,000+ down payment.

Use the Philadelphia Homebuyer Assistance Calculator to model how HUD home purchase programs stack with Philadelphia-specific down payment and closing cost assistance before you make any offer.

Not financial advice — just someone doing a lot of research and asking a lot of questions. HUD program availability and terms vary by state and change over time — verify current conditions with a HUD-registered agent or FHA lender before making any decisions.