Yeah. Let that sink in.

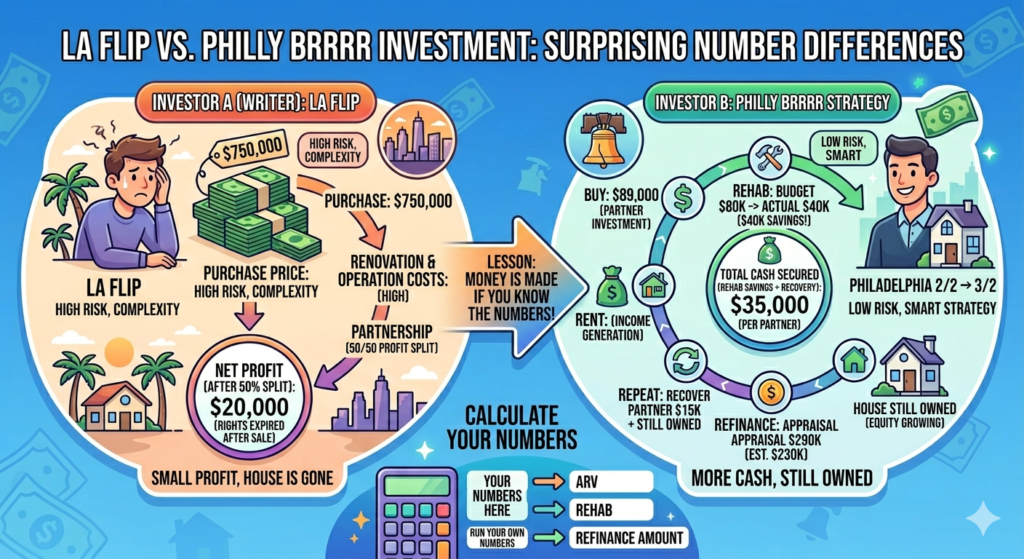

A few years back, I did my first house flip in LA. The purchase price was somewhere in the $700K–$800K range — very LA, very stressful, very “oh god what am I doing.” I handed off most of the heavy lifting to a company that co-managed the project with me, and we split the profits 50/50.

After everything — the renovation, the fees, the holding costs, the split — I walked away with about $20,000.

Twenty thousand dollars. On a three-quarter-million-dollar deal.

I wasn’t mad exactly. It was my first flip. I learned a ton. But I also remember thinking… this doesn’t feel right.

Fast forward to now. I’m deep in the Philadelphia market, studying deals constantly, and I came across this investor’s story that genuinely stopped me mid-scroll.

Here’s what happened:

He bought a 2bed/2bath for $89,000. His partner covered the purchase price and renovation costs. They budgeted $80K for rehab — and only spent $40K. That $40K in savings? Split evenly. Each partner pocketed $20K just from coming in under budget.

They also bumped the layout from 2 bedrooms to 3 — which matters a lot for appraisal value.

The investor conservatively estimated ARV at $230K. The actual appraisal came in at $290K.

Then they did a cash-out refinance. Each partner pulled out another $15K.

Total per partner: $35,000 — and they still own the property.

No sale. No exit. The house is sitting there building equity while they’ve already been paid.

Why did I walk away with less on a deal 8x the size?

Honestly? A few reasons.

In LA, margins are brutal. You’re working with high purchase prices, high labor costs, and buyers who expect perfection. One surprise (and there’s always a surprise) eats your profit fast.

But the bigger issue was that I didn’t really know what I was doing. I outsourced the knowledge along with the labor. I handed over control — and with it, a huge chunk of the upside.

This investor did something different. He kept his numbers conservative on purpose. He said something like: underestimate your ARV, spend less than you planned on rehab, and let the deal surprise you.

That’s not luck. That’s discipline.

The real lesson here isn’t “buy cheap houses.”

It’s that the more you understand your numbers — your rehab budget, your ARV, your refi math — the more of your own money you actually keep.

I’ve been studying this stuff obsessively since moving to Philadelphia, and I’m still learning. But every time I dig deeper, I find more money that I was leaving on the table before.

If you’re planning a BRRRR deal or thinking about a cash-out refi, run your numbers before you commit. Know what you expect, know what’s conservative, and know where you can come in under.

I built a calculator below to help with exactly that — plug in your deal and see what a cash-out refi could look like for you.