I’ve been spending a lot of time lately researching what it actually takes to get financing for a real estate investment in Philadelphia.

My credit scores are decent — around 750 on Experian and close to 800 on the others. I thought that was the hard part. I thought if your credit score was good, the rest would follow.

It turns out credit score is just the beginning.

The more I dug into how lenders actually evaluate borrowers — conventional lenders, hard money lenders, DSCR lenders — the more I realized that most people, including me, have been thinking about this wrong. Your credit score gets you in the door. What happens after that is a completely different conversation.

Here’s what I’ve learned.

What Your Credit Score Actually Does

Your credit score is a three-digit number that tells lenders how reliably you’ve paid back debt in the past. It’s calculated based on payment history, amounts owed, length of credit history, new credit, and credit mix.

For real estate lending, here are the general benchmarks:

760 and above: Best rates and terms available 720 to 759: Very good — most programs available 680 to 719: Good — some restrictions may apply 620 to 679: Fair — limited programs, higher rates Below 620: Difficult — hard money only, higher rates and stricter terms

A score in the 750 to 800 range puts you in a strong position for most loan programs. That’s genuinely good news. But it doesn’t mean approval is automatic.

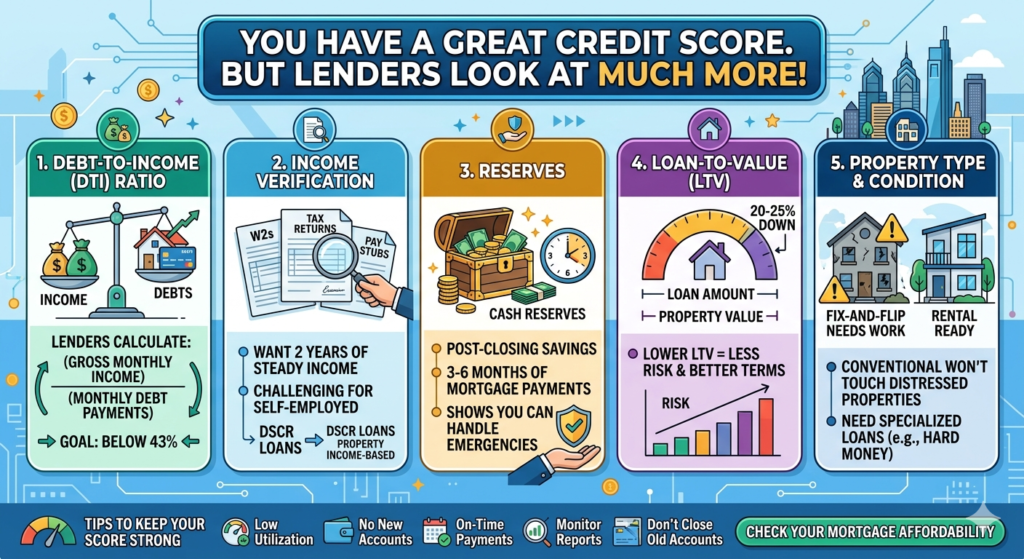

What Lenders Look at Beyond Your Score

This is the part most people don’t talk about.

Debt-to-Income Ratio (DTI)

For conventional loans, lenders calculate how much of your gross monthly income goes toward debt payments. Most want to see a back-end DTI below 43% — meaning all your monthly debt payments combined should be less than 43% of what you earn before taxes.

If you don’t have verifiable income — if you’re self-employed, between jobs, or building something new — your DTI calculation gets complicated fast. This is one reason why DSCR loans exist. They skip the personal income calculation entirely and focus on the property’s income instead.

Income Verification

Conventional lenders want two years of tax returns, W2s, or documented self-employment income. If you can’t show consistent, verifiable income, conventional financing becomes very difficult regardless of your credit score.

For investors in non-traditional income situations, this is often the real obstacle — not the credit score.

Reserves

Most lenders want to see that you have cash left after closing. Typically 3 to 6 months of mortgage payments sitting in an account you own. This proves you can handle the loan even if something goes wrong in the first few months.

If your credit score is excellent but your bank account is empty, many lenders will decline you anyway.

Loan-to-Value

Lenders look at how much you’re borrowing relative to the value of the property. Lower LTV means less risk for them and better terms for you. If you’re putting 20% to 25% down, you’re in a much stronger position than someone putting 5% down — even if the credit scores are identical.

Property Type and Condition

Conventional lenders won’t touch distressed properties. If you’re buying a fix-and-flip or a property that needs significant work, you need a loan product specifically designed for that — like a hard money loan or a renovation loan. A perfect credit score doesn’t change that requirement.

How to Keep Your Score Strong While Preparing to Invest

Since my scores are already in decent shape, my focus right now is on protecting them while I prepare for my first investment.

Keep utilization low. Credit utilization — how much of your available credit you’re using — has a significant impact on your score. Keeping balances below 30% of your limits helps. Below 10% is even better.

Don’t open new accounts unnecessarily. Every hard inquiry from a new credit application can temporarily lower your score. Before you’re ready to apply for a real estate loan, avoid opening new credit cards or taking on new debt.

Pay everything on time. Payment history is the single biggest factor in your credit score. One missed payment can drop a good score significantly. Set up autopay for everything.

Monitor all three bureaus. Experian, Equifax, and TransUnion can have different information. Check all three regularly for errors — errors are more common than most people realize, and they can drag down your score for no reason. Dispute anything that looks wrong immediately.

Don’t close old accounts. Length of credit history matters. Closing an old credit card you don’t use can actually hurt your score by shortening your average account age.

What This Means for My Situation

My credit scores are not the problem. That’s genuinely useful to know.

What I’m working on now is the other pieces — building verifiable income, understanding which loan products match my situation, and finding the right deals so that when I’m ready to move, I can move quickly and confidently.

The credit score is the foundation. But a foundation alone doesn’t build anything. You still have to do the work.

Use the free Mortgage Affordability Calculator below to see what your numbers look like when you’re ready to apply.