I came across a TikTok video talking about buying land, dropping a double-wide on it, and selling the whole package for $50K profit per deal. My first reaction was skepticism. My second reaction was — wait, let me actually look into this.

So I did. And here’s what I found after going deep on the mobile home investing strategy that nobody in “real” real estate talks about — because they’re too busy laughing at the idea.

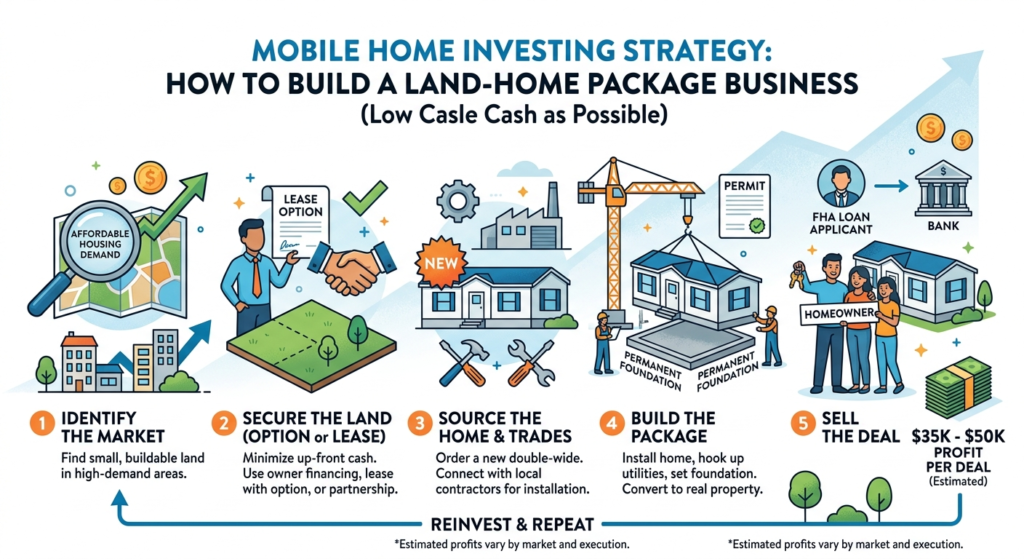

Mobile Home Investing Strategy: What It Actually Is

The model is simple. You find a small piece of buildable land in a market where affordable housing demand is real. You buy it. You install a new double-wide manufactured home on a permanent foundation. You sell the land-home package to a buyer who finances it with an FHA or conventional loan.

That’s it. No tenants. No long-term management. No giant rehab surprises hiding behind 1920s plaster walls.

The numbers that get thrown around — $35K to $50K profit per deal — are not fantasy. This strategy works by combining two undervalued assets: cheap rural land most investors ignore, and affordable manufactured housing that 21 million Americans currently call home. Together they create something worth more than the sum of their parts. Landydandy

Why the Math Works (Even If People Laugh at You)

A new double-wide manufactured home averages around $145,700 — roughly 66% less expensive than a comparable site-built home. When you pair that with a piece of land, convert it to real property via permanent foundation, and sell it as a complete package, your buyer gets an affordable home with real financing options. You get a margin. Amerisave

The key insight: you’re not just selling a mobile home. You’re solving a housing problem. Manufactured homes now represent approximately 10% of new single-family construction in the U.S., and average sales prices have climbed 58% between 2018 and 2023. Demand isn’t going away. Amerisave

The Permanent Foundation Rule — This Is Everything

Here’s what separates a smart mobile home investing strategy from a stuck deal. If the home is permanently affixed to land the buyer owns, you can finance both the home and land with a single mortgage — FHA, VA, conventional, or USDA all become available options. Amerisave

If you skip the permanent foundation, your buyer is stuck with a chattel loan. Chattel loans carry interest rates 2 to 5 percentage points higher than traditional mortgages, with shorter terms of 15 to 23 years — meaning higher monthly payments and a much smaller buyer pool. Amerisave

Permanent foundation = more buyers = faster sale = higher price. Budget for it from day one.

Zoning: The First Thing You Check, Not the Last

Before you fall in love with any piece of land, check the zoning. Zoning laws dictate whether manufactured homes are permitted, and violations can result in penalties or the complete inability to place a home on the property at all. The Land Geek

Rural and agricultural zones (A-1, AG) are typically the most permissive for manufactured home placement. Standard residential zones may require permanent foundations and specific aesthetic standards like skirting, roofing pitch, and minimum square footage. RealMobileHomes

Call the county planning office before you make an offer. This is a five-minute phone call that can save you from a very expensive mistake.

Mobile Home Investing Strategy: Doing 5 Deals Without Using All Your Cash

Here’s where I spent the most time thinking. Because one deal sounds doable. Five deals — which is what you’d need to hit $200K in a year — is a different conversation.

The key thing to understand: you are not the one getting the FHA loan. Your buyers are. FHA is owner-occupant financing — one loan, one primary residence. As the investor building and selling multiple packages, you need a completely different financing stack.

Here’s how to structure it with as little of your own money as possible:

Land acquisition: Look for seller financing on raw land. Motivated landowners — especially in rural markets — will often carry the note themselves, sometimes with little or no money down. You’re buying land that most investors aren’t touching, which gives you negotiating leverage. Use our land potential analyzer to vet parcels before you make an offer.

Manufactured home purchase: Most manufactured home dealers offer their own in-house financing or work with specialty lenders. Some will finance the home separately from the land, which means you can potentially control both assets with minimal cash upfront — then combine them on the permanent foundation before selling.

Construction and installation costs: This is where you need either a private money partner or a construction line. A private money lender who understands the model can bridge the gap between your purchase costs and your sale price. If the home is later converted to real property on owned land, borrowers may qualify for FHA, VA, USDA, or conventional refinancing — which means your buyer’s financing on the back end is clean, even if your acquisition financing is creative. Capital Home Mortgage

The sequential approach: Trying to fund five packages simultaneously ties up a lot of capital before a single dollar comes back. A smarter play — especially starting out — is deal one funds deal two. You close the first package, take the profit, roll it into the next land purchase. Slower to $200K, but you’re not overleveraged while you’re still learning the market.

What to Research Before You Do Anything

I’m deep in research mode on this one, and here’s the checklist I’ve built for myself:

Demand first. Talk to local real estate agents in your target market. Check recent manufactured home sales. If they’re sitting for six months, that’s your answer. If they’re moving in 30 days, that’s a different story.

Zoning before the offer. Call the county. Ask specifically whether a new double-wide on a permanent foundation is permitted on the parcel you’re looking at.

Utility availability. Before buying land, verify zoning permissions, utility availability, flood zone status, soil and septic suitability, and access and easements. Rural land without water and sewer hookups adds cost and complexity fast. Cbisaacrealty

Dealer relationships. Find a manufactured home dealer in the region who’s done land-home packages before. They’ll know the local permitting process, foundation contractors, and sometimes even have financing relationships already set up.

Exit strategy before you buy. Are you selling retail to an owner-occupant? Owner-financing to a buyer who can’t get a bank loan? Renting as a long-term hold? Each exit has different math. Know yours before you write the check.

The Honest Reality Check

This mobile home investing strategy is real, repeatable, and genuinely solves a housing problem that isn’t going away. But it’s not a one-click TikTok business. The people doing it well have spent time building dealer relationships, understanding local zoning, and finding markets where manufactured home demand is actually strong.

The math on a single deal is straightforward. The challenge is execution — permits, foundation contractors, utility hookups, buyer financing — all of which require local knowledge you have to build from scratch if you’re coming in from the outside.

I’m not doing this tomorrow. But I’m paying close attention.

Not financial advice — just someone doing a lot of research and asking a lot of questions.