What a $300,000 Mortgage Actually Costs You in Philadelphia — Month by Month

Mortgage Philadelphia investment property math is something most buyers glance at once and never look at again. That’s a mistake.

Most people know their monthly payment. Very few know what they’re actually paying for.

When you make a mortgage payment, the money doesn’t all go toward paying down your loan. In the early years of a 30-year mortgage, the majority of every payment goes straight to the lender as interest. The portion that actually reduces your balance — the principal — is surprisingly small at first.

I didn’t fully understand this until I started studying real estate seriously. Once I did, it changed how I think about every property decision I make.

The Numbers on a Mortgage Philadelphia Investment Property at $300,000

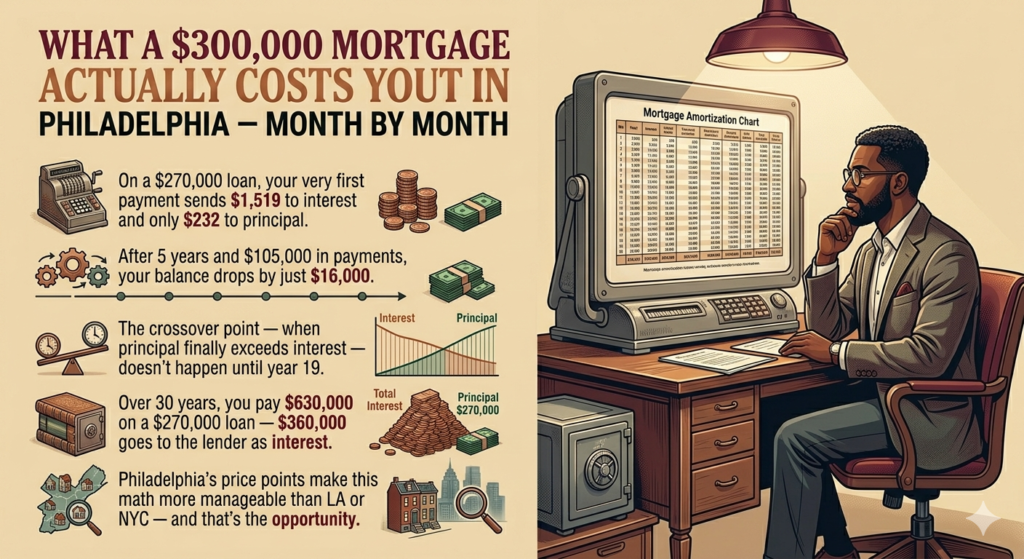

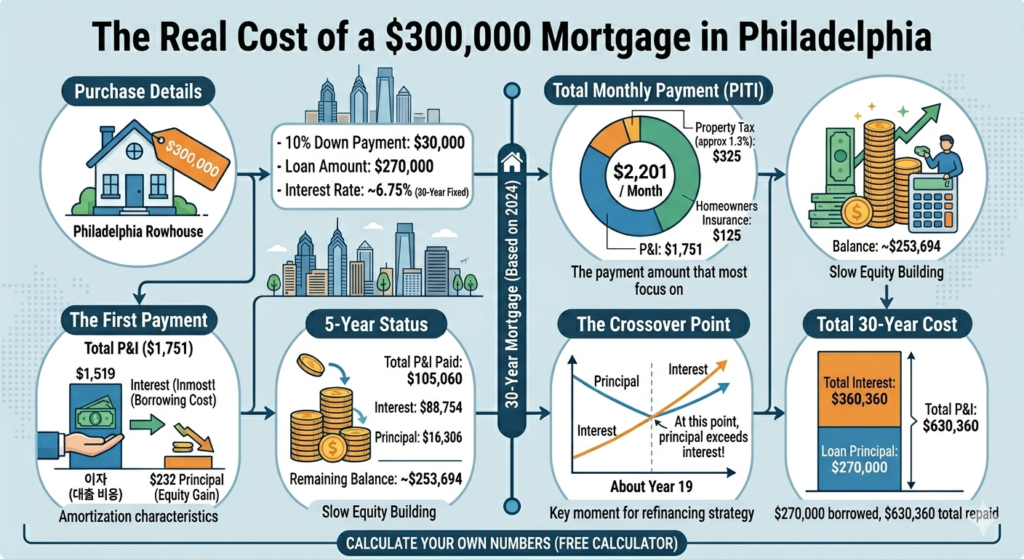

Let’s use a real example. A $300,000 rowhouse in Philadelphia. You put 10% down — $30,000. Your loan amount is $270,000. At approximately 6.75% on a 30-year fixed mortgage:

- Principal and interest: $1,751/month

- Philadelphia property tax (~1.3% annually): $325/month

- Homeowner’s insurance: ~$125/month

- Total monthly payment (PITI): ~$2,201/month

That’s the number most people focus on. But it’s not the whole story.

What Your First Payment Actually Does

In your very first payment of $1,751 in principal and interest:

- Interest: $1,519

- Principal: $232

You paid $1,751. Only $232 reduced your loan balance. The other $1,519 went to the lender as the cost of borrowing.

This is how amortization works. Your loan is structured so you pay proportionally more interest when the balance is high, and more principal as the balance decreases over time.

The First Five Years of a Mortgage Philadelphia Investment Property

After 60 payments — five years at $1,751 every month:

- Total paid: $105,060

- Total interest paid: $88,754

- Total principal paid: $16,306

- Remaining balance: ~$253,694

You’ve paid over $105,000 and your loan balance dropped by only $16,000. That’s the reality of a 30-year mortgage in the early years.

It’s not a reason to panic. It’s a reason to understand what you own and plan accordingly.

According to the Consumer Financial Protection Bureau, amortization schedules are required to be disclosed at closing — but most buyers never read them carefully enough to understand where their money is actually going.

The Crossover Point

There’s a moment in every 30-year mortgage when your monthly principal payment finally exceeds your monthly interest payment. On this loan, that crossover happens around year 19.

Before year 19, more of every payment goes to interest than principal. After year 19, more goes to principal than interest.

This is why real estate investors talk about refinancing and equity strategies so much. In the early years of a mortgage Philadelphia investment property, you’re building equity slowly — primarily through appreciation, not paydown.

The Total Cost of a 30-Year Mortgage

Over the full life of this loan:

- Total principal and interest payments: $630,360

- Original loan amount: $270,000

- Total interest paid over 30 years: $360,360

You borrowed $270,000. You paid back $630,000. The difference — $360,000 — is what the lender earned.

In Philadelphia, where $300,000 buys you a real house in a real neighborhood, understanding this math gives you options that buyers in more expensive markets simply don’t have.

The 15-Year Alternative

If you can afford the higher payment, a 15-year mortgage dramatically changes the math.

On the same $270,000 loan at 6.25%:

- Monthly principal and interest: $2,315

- Total interest over 15 years: $146,700

You save over $213,000 in interest compared to the 30-year. The tradeoff is $564 more per month.

For investors with strong cash flow, the 15-year builds equity faster and costs significantly less. For buyers who need the lower payment to qualify or maintain cash reserves, the 30-year makes more sense. There’s no universally correct answer.

What This Means for Philadelphia Investors

If you’re buying a primary residence, the math above is simply the cost of homeownership.

If you’re buying a mortgage Philadelphia investment property, the calculation looks different. Your tenant’s rent covers the mortgage payment — including that heavy interest load in the early years. Meanwhile, appreciation is building your equity from the top down even while principal paydown does so from the bottom up.

This is why buy-and-hold investors who bought in neighborhoods like Point Breeze and Germantown five to ten years ago are sitting on significant equity today — not primarily because they paid down their mortgages, but because the market moved.

Want to see your exact monthly payment, total interest, and full amortization schedule? Run it through the Mortgage Calculator before you make any offer.

Ready to see what mortgage rate you actually qualify for? Get free quotes from multiple lenders in minutes — no commitment required. 👉 Check Your Mortgage Rate on LendingTree

Not financial advice — just someone doing a lot of research and asking a lot of questions.