I’ve been watching a lot of real estate content lately — occupational hazard when you’re trying to learn this stuff — and I keep coming across strategies that sound almost too clever to be real.

Subject To financing. Seller Financing. Creative financing. These terms get thrown around a lot in investing circles, but nobody seems to explain them clearly or honestly.

So here’s my attempt at that. What they actually are, how they’re different, when they work, and what can go wrong.

First: Why These Strategies Exist

Both of these strategies exist because traditional bank financing has real limitations.

Mortgage rates hovering near 6.15% are locking millions of homeowners into their current properties. Meanwhile, investors with complicated income situations — self-employed, heavy tax deductions, multiple properties — often can’t qualify for conventional loans even when they’re financially strong. LJC Financial

Creative financing fills that gap. Instead of going through a bank, the deal gets structured between buyer and seller directly. And in a market like Philadelphia, where there’s a wide range of property conditions, motivated sellers, and savvy investors, these strategies come up more than you’d think.

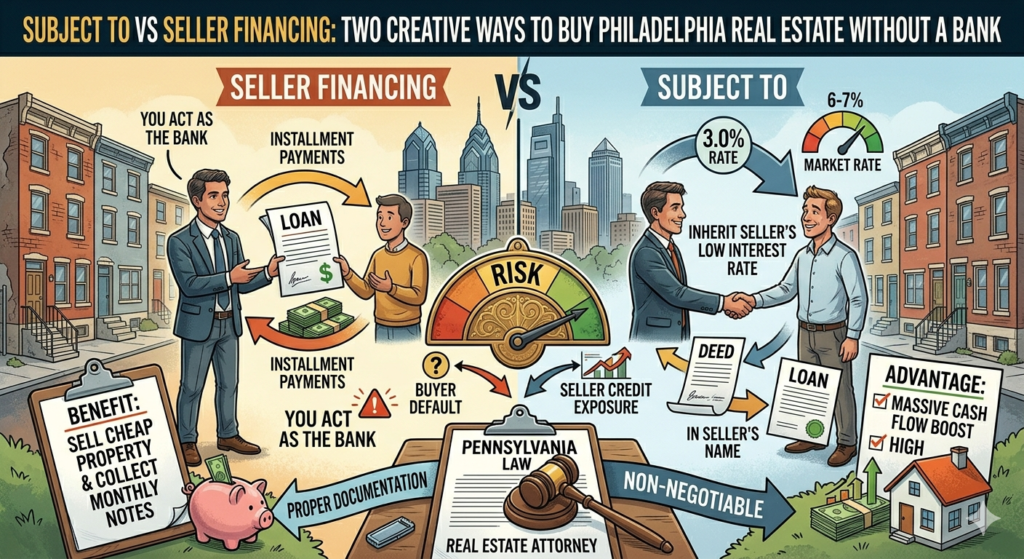

Seller Financing: You Become the Bank

Seller financing is exactly what it sounds like. Instead of the buyer going to a bank for a mortgage, the seller provides the financing directly.

Here’s how the “Loan & Own” version of this works — a strategy I’ve seen getting a lot of attention lately:

- You buy a distressed property cheap — say $30,000 cash

- You sell it to a buyer for $69,000

- Instead of the buyer getting a bank loan, you carry the financing yourself

- The buyer pays you monthly — principal and interest — like a mortgage payment

- You hold a 30-year note and collect payments every month

- No tenants. No 2am maintenance calls. No toilets.

The seller acts as the bank, creating a new financing agreement with the buyer. You own the note, not the property. And if the buyer defaults, you can foreclose and get the property back — then do it again. PeerStreet

The appeal is obvious: passive income without being a landlord. Monthly checks without dealing with tenants.

The catch:

The buyer pool for seller-financed properties tends to be people who can’t qualify for a conventional mortgage. That’s not always a bad thing — plenty of solid, hardworking people have credit issues for legitimate reasons. But it does mean your buyer may be higher risk than a typical bank-qualified purchaser.

If your buyer stops paying, you have to go through the foreclosure process — which in Pennsylvania takes time and costs money. And the $30,000 properties that make this model work tend to be in markets that are… not exactly Philadelphia’s growth neighborhoods. Know what you’re buying and where.

Subject To: Taking Over Someone Else’s Mortgage

Subject To is a completely different animal.

Subject-to financing means a buyer takes control of a property while the existing mortgage stays in the seller’s name. Instead of applying for a new loan, the buyer agrees to make payments on the seller’s current mortgage. The deed transfers to the buyer, but the mortgage stays in the seller’s name. Amerisave

In plain English: the house becomes yours, but the loan stays in the previous owner’s name. You make the payments. They just… go away.

Why would a seller agree to this?

Usually because they’re in trouble. Subject-to deals often happen when sellers want to exit quickly or when buyers have difficulty qualifying for loans — sellers facing foreclosure, behind on payments, or going through life changes that make a quick exit more important than maximizing price. Amerisave

Why would a buyer want this?

Two big reasons:

First, speed. Without the need for loan approval, deals can close quickly — often within days or weeks. Amerisave

Second — and this is huge right now — interest rates. If the seller’s mortgage has a low interest rate, the buyer benefits from those terms. If someone bought a house in 2021 at 3% and you take over their mortgage Subject To, you’re now paying 3% interest in a 6-7% market. That’s an enormous advantage that translates directly into cash flow. Templeviewcap

The risks — and they’re real:

Most mortgages include a due-on-sale clause allowing lenders to demand full repayment if ownership changes. This can trigger foreclosure if the lender enforces it. In practice, lenders rarely enforce this as long as payments are being made — but it’s a real legal risk that you need to understand going in. Amerisave

Since the loan remains in the seller’s name, missed payments by the buyer can damage the seller’s credit. This is why sellers who agree to Subject To deals need to trust the buyer, and why buyers need to be serious about keeping payments current. Amerisave

You also don’t have a direct relationship with the lender. The buyer cannot modify loan terms — you’re locked into whatever terms the seller originally had. Amerisave

Side by Side: Which Is Which

| Seller Financing | Subject To | |

|---|---|---|

| Who holds the loan | You (the seller/investor) | Original lender (in seller’s name) |

| New loan created | Yes | No |

| Best for | Selling cheap properties for passive income | Acquiring properties with assumable low rates |

| Main risk | Buyer default, foreclosure process | Due-on-sale clause, seller credit exposure |

| Down payment needed | Negotiable | Usually small (cover arrears) |

| Interest rate | You set it | Whatever seller had |

How These Play in Philadelphia Specifically

Philadelphia’s market creates some interesting opportunities for both strategies.

On the Seller Financing side: there are genuinely distressed properties in certain neighborhoods that can be acquired cheaply and sold via owner financing to buyers who want to own but can’t get conventional loans. The demand is real — buyers who struggle to qualify for traditional loans can still purchase homes this way. Amerisave

On the Subject To side: Philadelphia has a lot of long-term homeowners who bought years ago at much lower rates. Some of them are now in situations — estate sales, divorces, financial hardship, relocation — where a quick exit matters more than price. Those 3-4% mortgages from 2019-2021 are gold right now, and Subject To is how investors access them.

In 2025, roughly 15% of traditional real estate contracts fell through due to financing issues. Creative financing solves exactly that problem — for both buyers and sellers. Delaware County

The Honest Reality Check

Both strategies require more sophistication than a typical purchase. You need:

- A real estate attorney who understands Pennsylvania law — not optional

- A clear understanding of the risks going in

- Honest conversations with sellers about what they’re agreeing to

- Proper documentation for everything

Subject To especially needs legal guidance. The due-on-sale risk is real, and the documentation needs to protect both parties. Don’t try to do this without a lawyer who’s done it before.

Seller Financing is more straightforward legally, but you’re essentially becoming a lender — which means you need to think like one. Credit checks on your buyer, proper note documentation, understanding your foreclosure options if things go sideways.

Neither of these is a shortcut. They’re tools — and like any tool, they work great when used correctly and can cause real damage when used carelessly.

Want to see if the numbers work on a creative financing deal? Use the calculator below to model your cash flow.