Preferred equity real estate financing closed an $8.2 million multifamily deal that a traditional bank rejected — in 19 days.

Most people think if the bank says no, the deal is dead. It’s not. It just means you need a different structure. I came across a breakdown of this acquisition in Mesa, Arizona that got rejected by a traditional lender and then closed using a creative financing stack I’d never seen explained this clearly before.

This one is a little more advanced than my usual posts. But this is exactly the kind of deal structure I want to understand as I’m working toward larger projects. Let me break it down piece by piece.

Why the Bank Said No: DSCR

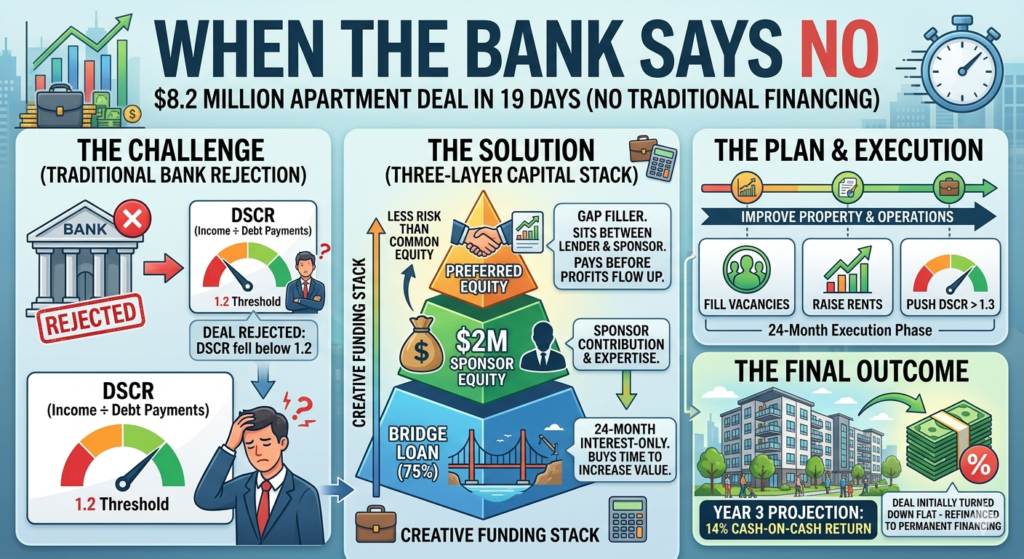

The deal failed traditional bank underwriting because of DSCR — Debt Service Coverage Ratio.

DSCR measures whether a property generates enough income to cover its debt payments:

DSCR = Net Operating Income ÷ Annual Debt Payments

Banks typically require a DSCR of 1.2 or higher. This property didn’t hit 1.2. Maybe the building had vacancies. Maybe rents were below market. Maybe operating expenses were too high. Whatever the reason — on paper, the income wasn’t sufficient.

Bank says no. Deal dead? Nope.

The Three-Layer Financing Stack

Instead of one loan from one bank, the team built a three-layer structure — and preferred equity real estate financing was the piece that made it work.

Layer 1 — Bridge Loan (75% of total cost)

- Short-term loan covering 75% of the acquisition cost

- Interest rate: SOFR + 3.25%

- Term: 24 months

- Payments: Interest only for the full 24 months — no principal paydown required

Layer 2 — Sponsor Equity ($2 million)

- The investor put in $2 million of their own cash

- This is their skin in the game

Layer 3 — Preferred Equity Real Estate Financing

- Filled the gap between what the bridge loan covered and what the sponsor could put in

- Return structure: 12% paid currently (monthly cash payments) + 4% accrued (paid later)

- Sits between the debt and the common equity — gets paid before the sponsor profits, but after the lender

Total: $8.2 million acquisition, closed in 19 days.

The Strategy: Lease Up and Stabilize

The 24-month interest-only period wasn’t just a financing convenience — it was the entire strategy.

During those two years, the plan was to fill vacancies, push rents to market rate, cut unnecessary operating expenses, and get the DSCR from below 1.2 to above 1.3.

Once the property hits 1.3 DSCR, it qualifies for permanent financing — a long-term loan with better terms, lower rates, and a fixed structure. The bridge loan gets paid off and replaced with something sustainable.

By year three, the sponsor was projecting a 14% cash-on-cash return on their $2 million investment. That’s $280,000 per year in cash flow on a deal that a bank initially rejected.

What Is Preferred Equity Real Estate Financing, Exactly?

This was the part I had to sit with for a minute.

Think of the capital stack like floors in a building:

| Floor | Who | Gets Paid When |

|---|---|---|

| Ground floor | Lender (Bridge Loan) | First — always |

| Middle floor | Preferred Equity | Second — before sponsor profits |

| Top floor | Sponsor (Common Equity) | Last — but biggest upside |

Preferred equity real estate investors get a fixed return — in this case 12% current + 4% accrued — before the sponsor sees any profit. They take less risk than the sponsor, so they get less upside. But they get paid first.

It’s not a loan. It’s not traditional equity. It sits in between — hence “preferred.”

According to BiggerPockets, preferred equity real estate structures have become increasingly common in value-add multifamily deals precisely because they fill the gap when traditional financing falls short — without requiring the sponsor to find a single massive equity partner.

Why This Matters for Philadelphia Investors

You’re probably not doing an $8.2 million deal tomorrow. Neither am I.

But understanding preferred equity real estate financing matters because the concepts scale down directly.

DSCR is relevant at every level. Even small multifamily deals in Philadelphia get underwritten on DSCR. If you’re buying a triplex and the numbers don’t work for a conventional loan, knowing the difference between 1.1 and 1.3 DSCR changes how you underwrite every deal.

Bridge loans exist for smaller deals too. Hard money is essentially a bridge loan for residential investors — short term, interest only, buy time to add value, then refinance into permanent financing. That’s literally the BRRRR strategy.

The capital stack concept scales down. Even on a $300,000 Philadelphia rowhouse flip, you have a capital stack — hard money loan, your equity, maybe a partner’s money. Understanding who gets paid first makes you a smarter investor at every level.

Run your own DSCR numbers with the DSCR Calculator before you approach any lender — conventional or creative.

Not financial advice — just someone doing a lot of research and asking a lot of questions.